Back from the MBA Secondary Conference in NYC. Generally the mood was upbeat, although regulatory issues weighed on everyone. Lots of talk about TRID.

Markets are flattish this morning as retailers report first quarter earnings. Wal Mart missed big yesterday, while Target came in better than expected this morning. Overall, the savings from lower gas prices are not being spent – they are being saved. In the battle of the home improvement stores, the Home Despot was the winner over Lowe’s this spring.

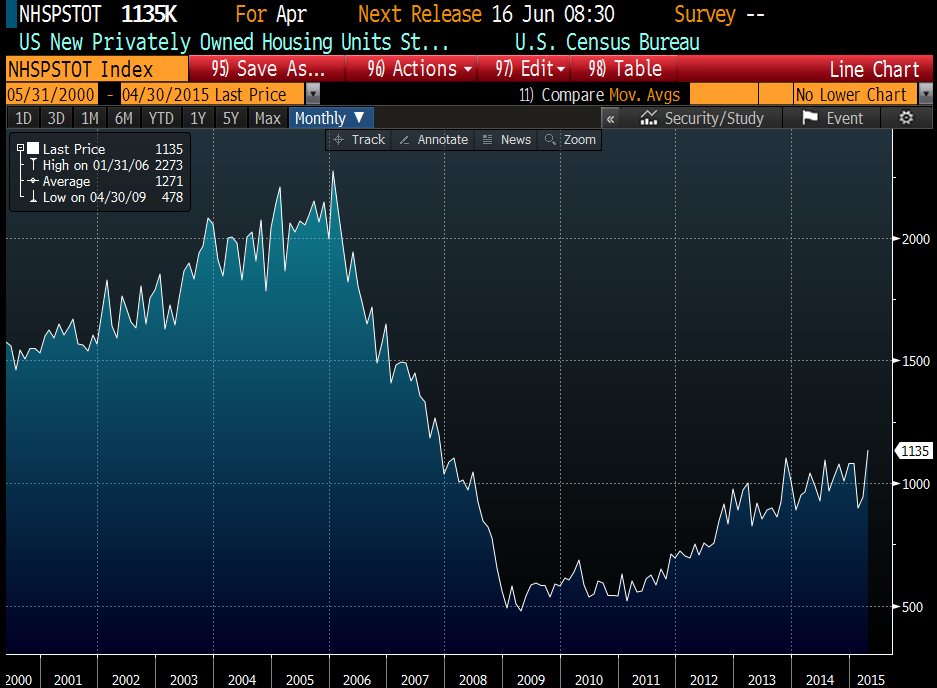

Catching up on economic data, the NAHB Housing Market Index fell to 54 from 56. Housing Starts came in well above expectations, at 1.135 million. Building Permits rose to 1.143 million as well. So, at least housing rebounded smartly after a tough Q1, however most other indicators (especially manufacturing-related) have not. Blame the dollar.

Chart: Housing Starts: 2000-Present

Mortgage Applications fell 1.5% last week, according to the MBA. Purchases fell 3.7% while refis were up .3%.

This afternoon, we will get the FOMC minutes. Of particular interest will be any mention of the huge bond market volatility we have been seeing, particularly emanating from Europe. Also look for their characterization of the first quarter weakness and the lack of a meaningful rebound. Janet Yellen will also be speaking at 1:00 pm EST. We could see some volatility in rates early this afternoon.

It is no secret that Bernie Sanders hates, hates, hates the financial sector. He has a new plan to fund free college education with a special tax on Wall Street. This is just election fodder to pull Hillary to the left and it is going absolutely nowhere.

Angela Merkel has given Greece until the end of the month to reach a deal with its creditors.

Filed under: Morning Report |

It’s a one-off, Bagger!

http://www.buzzfeed.com/virginiahughes/data-faked-in-study-about-gay-canvassers

Trust me wing-nut, the AGW science is Rock.Fucking.solid!!

LikeLike

This is how science works. The bad studies eventually get found out or refuted. And calling social science like this study tried to be science is a bit of stretch to begin with.

But go ahead and keep thinking that 95% of all scientists must be wrong about climate change since it has happened before.

LikeLike

yello:

But go ahead and keep thinking that 95% of all scientists must be wrong about climate change since it has happened before.

I wonder what it is exactly that you think 95% of all scientists agree on.

LikeLike

Is anyone here denying that the climate is changing?

And you might want to rethink the “science” behind your 95% number.

To be fair, it’s probably as rock solid as Michael Mann’s hockey stick.

LikeLike

Well, the Arctic ice cap is melting and melting pretty fast. Not only have the oil companies decided it is time to drill in the Arctic, but all shippers are seriously investigating the Arctic Passage, which should become free of ice year round within a decade.

So if that happens, do the investors in the new Canal in Central America simply lose their shirts when no northern hemisphere trade goes through it?

LikeLike

Mark:

Not only have the oil companies decided it is time to drill in the Arctic…

Doesn’t the fact that there is oil to be drilled in the Arctic imply that at some point in the distant past there was little or no ice in the Arctic? How would that have been even possible in the absence of man and his carbon polluting ways?

LikeLike

Doesn’t the fact that there is oil to be drilled in the Arctic imply that at some point in the distant past there was little or no ice in the Arctic?

Yes.

How would that have been even possible in the absence of man and his carbon polluting ways?

For answers to questions about sea ice changes in the Arctic over geologic time check out

http://nsidc.org/arcticseaicenews/faq/

—

My interest that led to my raising this speculation is geopolitical.

See http://www.cfr.org/arctic/strategy-advance-arctic-economy/p27258

For investor responses to short term changes in Arctic sea ice, the general subject of my speculation, I started with

http://www.shell.com/global/future-energy/arctic.html

and considering the huge tonnage of shipped petroleum products compared to everything else I recalled this:

http://www.cfr.org/arctic/thawing-arctic-risks-opportunities/p32082

Surely you know that Houston handles more tonnage through the Ship Channel than the total of the ports of NY and Los Angeles. You should know that the Gulf ports handle most of the tonnage in the USA and the main reason is oil and gas.

http://www.rita.dot.gov/bts/sites/rita.dot.gov.bts/files/publications/national_transportation_statistics/html/table_01_57.html

Perhaps you didn’t know that the Ship Channel is prepping for the increased shipping through Panama that was expected with the deepening of the existing Canal to take super tankers. I don’t actually expect anyone outside TX and LA to follow this stuff. George may read the Houston Chronicle daily, and I go here a couple of times a week: http://fuelfix.com/. Check out:

http://fuelfix.com/?s=arctic+oil

So news that may affect our area leads to speculating stuff like “what if Shell builds a refinery in Seattle?” and then deciding that Shell would find it cheaper to ship directly from the Arctic to the Gulf – no worries.

And then, by reason of catching a story on this Nicaraguan canal that mainly Chinese interests [I think] are building, I began to think that open Arctic shipping lanes might hose those guys [but incidentally be good for Houston no matter what].

I have tried here to explain the stream of consciousness that led to my musing. I only wondered if financial guys had put together these facts on the ground and whether anyone was pulling support on the Nicaragua venture.

Brent?

LikeLike

I have a friend in the industry. I am going to ask him what he has heard.

I’ll report back later.

LikeLike

Mark:

For answers to questions about sea ice changes in the Arctic over geologic time check out…

It was just a rhetorical question.

LikeLike

Mark:

So if that happens, do the investors in the new Canal in Central America simply lose their shirts when no northern hemisphere trade goes through it?

Only if it is economically more beneficial for the trade to move through the Arctic rather than the Central American canal, and we all know, of course, that AGW is an unmitigated calamity and can’t possibly be beneficial in any way at all.

LikeLike

Good piece on the aftermath of the American Civil War.

http://opinionator.blogs.nytimes.com/2015/05/19/how-the-civil-war-changed-the-world/?ref=opinion&_r=0

LikeLike

That Columbia mattress chick story gets more bullshittier.

http://reason.com/archives/2015/05/20/columbia-rape-saga-lingers-after-mattres

LikeLike

Everything you need to know about Constitutional law, the first of two parts:

http://www.thepublicdiscourse.com/2015/05/15013/

It’s final exam time at the nation’s law schools. That means it’s time for professors to concoct fiendish hypotheticals for essay exams and for students to cram, trying to sort out the various three-part, two-pronged, quadruple-somersault doctrinal “tests” and “tiers of scrutiny” with which the Supreme Court’s judicial decisions have cluttered the Constitution, and prepare to spit back the doctrinal gobbledygook in some equally incoherent form on the test.

This is what passes for “Constitutional Law” in our law schools these days: a hopeless mash-up of confusing half-truths, quarter-truths, and outright untruths, taught as “law.” For the desperate law student, I offer this super-duper two-part mini-review of everything you really need to know about constitutional law: part one today, and part two tomorrow.

A warning, however: this is probably not what your professor has been teaching you. It’s an unmasking of what he or she taught—and a brief recitation of the real, crucial questions about constitutional interpretation. Using what I say here might yield you nothing better than a C, depending on the instructor. But heck—that’s better than failing. Regurgitate what follows on the test and you might just pass; learn these principles in the next fifteen minutes and you will have learned more real constitutional law than your faithfully-attending, casebook-reading peers.

And as for the universe of non-law students out there: first, I commend you for your incredible good judgment! You are uncorrupted by a law school education! And I offer you the same mini-primer on “constitutional law,” to help you puncture the inflated puffery of your lawyer-friends (even lawyers need real people as friends) when they spout off about constitutional law “doctrine” in pseudo-intellectual fashion. This primer might also help you navigate through the fog of new Supreme Court decisions. ’Tis the season for these too. Once you realize what the justices are up to, you can see why it often makes so little sense.

LikeLike

Might as well, I already assume they’re banging anyway.

LikeLike

I can’t believe nancy is so dense she would say something like that with #MattressGirl running around with false accusations…

LikeLike

“It’s a “throwback to a former era and shouldn’t be in practice,” Pelosi said.”

Not hardly. It’s the exact result that the current zeitgeist demands.

LikeLike

Part 2 of everything you need to know about Constitutional law:

http://www.thepublicdiscourse.com/2015/05/15016/

We had just completed discussion of the first four methods, and have now arrived at the fifth technique: policy, pragmatism, or considerations of “substantive justice.”

As a technique of constitutional interpretation—of actual textual exegesis—of trying faithfully to ascertain the meanings of the Constitution’s words—policy-driven “interpretation” is, of course, completely illegitimate. Think about it: If you were really trying to figure out what the words of a written text actually mean, you wouldn’t start with the lawyers-joke question: “Well, what do you want them to mean?” Would you?

Policy-driven “interpretation” ignores a fairly obvious reality. The Constitution does not necessarily mean all good things. It countenanced slavery, originally, didn’t it? Did the words not mean what they meant just because they meant bad things? That’s just plain silly.

Moreover, what one person thinks is good “substantive justice,” another will think a wrongheaded atrocity. Did you notice, dear student, how so many so-called “Constitutional Law” classes tended to degenerate into simple political shouting matches over preferred policies on abortion, gay rights, affirmative action, war, the death penalty, and many other things? Did it ever occur to you that policy differences not actually addressed by the Constitution are to be resolved by democracy—by the institutions of representative government?

The outcomes-oriented method of constitutional “interpretation” reminds me of the way my high school chemistry lab partner—let’s call him “Cal” —and I used to write our lab reports. Cal, who is now a lawyer of course, would loudly and proudly proclaim our methodology to anyone who would listen: “First, draw the desired curve. Then, plot the data. If time permits … do the experiment!”

Alas, this is how the Supreme Court often plays the constitutional interpretation game. They are skilled practitioners of “The Cal-and-Mike-High-School-Chemistry-Lab-Experiment-Method of Constitutional Interpretation.” The justices begin with their desired conclusion, marshal the right arguments, and if time permits read the Constitution. Any number of Supreme Court cases read this way; they’re just dressed up outcome-driven policy decisions, clothed in legal language. All the Court’s abortion cases fit this description. So do all the gay rights cases. Watch for it to reappear in the Court’s pending same-sex marriage decisions.

LikeLike

So, question, did we lose the Republic due to Marbury v Madison?

LikeLike

McWing:

So, question, did we lose the Republic due to Marbury v Madison?

I don’t think it is necessarily fair to blame Marbury v Madison. It established the doctrine of judicial review, not judicial supremacy.

Since the Constitution is the supreme law of the law, it makes perfect sense that courts should defer to it rather than deferring to congressional legislation. But that doesn’t mean that both Congress and the president need to defer to SCOTUS’ declaration of what the constitution means. The branches are constitutionally co-equal, and within its own realm of power, each branch should come to, and act on, its own conclusions about what the Constitution means for a given issue. As the article said:

Neither the Constitution itself nor Marbury makes SCOTUS’ claims about what the Constitution says authoritative over the other branches.

I think what is to blame for the current sorry state of affairs is not Marbury, but is instead a widespread and drastic departure on the part of most politicians and judges (and many people in general) with regard to what government exists for in the first place. The philosophy of government held by the framers is simply no longer held by most politicians (or probably people) today, which has led to a complete abandonment of any real sense of obligation or fidelity towards the constitution. The Constitution is no longer viewed or used by politicians (among whom I include SCOTUS) as a truly legitimate guide and check on what government can and cannot do, but is instead viewed as simply a marketing tool for legitimizing (or de-legitimizing) any and all things that they want government to do (or not do) at any given time.

LikeLike

@ScottC1: “I wonder what it is exactly that you think 95% of all scientists agree on.”

I like what Michael Crichton said about consensus ≠ science. And, more to the point, as I think you are indicating, scientist do not agree on everything regarding anthropogenic global warming. They do not all agree with the models (all of which are flawed and will likely be deeply flawed for years, until such time as they can be developed with extreme AI, and even then if the results don’t match the consensus the models might need to be “tinkered” with). Not all agree as to causes or degrees or results (such as the cooling effect of increased cloud cover due to increased evaporation due to heat). They do not all agree on the hockey stick. Or, at least, there is not a 95% consensus on these things.

Even more so, there is disagreement as to outcomes. In general, a warmer planet offers many benefits, especially away from the equator. This is not a justification for doing nothing, or maintaining the status quo, but just a fact. A warmer planet does not automatically end in a disaster movie. Things that don’t involve giant asteroids or nuclear Armageddon rarely do.

There are also lots of non-scientific forces pushing for a particular conclusion that should be as suspect as research funded by the coal and oil industries. There is also a bone-deep ingrained narcissism that once put us at the center of the universe, and now puts us in a position to destroy planets with our cars and bbqs.

… which doesn’t even get to the proposed solutions, which, thus far, have mostly been variations on new forms of wealth redistribution or increased government regulation and control (that, naturally, come with kickbacks to the politicians who advocate for them). At best, they advance ideological ideas that existed well before being anchored to modern environmentalism.

LikeLike

@yellojkt: “This is how science works. The bad studies eventually get found out or refuted. And calling social science like this study tried to be science is a bit of stretch to begin with.”

Well, it’s how people work, technically, not “science” in it’s more idealized form. Yet this happens a lot of AGW, and experience tells me that’s a red flag. I also have yet to see anything that can demonstrate to me, as a lay person, that we are remotely capable of modeling systems with billions of inputs, that vast majority of which can’t be measured, and the vast majority of that which can be measured has a limited run of historical data, and get anything like an accurate prediction. Otherwise, we’d model much simpler complex systems, such as the stock market, and all become amazing wealthy. 😉

LikeLike

Otherwise, we’d model much simpler complex systems, such as the stock market, and all become amazing wealthy. 😉

Using standard competitive economic modeling, it seems to me that if we could all predict the stock market we would force it to an equilibrium that would not permit us all to become wealthy, but that would permit us all not to fail miserably, and probably earn a modest return on our investments in a growing economy, while minimizing our losses in a downturn.

Making no assumptions about causation, the insurance industry accepts the fact of warming to the point that it will not continue to write beach front homeowners policies, and O&G is drilling in the Arctic.

So let’s talk about working off the insurance industry models to make policy. Big public works projects will be necessary to move coastal cities inland over the next 50 years. I’ll bet the insurance lobby, which is very powerful, will push state leges and Congress to fund stuff like this, but more likely, to guarantee their policies.

I think they are betting that Galveston I. is doomed for human habitation. The Sea Wall held during Rita but the water level in the Bay rose so that the island was flooded from the mainland side. That’s gonna happen to Miami Beach, too. Maybe Manhattan. I am not actually predicting this – but some insurance lobbyists are. They don’t wanna be on the hook for this. So what will happen when gov tries to make them write affordable policies on the coast? They will get huge guarantees from the Federal gummint, that’s what.

Better to dismantle Galveston and Miami Beach, and put people to work digging, than subsidize the insurance industry? What do you think?

LikeLike

Mark:

Making no assumptions about causation, the insurance industry accepts the fact of warming to the point that it will not continue to write beach front homeowners policies…

The reluctance of insurance companies to write “affordable” policies on beach front property has existed for decades, long before the current AGW craze. Ever since, in fact, they discovered that hurricanes destroy houses and hurricanes come from the ocean. And governments have been involved in either enticing/forcing them to provide it, or providing it themselves, for just as long.

Better to dismantle Galveston and Miami Beach, and put people to work digging, than subsidize the insurance industry? What do you think?

I think the government should stop forcing insurance companies to write affordable policies and just let the market – and nature – takes its course.

BTW, if insurance companies are compelled or enticed to provide “affordable” insurance with tax dollars as a backstop on their losses, it is the insured, not the insurance companies, that are being subsidized. And I agree that they should not be subsidized.

LikeLike

Mark:

FYI, the National Flood Insurance Act was passed in 1968 precisely because most insurance companies had ceased to provide flood insurance by then. At the time the panic of the day was overpopulation, not AGW. (Predictions of a new ice age were still 7 or 8 years off at that point, if I am not mistaken.)

LikeLike

Do nothing. Based on your assertions people will be able to walk faster than the rising water. Let those living in “at risk” areas, you know,move.

Problem solved.

LikeLike

What is the likelyhood that insurance companies are using AGW as an excuse for rent-seeking?

LikeLike

McWing:

What is the likelyhood that insurance companies are using AGW as an excuse for rent-seeking?

Could be, I suppose, but if so I’d be interested in how they are doing it. I would imagine that most weather-related government insurance programs primarily redound to the benefit of the insured, not the insurer, by giving them under-priced insurance. Unless the government is forcing people to buy insurance who otherwise would not (eg Obamacare), or forcing people to buy over-priced insurance, I don’t know how the industry could be seen as rent seeking.

It is the case, I believe, that the government requires flood insurance on loans made against houses in federally designated flood zones, but it is the government itself, not insurance companies, which provides that insurance. And it does so at the wrong price, which is a) why it isn’t provided privately and b) why the program is hugely in debt.

http://www.npr.org/2014/01/01/258706269/federal-flood-insurance-program-drowning-in-debt-who-will-pay

LikeLike

What I’m suggesting is their desire to have the insurance they issue subsidized via the government to Keep Prices Affordable to Average Americans in areas that are allegedly susceptible to the result of an angry, wounded Gaia.

LikeLike

McWing:

What I’m suggesting is their desire to have the insurance they issue subsidized…

Which subsidies are you thinking of? The subsidies I know of (eg Citizens Property Insurance Corporation in Fla, the previously mentioned National Flood Insurance Program nationally) go directly to the insured in the form of government provided insurance. The industry doesn’t get anything from those.

LikeLike

What I was thinking of would be subsidies for areas that we would not otherwise think would need them. Increased rates in, say, Oklahoma, because the Climate Models tell us that there will be more tornados with greater ferocity (even though we are seeing record low numbers of them currently). Ditto insurance rates along the gulf coast because Climate Models predict a Greater Frequency of More Intense Hurricanes (despite a relative dearth of the them currently). Heck, I could see insurance companies seeking subsidies as they attempt to raise rates due to the increase in Extreme Weather that Climate Models are predicting.

See what I’m driving at here? It’s worked in regards to health insurance and subsidies via The Abomination. Why wouldn’t these same companies start lobbying to have it done on homeowner / property insurance as well. It can become a Crisis in Need of an Immediate Government Intervention to Resolve. The end result would be guaranteed profits and shitty insurance.

LikeLike

McWing:

What I was thinking of would be subsidies for areas that we would not otherwise think would need them.

Sure, it is possible that insurance companies might raise rates beyond “affordability” for spurious AGW reasons and then lobby the government to subsidize the rates in order to make them affordable. But I am not aware of that happening anywhere, and the primary subsidy model that I am aware of generally involves government providing too-cheap insurance directly to buyers, not indirectly via subsidies to insurance companies.

LikeLike

You’re leaving me NO ROOM for my paranoid ramblings here!

LikeLike

lol

LikeLike

BTW, the direct-to-buyer subsidy is ultimately the single-payer model that the left actually prefers for health care, too. But since they needed the support of the insurance companies in order to get anything passed, they had to go a different route to begin with. Thus the rent-seeking arrangement of guaranteed buyers and back-stopped losses in exchange for controlled premiums and coverage. But as I have mentioned, I fully expect that, in time, the left will join you in demonizing the insurance companies (just as they demonized the banks with regard to guaranteed student loans) as little more than rent-seeking middlemen costing the taxpayer money, and will seek to strip them out, thus achieving their wet dream of a single payer system.

You read it here first.

LikeLike

I think the government should stop forcing insurance companies to write affordable policies and just let the market – and nature – takes its course.

Fair point. It isn’t really a Hobson’s Choice, is it? We can do this without government intervention. As property becomes uninsurable, it will gradually be abandoned, or sold at huge discount to folks who will gamble. While flood insurance has been subsidized for decades, the refusal to write in many coastal places is recent.

It is pretty clear to me that New Orleans should be largely evacuated, accept for the levee areas, like Tulane University, Audobon Park, Vieux Carre, the CBD, the Port, and the Metarie Ridge. Figure a small city of 60000-90000 servicing the Port and the University and with a tourist attraction, would be both insurable and would survive. All that below sea level stuff would be gone. True wetland.

LikeLike

Mark:

We can do this without government intervention.

Agreed.

While flood insurance has been subsidized for decades, the refusal to write in many coastal places is recent.

Maybe the reluctance has grown in some places, but it has existed since at least the 1960s. This is from a paper on the history of home insurance (wind, not flood insurance) in Florida:

http://www.colorado.edu/hazards/publications/wp/wp96.html

LikeLike