Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1422.7 | 2.9 | 0.20% |

| Eurostoxx Index | 2648.5 | -2.6 | -0.10% |

| Oil (WTI) | 89.09 | 0.5 | 0.54% |

| LIBOR | 0.31 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 79.66 | -0.015 | -0.02% |

| 10 Year Govt Bond Yield | 1.78% | 0.00% | |

| RPX Composite Real Estate Index | 191.8 | 0.1 |

Markets are quiet this morning, as most of Europe is shut for Boxing Day. Bonds and MBS are flat.

Not much is happening on the fiscal cliff front, although Obama plans to cut his vacation short and return to Washington to try and hammer out a deal. Chances of any sort of grand bargain are virtually nil; all that could be accomplished at this point is some sort of fig leaf. In spite of the political and economic uncertainty, and the early indications of a weak Christmas, the bond market still refuses to price in the possibility of a recession.

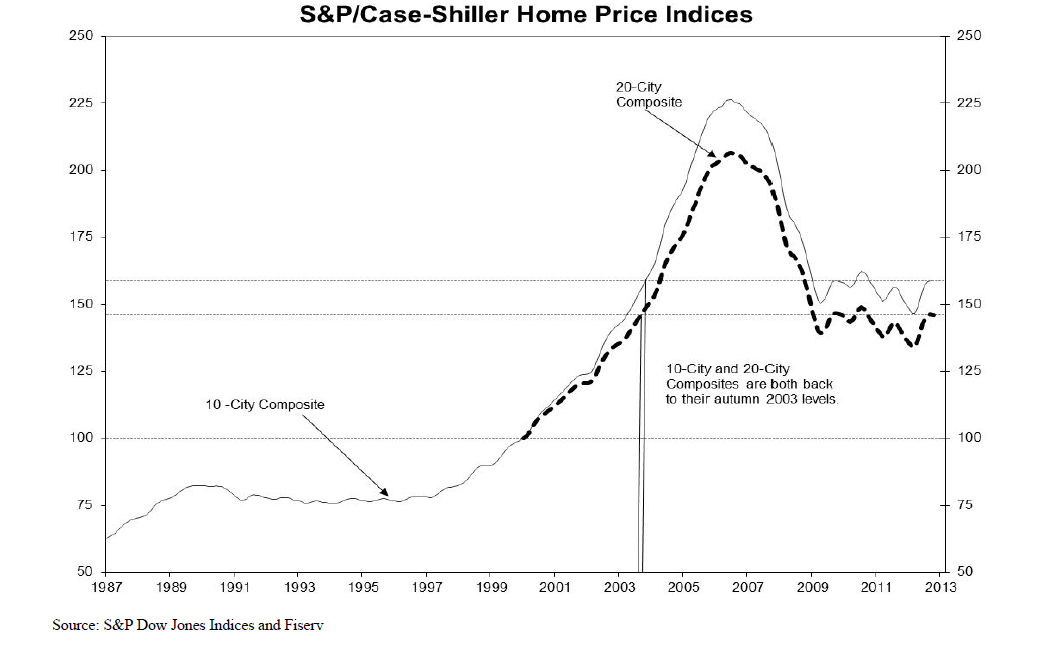

The S&P / Case-Schiller index of home values came in at 145.93 for the month of October, up 4.3% year-over-year and up 66 basis points month-over-month. The hardest-hit MSAs continued to show the biggest gains, with prices up 22% in Phoenix and 10% in Detroit. The Northeast MSAs (Boston and NY) are showing the smallest increases.

Chart: S&P / Case-Schiller:

The Obama administration is considering expanding its mortgage-refinancing program to include underwater borrowers with non government loans. Such a move would require legislation to change Fannie and Fred’s charters and would also involve a bump in the guarantee fee to price in the additional risk. It will also require the blessing of FHFA, which has indicated general support for the program. Finally, it will require some sort of immunity from buy-back risk in order to get originators on board.

A new study confirms what many have thought about high-frequency trading: It is highly profitable and adds no value to the system as a whole. Aggressive, liquidity-taking high frequency trading (in other words, front-running) does the best. The profitability of HFT seems to be persistent – new entrants are less likely to be profitable and are more likely to exit. Speed matters above all, and that is why James Simons is so consistently profitable.

Filed under: Morning Report | 5 Comments »