Vital Statistics:

|

Last |

Change |

Percent |

| S&P Futures |

1742.0 |

-1.7 |

-0.10% |

| Eurostoxx Index |

2968.5 |

6.1 |

0.20% |

| Oil (WTI) |

97.58 |

0.4 |

0.40% |

| LIBOR |

0.236 |

0.000 |

-0.04% |

| US Dollar Index (DXY) |

81.15 |

0.024 |

0.03% |

| 10 Year Govt Bond Yield |

2.64% |

0.01% |

|

| Current Coupon Ginnie Mae TBA |

106.1 |

0.0 |

|

| Current Coupon Fannie Mae TBA |

104.8 |

0.0 |

|

| RPX Composite Real Estate Index |

200.7 |

-0.2 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.24 |

|

|

Markets are flattish this morning after the ADP Employment Report forecast that 175,000 jobs were created in January. Bonds and MBS are flat. Markets might be a little thin today as the Northeast is snowed in once again.

The ADP report suggests a “meh” number for this Friday’s jobs report, although the ADP report has been a lousy predictor of the BLS numbers lately – last month, ADP forecast 238k jobs and the BLS number came in at 87K. So take this number with a grain of salt. Given what we know about the Fed’s intentions regarding tapering, it would take an extraordinary number on either side to change the Fed’s glidepath.

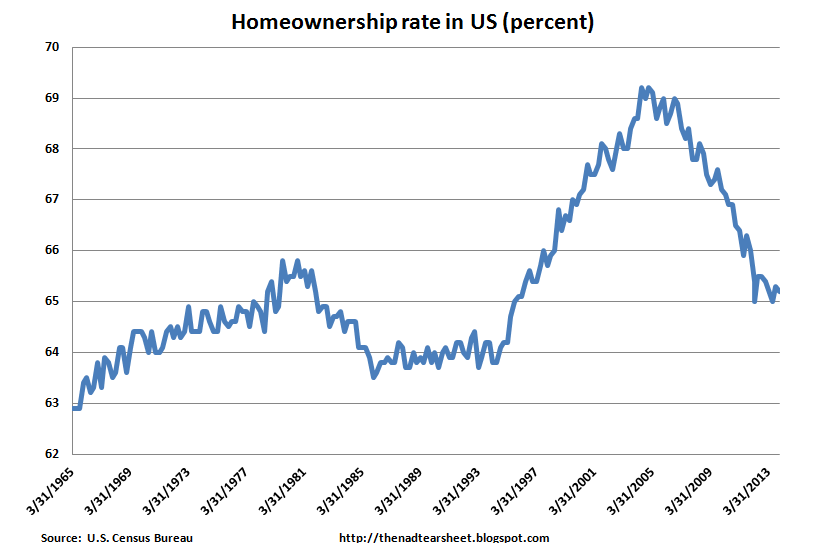

Mortgage Applications rose .4% last week, which is actually a pretty dismal number when you think about it – mortgage rates fell 7 basis points last week and we had an easy comparison given the MLK holiday the week before. Purchase apps were down 3.8%, while refis were up 2.8%. That said, this is a seasonally weak time, so it is hard to read too much into it, but there it is. FWIW, the homebuilders that have reported fourth quarter earnings so far noted strong traffic in January, which is an encouraging sign.

In the partisan spin wars about obamacare, the CBO launched a new toy to tussle over, with a study showing that obamacare would

cost the economy about 2 million jobs. Republicans cited the study, saying that it confirmed what we knew all along, that obamacare would be a job killer. When you look at what CBO actually said, however, it they concluded that the job losses would comhe from people voluntarily leaving the work force, not employers cutting hours / jobs. In fact, CBO said the job losses attributable to employers cutting jobs was so small they didn’t bother to measure it. Obviously Elmendorf (head of the CBO) hasn’t been checking out the reports put out by the regional Federal Reserve banks, or the NFIB small business surveys, which document actual hiring plans from actual businesses and instead is relying on some sort of model to predict what will happen.

Regardless of how their model is specified, the CBO is in effect arguing that the laws of supply and demand are different in the labor market (which is an underlying assumption of most other left-wing labor policy). The normal supply / demand curve looks like this: As prices increase, more supply comes out (which means if compensation increases, more people want to work) and demand decreases ( which means businesses will want to cut costs / substitute labor for technology, etc) All pretty common-sense stuff. Anyone who has taken Econ 101 will recognize this chart:

However, CBO is making a different argument: Because of obamacare (which raises the price of labor through employer mandates, etc) people will drop out of the labor force more than they would otherwise. In other words, as price increases, supply will decrease. If people are starting to make more, does anyone really think that would encourage people to quit working? And their second argument makes even less sense – that employers will ignore increased compensation costs and continue to hire as before. Anyone who has used a self-checkout at the supermarket knows that argument is bunk. The CBO is arguing that employer demand for labor is inelastic – meaning that no matter what the price of labor is, they will pay it. In other words, if prices increase, demand stays the same. That may be true of certain items (think life-saving drugs like insulin), but certainly not 99.9% of the goods out there, and certainly not labor. Heck, if that was the case, raise the minimum wage to a million dollars and we’ll all be rich! Essentially, CBO is arguing that the labor market looks like this:

I’ll leave it to the reader to figure out whether this makes sense or not.

This study, along with another Elmendorf special – that mass principal mods would save the government money – makes me wonder how partisan the supposedly non-partisan Elmendorf CBO is.

Filed under: Morning Report | 45 Comments »