Stocks are lower this morning on no real news. Bonds and MBS are down as European bonds sell off.

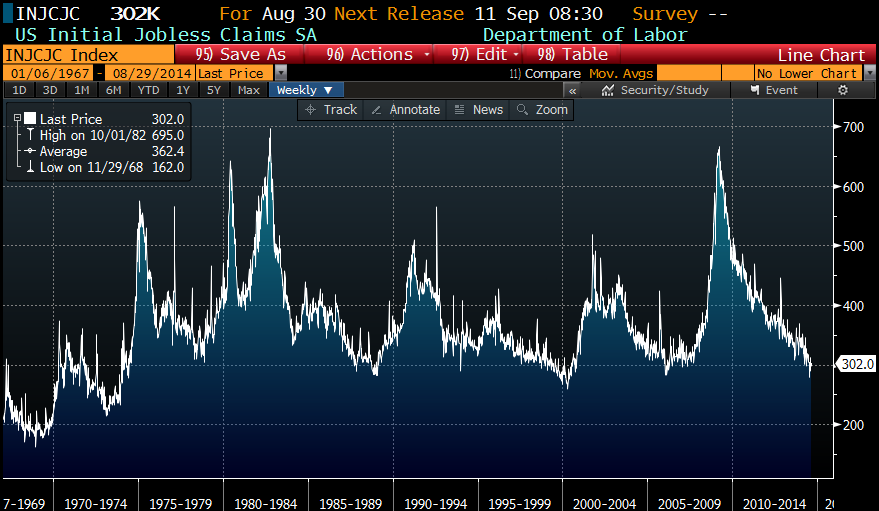

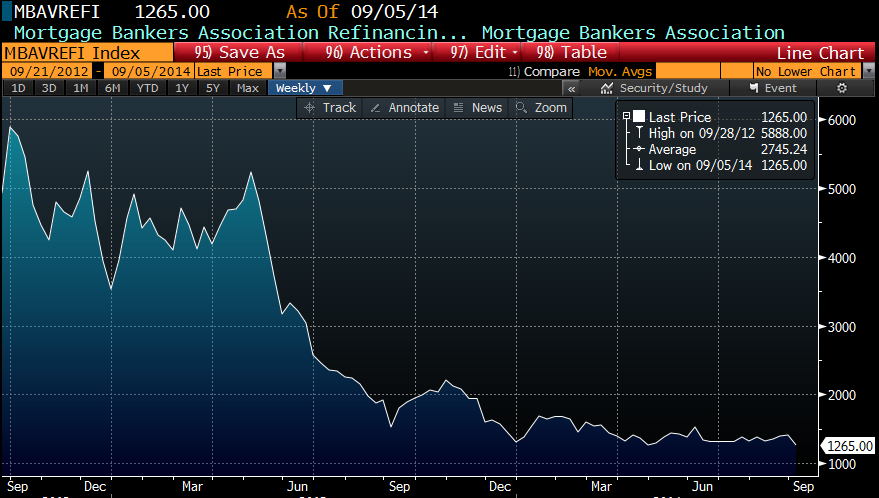

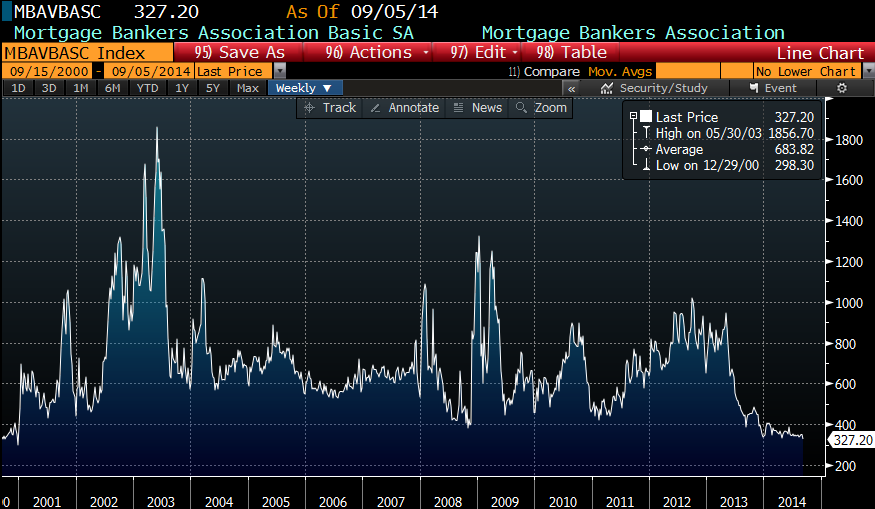

Mortgage Applications fell 7.2% last week as we had the Labor Day holiday and rates backed up. Purchases fell 2.6% while refis fell 10.7%. Refis accounted for 55.4% of all loans. The refi index just hit its lows for the year, even though rates have fallen almost 50 basis points. This effect is called prepayment burnout, and it is due to the fact that anyone that has been able to refinance already has. The driver of refis going forward will be home price appreciation, not rates.

Note that the overall mortgage application index is hitting lows not seen since 2000.

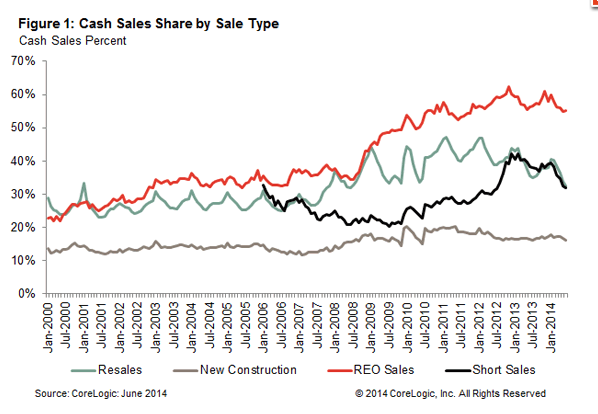

On the plus side, all-cash transactions are down to a six year low. Cash sales fell to 33% of total home sales in June, down from 36.3% a year ago.

Rep Maxine Waters (D-CA) is introducing legislation to change what goes on credit reports. One fix being considered is eliminating medial debt, which accounts for more than half of all unpaid debt in collection, from credit scores. Other changes would remove settled debts, remove black marks after 4 years instead of 7, and remove student debt defaults if the loan performs for a set period thereafter. The idea is to open access to credit.

Think fast food workers are irreplaceable? Think again. McDonalds is expanding a test concept allowing people to order via a tablet. This makes a good juxtaposition to the “living wage” strikes and legislation being considered.

Unintended consequence of ZIRP, number 1,234,567 – LBO funds are ratcheting up the leverage to boost returns. Not only that, but credit quality and covenants have been declining in these deals. The S&P 500, sitting at record levels, is assigning a 100% probability that the Fed can stick the landing and start raising interest rates without anyone blowing up. As we saw when the Fed started raising rates in 1994, 1999, and 2004, bad things tend to happen (Orange County in 94, the end of the stock market bubble, the end of the real estate bubble). If I was fully invested in the market, I would begin to finish my drink, find my coat, and watch the door.

Filed under: Morning Report | 35 Comments »