Green on the screen again this morning as stocks try to rebound. Yesterday, stocks traded up early only to give it all back late in the day and close with big losses. Bonds and MBS are falling again.

Durable Goods orders were strong at 2%, and June’s number was revised upward. Capital Goods Orders Non-defense, ex-air (a proxy for business capital investment) rose 2.2% versus a 0.3% expectation, while June was revised upward from 0.9% to 1.4%. These were the highest readings in a year.

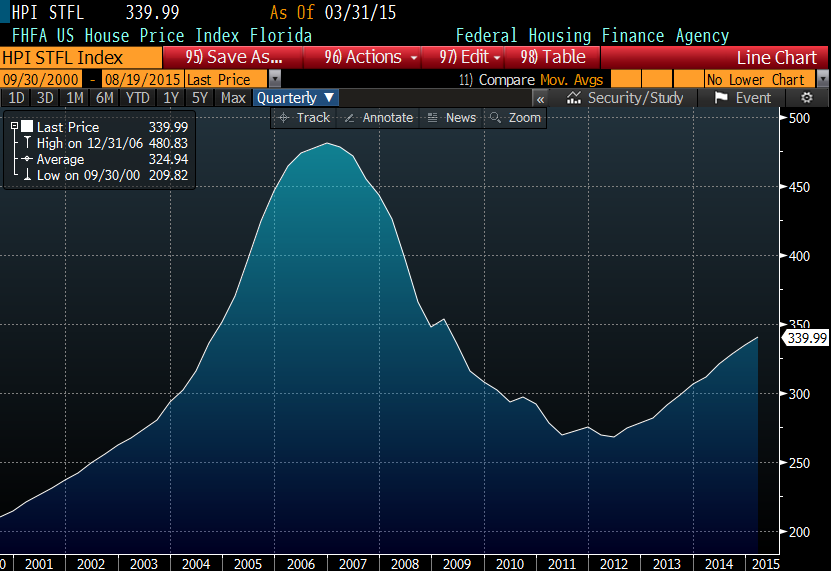

Mortgage Applications rose 0.2% last week as purchases rose 1,7% and refis fell 1%. Surprising that refis fell given the 17 basis point drop in the 10 year, but it looked like TBAs (which set mortgage rates) largely ignored the move in the bond market.

Not sure what caused yesterday’s late day sell-off, but the S&P 500 made a 60 point swoon in the last hour of trading to close down 26 points.

The other interesting thing about this sell-off has been the fact that bonds have not reacted much to the sell-off. The flight to safety trade has been almost non-existent in Treasuries. Odd, since the sell-off has taken down the probability of a rate hike in September. In fact, many strategists are moving out their estimate for the first hike to 2016.

Larry Summers was arguing over the weekend that financial conditions are acting like a tightening, and therefore the Fed doesn’t really need to raise rates right now. Hotlanta Fed President Dennis Lockhart said that conditions in the financial markets have complicated the Fed’s decision. By any measure, inflation is nowhere to be found. Given the fear of replicating the 1937 mistake, the Fed is probably going to err on the side of caution. Aside from the psychological discomfort of having rates at 0%, what reason is there to raise rates?

The carnage in the stock markets in Asia have created some bargains. HTC (the cellphone maker) is trading at a discount to cash. Market cap of $39.7B, no debt, $47.2 billion of cash. Like buying dollar bills for 84 cents. In crisis, opportunity.

Filed under: Morning Report | 55 Comments »

{kind=link}