Posted on October 9, 2015 by Brent Nyitray

Markets are higher this morning as commodities continue to rebound. Bonds and MBS are down.

Import Prices fell 0.1% in September and are down almost 11% on a year-over-year basis.

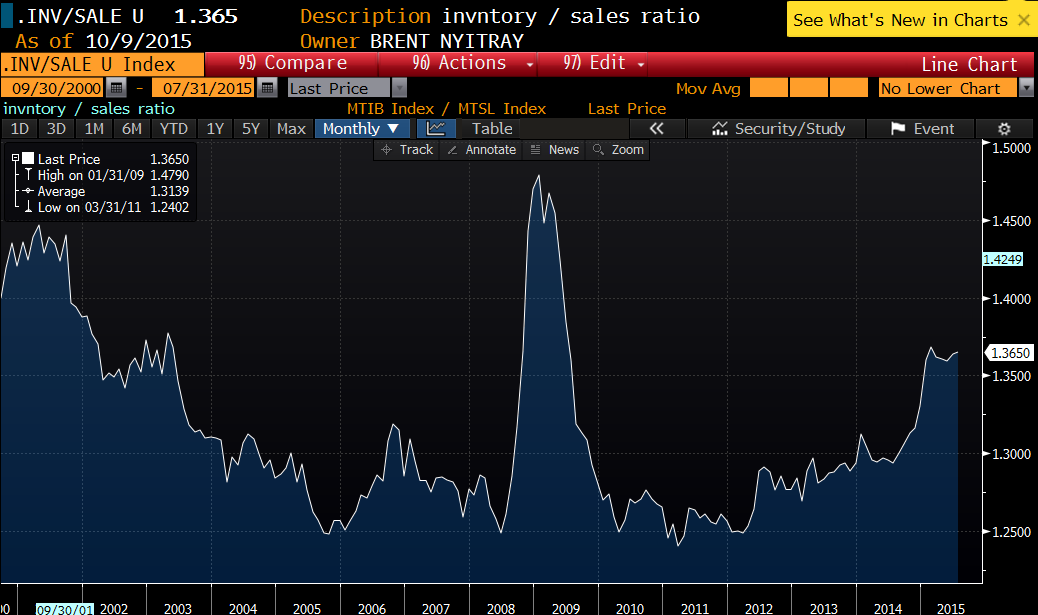

Wholesale inventories rose 0.1% in August, while wholesale sales fell 1%. Both numbers were worse than expectations. The increase in the inventory to sales ratio is a worrisome sign., You typically see the ratio build ahead of a cyclical recession.

The FOMC minutes confirmed what everyone suspected – that international worries prompted the Fed to hold interest rates steady at the September FOMC meeting. Overall, the Committee seemed rather constructive on the US economy in general. The Fed Funds futures are currently handicapping a 10% probability of a hike at the October meeting and something like 40% in December.

Representative Kevin McCarthy withdrew his name from consideration for the next House speaker after allegations of an affair ended up on a Wikipedia page. This leaves current speaker John Boehner in charge for the time being. Interestingly, the Wikipedia edit emanated from the US government itself – someone in the Department of Homeland Security. After the Secret Service started distributing confidential information on Representative Chaffetz, it looks like the worker bees in the government are going directly after Republican politicians. It will be interesting to see if anyone in the Obama administration actually cares.

Hillary’s plan for the financial system. A surtax on banks with over $50 billion in assets, an increase in the statute of limitations for financial crimes, and toughening the Volcker rule regarding proprietary trading.

Filed under: Morning Report | 29 Comments »

Posted on October 8, 2015 by Brent Nyitray

Markets are lower this morning on overseas weakness. Bonds and MBS are up.

Third quarter earnings season starts tonight with the traditional report out of Alcoa.

Initial Jobless Claims fell to 263k last week, the lowest since July.

The minutes from the September FOMC meeting will be out at 2:00 pm EST. Be aware of possible bond market volatility as the market digests it.

The Bloomberg Consumer Comfort Index rose to 44.8 from 43 last week.

Fannie Mae is announcing further reps and warranties guidance for loans starting Jan 1. It will include new alternatives to repurchase if the loan has a defect. The government is sick and tired of tight credit, especially at the lower end of the credit spectrum. These are intended to ease credit by giving lenders more certainty. The government is clearly worried given that the big banks like JP Morgan are backing away from FHA originations.

Larry Summers makes the case for going big on expansionary fiscal policy. His argument is that China’s slowdown threatens to drag the global economy into a secular stagnation similar to what Japan has been going through. He argues that monetary policy is pretty much played out: rates are at zero, and the stimulative effect of additional QE with the 10 year at 2% would be de minimus. He argues for a new “New Deal” where the government deficit spends on infrastructure spending. Of course this isn’t a new idea in the modern age: Japan has been doing precisely that for 25 years and has nothing to show for it except for a debt to GDP ratio of 2.3x. That would be like the US spending $40 trillion over 25 years. Before we advocate spending that kind of money, we should figure out why it hasn’t worked in Japan.. And if over 1 quadrillion yen is not enough, then what is? We need a better answer than the un-falsifiable “More Cowbell.” If the Rx only works in theory, then maybe the answer is to just slug it out until the economy corrects on its own.

Filed under: Morning Report | 12 Comments »

Posted on October 7, 2015 by Brent Nyitray

Mortgage applications rose 25% last week as purchases rose 27%% and refis rose 24%. That is a surprising result given the Bankrate 30 year fixed rate mortgage rose 5 basis points last week. Some think that it was partly TRID-driven.

Janet Yellen’s intention to let the labor market run hot for a few years has some Fed watchers worried. The criticisms range from fears about creating another 1970s – style inflationary environment to worries about the Fed’s credibility. We are in uncharted territory with the amount of control central banks worldwide are exercising over the economy. FWIW, I do not see much in the way of similarities between the 1970s and today: capacity utilization is low, and the chance of an oil shock is pretty remote. In fact we have the exact opposite situation. The inflation hawks make the case that monetary policy acts with such a lag that the die may already be cast for higher inflation (a similar argument that some of the global warming alarmists make with respect to CO2 in the atmosphere) The other point is more valid: the evidence that the Fed can influence wages and labor force participation is weak and the Fed is setting up unrealistic expectations that could damage its credibility down the road.

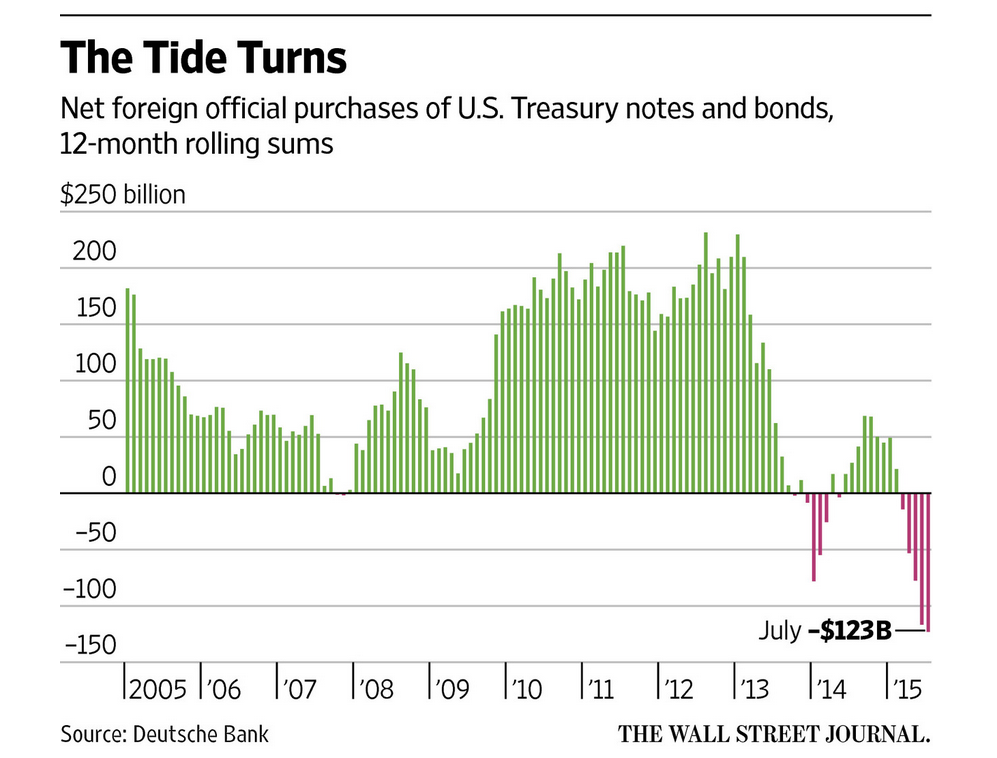

As we contemplate higher interest rates, foreigners are selling US Treasuries. While economic fundamentals will ultimately matter more than foreign fund flows, but it looks like foreign investors are cutting exposure ahead of higher rates. It probably will affect volatility, as primary dealers have pulled back market-making activity and Treasury markets have become less liquid in general.

Now that house prices are approaching the 2006 peaks, some are arguing that we are in another bubble. Affordability is down as wages have gone nowhere, and scarcity is driving up prices. FWIW, bubbles are psychological phenomenons – the occur when buyers (and lenders) believe an asset is special and cannot go anywhere but up. We won’t see another housing bubble in the US, but our grandkids might.

Filed under: Morning Report | 3 Comments »

Posted on October 6, 2015 by Brent Nyitray

Stocks are unchanged this morning as there is very little in the way of economic data / earnings to move markets. Bonds and MBS are down small.

The trade deficit widened to 48 billion in August as the strong dollar cuts exports and increases imports.

The IMF cut is global growth estimate to 3.1% from 3.3%. Blame weak commodity prices.

Economic Optimism improved markedly according to Investors Business Daily and TIPP Online. Many of these consumer confidence indices are merely inverse gasoline price indices. Falling gasoline prices makes people happy.

Home prices rose almost 7% in August on a year-over-year basis, according to CoreLogic. They are forecasting home price appreciation around 4.3% over the next year.

Bill Gross sees another 10% downside in stocks and is recommending sitting in cash for a while. His point is that corporate profits are flatlining as commodity prices hurt earnings in the energy patch and the strong dollar hurts manufacturers. Expect more layoffs in the energy sector. Bill Gross called the Chinese sell-off earlier this year as well as the German Bund sell off.

TRID is expected to delay closings as people get adjusted to the new rules. CFPB Chairman Richard Cordray says the agency will give lenders who are making good-faith efforts to comply with the new rules a break: “Nobody believes that market participants are going to be trying to abuse consumers here; they’re trying to change their systems. So we’ll be diagnostic and corrective, not punitive, and there will be time for them to work to get it right and not be perfect on the first day,” said Cordray. We’ll see if that actually happens.

Filed under: Morning Report | 22 Comments »

Posted on October 5, 2015 by Brent Nyitray

Markets are higher this morning on overseas strength. Bonds and MBS are down.

The Labor Market Conditions Index fell from a downward-revised 1.2 to zero. This has been the average since 2000.

The Markit US Composite PMI came in at 55, while the services PMI came in at 55.1. The ISM Non-Manufacturing Composite fell from 59 to 56.9.

The Bernank weighs in on raising rates. His Rx: don’t. Separately, DoubleLine’s Jeffrey Gundlach thinks we have further downside in risk assets like junk bonds, US equities and emerging markets stocks and bonds. His point: people are holding and hoping these assets rebound. That isn’t the psychology of a bottoming process. That happens when people throw in the towel and sell.

It is looking like the Trans-Pacific Partnership free trade deal is pretty much done. It still has to get through Congress, although he did get fast-track approval. I suspect it won’t move the needle that much for the US economically. It is mainly about intellectual property protection for US firms.

Sometimes bad ideas get implemented, fail, become forgotten, and then come back, like Freddy Kreuger. One such idea is the financial transactions tax, also known as the Robin Hood tax. It is back in vogue in Europe, and Bernie Sander wants a 50 basis point tax on all stock trades, a 11 basis points on bonds and 5 on derivatives will be able to fund a slew of new government benefits. Don’t believe it. While leftist politicians love to promote ideas like this as new, they aren’t. They have been tried and discarded. Sweden implemented on in the 1980s, only to see most stock trading in Swedish stocks flee to London. The UK in fact did implement one for stock trades, and all it did was drive institutional investors to use swaps to sidestep it and retail investors to go to betting parlors like City Index. They will sell it as raising a lot of revenue – it won’t simply because it will kill high frequency trading, and volume will dry up. They will sell it as reducing volatility – some (not all, but some) of HFT is actually market-making which is stabilizing. We don’t really have market-makers or specialists on the floor of the New York Stock Exchange like we used to. You could make the argument that it will increase, not decrease volatility. Anyway, #FeelTheBern is big on this idea – he should take a look at how it has (not) worked in the past.

Filed under: Morning Report | 15 Comments »

Posted on October 2, 2015 by Brent Nyitray

Stocks are lower after the jobs report disappointed. Bonds and MBS are up big

- Change in nonfarm payrolls +142k vs. +201k expected

- Two month revision -59k

- Unemployment rate 5.1% (in line with expectations)

- Average Hourly earnings 0% month over month +2.2% YOY

- Labor force participation rate falls to 62.4%

Very disappointing jobs report. No wage growth, and the labor force participation rate has fallen all the way back to Oct 1977 levels, which was the time when Reggie Jackson earned his nickname Mr October.

Stock index futures reversed a strong rally on the news. The 10 year bond yield dropped 12 basis points as well. It certainly looks like the decision to stand pat in September was the right one. For all the Fed’s discussion of October being a “live” FOMC meeting, consider it dead.

In other economic news, factory orders fell 1.7% in August and the ISM New York index fell to 44.5 from 51.1.

Yesterday, the House Financial Services Committee passed a bill to bring a bit of accountability and control to the CFPB. The director will be replaced with a 5 member commission, and there will be an inspector general. The CFPB is currently under the Fed, and gets its funding there. Congress has no say over their operations. This was intentional, to prevent a more conservative Congress from de-fanging the agency.

Finally, it looks like Hurricane Joaquin is going to miss the East Coast.

Filed under: Morning Report | 28 Comments »

Posted on October 1, 2015 by Brent Nyitray

Stocks are higher after yesterday’s rally. Given that yesterday was the end of a pretty lousy month (and quarter) it looked like people gunned the market a little to make their quarterly returns look a little better. Bond yields continue to grind lower.

The next two days are going to have a lot of economic data.

The ISM Manufacturing Index fell to 50.2 in September from 51.1 in August. 7 industries reported expansion, while 11 reported contraction. The slowdown in China and the strong US dollar are weighing on business confidence. A 50.2 reading would correspond to about a 2.2% GDP growth rate.

Initial Jobless Claims rose to 277k last week. We continue to bounce around the lows with this number. That said….

Jobless Claims may be increasing in the future, as Challenger and Gray announced job cuts increased 93%. This indicator combs the newswires for companies making announcements for job cuts. Something like 58,000 job cut announcements were made in September, with the 30,000 cuts at HP accounting for most of it.

The Bloomberg Consumer Comfort index rose to 43 from 41.9 last week.

Filed under: Morning Report | 26 Comments »

Posted on September 30, 2015 by Brent Nyitray

Stocks are up this morning on no real news. Feels like end of month / quarter window dressing. Bonds and MBS are down small

Mortgage Applications fell 6.7% last week as purchases fell 5.6% and refis fell 7.5%.

The ISM Milwaukee index fell to 39.44 from 47.7 last month. The Chicago Purchasing Manager Index fell to 48.7 from 54.4. The strong dollar is taking its toll on manufacturers.

All cash sales dropped to 31% in June, according to Corelogic. The historical, pre-bubble average is close to 25%. This speaks to the lack of first time homebuyers. It also speaks to an increase in gettable loans as that number reverts to the mean, even if home sales remain flat.

One of the big questions facing the Fed concerns falling unemployment and a falling labor force participation rate. Intuitively, you would think that as unemployment falls, people who are not currently in the labor force but want to be would find jobs, which would push up the participation rate. If the labor force participation rate remains low, that means the potential growth of the economy remains low, which means a slow, plodding recovery that won’t feel like any sort of economic boom. It also means inflation should, at least in theory, come back as companies bid up the wages of the fewer workers that are left. So far we aren’t seeing that. Millennials should be picking up the slack of retiring boomers but so far it hasn’t happened. And if Millennials don’t do it, then you need to pick up immigration.

Filed under: Morning Report | 15 Comments »

Posted on September 29, 2015 by Brent Nyitray

Markets are up this morning on good economic news overseas. Bonds and MBS are up small.

Consumer Confidence increased to 103 in September from 101.3.

NAR is saying they expect TRID to delay closings by up to 15 days. There will undoubtedly be a learning curve for the industry. TRID is the biggest change to the industry since the implementation of Dodd-Frank. CFPB claims they will use discretion in not going after lenders who make mistakes but are making a good-faith effort to work within the rules.

NAR put out the list of the 20 hottest real estate markets. While some at the top are not surprising (San Francisco) some of the other names are more associated with the economic dumpster fires we saw as the collapse began. Cities like Stockton CA and Detroit MI are included in the 20 hottest markets.

Glencore (which used to be called Xstrata) is a Swiss commodity trader who has been subject to solvency rumors. The stock has gotten hammered over the past year (down over 80%) but is up big today after addressing market rumors about solvency problems. While real estate types don’t typically have to worry about what happens in the area of precious metals, energy, and ag, stress in these markets can spill over to the rest of the financial sector. What does this mean for LOs? Stress = lower interest rates.

Speaking of stress, mutual funds that mimic hedge fund strategies may find themselves wrapped around the axle if we have a period of stress. Hedge fund arbitrage strategies typically require leverage and often invest in illiquid assets. Hedge funds at least have quarterly redemptions, which makes it easier to exit positions if need be. Mutual funds have no wiggle room – they have to accept redemptions daily. This could get ugly if markets turn south.

Filed under: Morning Report | 13 Comments »

Posted on September 28, 2015 by Brent Nyitray

Stocks are lower this morning on no real news. Bonds and MBS are up.

We have some important data this week, with construction spending, the ISM data and the jobs report on Friday. The market is forecasting a jump in wage inflation and that will be the number everyone is going to focus on.

Personal Spending rose 0.4% and Personal Income rose 0.3% in August. Inflation came in at 0.1% month-over-month and up 1.3% year-over-year.

Pending Home Sales fell 1.4% in August, but are up 6.7% year-over-year.

The Dallas Fed Manufacturing Index came in less negative than forecast.

On Friday, Speaker of the House John Boehner announced he was resigning. At the margin, it probably means a clean continuing resolution (in other words, no government shutdown). This isn’t going to matter to the markets one way or another – they recognize government shutdowns and debt ceiling fights as what they are: a chance for politicians to posture, and otherwise something to ignore.

The favorite to replace Boehner is Kevin McCarthy from California.

Speaking of government shutdowns and the debt ceiling, it does have an effect on the bond markets. The debt ceiling’s proximity means the government has to issue less T-bills than it ordinarily would, which makes them scarce and therefore they have ultra-low interest rates. This is bad news for money market funds and other savers. That said, ZIRP is the primary reason the issue.

Filed under: Morning Report | 31 Comments »