Stocks are up this morning on no real news. Bonds and MBS are up small.

We have a holiday shortened week, with markets closing early on Thursday. We do get some important data with the final revision to Q3 GDP, Existing Home Sales, New Home Sales, the FHFA House Price Index, personal spending and income, and inflation. Basically a week’s worth of data crammed into 3 days.

Oil continues to fall, hitting $34.23 a barrel for WTI.

The Chicago Fed National Activity Index fell to -.3 from – .17.

Goldman is predicting a March rate hike – a “fairly easy path.” They anticipate growth will remain above trend and employment growth to be well above breakeven. Inflation will pick up as the the big swoon in oil from $100 to $50 will be a year old and won’t be pushing down the inflation numbers.

This Guardian article details at least one set of layers of Denialism about Anthropic Global Warming (AGW). I dropped the phrase climate change for most part when I learned that Frank Luntz had coined it in order to obfuscate the direction of the change. Rather than just re-iterate the Guardian article which is a good read, I will annotate my opinions on the stages.

Stage 1: Deny the Problem Exists

Most people are beyond this stage. There is too much anecdotal evidence out there such as melting glaciers rising high tide lines to completely dispute the phenomenon. But every winter some congressman brings a snowball into the chambers to have a good laugh at all those pointy headed on-the-take climate scientists.

Stage 2: Deny We’re the Cause

The key word in AGW is “anthropic”. Climate changes all the time because of long term patterns, volcanic activity, sunspots, etc. What is more important to recognize is that for at least a century now we have been pumping ever increasing amounts of carbon dioxide and other chemicals into the atmosphere.

Stage 3: Deny It’s a Problem

Here is where we start hitting regions of debateability. Clearly the Bangladeshi are fucked. But they always have been. This is just one more reason that being poor in southern Asia is a bad lifestyle choice. However the people in Miami Beach, Norfolk, and eventually Manhattan’s Lower East Side are going to realize that being near navigable bodies of water is no longer the economic benefit it used to be. However we do have a lot of sunk economic infrastructure in areas which will eventually be under water.

Stage 4: Deny We can Solve It

Many of these arguments start to delve into the geopolitical realm. Without China and India getting on board, there isn’t much traction that can be made. And they are rightfully suspicious in claims that they need to curtail their climb up the prosperity curve for our sake. And also, some of the geo-engineering ideas such as large scale sequestration are just scary.

Stage 5: It’s too Late

Here is the argument I am most sympathetic to. We may have already passed the point of no return on some parameters. There are djinnis which just can’t be put back in the bottle. However, we really don’t know where the irreversible catastrophic lines in the sand are. Both climate and weather are chaotic systems and responses are non-linear. But fatalism is never a good look.

Personally I feel that climate change denialism is an astroturfed phenomenon created by the resource extraction industries to obfuscate their role in the unfunded externalities disaster which is impending. But that’s just my opinion, I could be wrong.

On a philosophical level, dealing with AGW requires cooperation on a global governmental level which is anathema to certain political philosophies. And some can be rightfully fearful of AGW as a camel nose under the tent way to impose radical systemic political change. But in the past we have accepted environmental regulation as qualified benefits to society. Clean air and water are luxury goods but we should allow ourselves to afford them. And a stable (if changing) climate is perhaps the biggest factor of life on earth we have taken for granted hitherto.

Recommended Reading

Climate change as a science fiction topic has been around for decades depending on how far back you want to take it. Lots of post-apocalyptic nuclear novels are easily translatable to the current crisis. But here are some which have focused on contemporary interpretations.

Earth by David Brin. Here the metaphor is a scientist-caused event which could destroy the earth, but the surrounding world-building of the near future is amazingly prescient for a novel written in 1991.

“Science in the Capitol” series by Kim Stanley Robinson. This trilogy envisions ever greater calamities being inflicted on Washington, D.C. In Forty Signs of Rain the region is flooded with rains of Biblical rage. The follow-up Fifty Degrees Below envisions near-Day After Tomorrow levels of cold. The final volume Sixty Days And Counting is just pure geo-engineering porn once world politicians realize Something Must Be Done.

While not directly climate change related, Ship Breaker by Paolo Bacigalupi takes place along the Louisiana coast after New Orleans has drowned and the remaining area has devolved to a scavenging economy similar to the ship breaking yards in India.

Markets are lower this morning on no real news. Bonds and MBS are up small.

Homebuilder Lennar reported better than expected earnings this morning with average sales prices up 6%, a decrease in gross margins and an increase in new orders of 10%. CEO Stuart Miller sees a “slow and steady” housing market improvement. He said the Fed rate hike was a sign of confidence in the economy.

Rob Chrisman discussed how TRID is impacting the non-agency markets. quotes one lender: “I see in your commentaries lots of feedback about TRID. Something else is happening and it appears, absent some quick changes in philosophy, the effect could be both a complete seizure of non-agency lending and possibly some firm’s very existence could be put in jeopardy. My firm has had 100% of the jumbo loans that we’ve sent for delivery rejected by our buyers. Yes – 100% – and we’re talking nearly 50 loans so far. Why? Every one had a TRID violation. Does that mean my firm screwed up and is alone on this? No. Two of the firms we sell to say they have purchased ZERO loans so far in December. ZERO. Why? Same reason. None of them were TRID compliant. The TRID rule is so severe, and so open for interpretation, and because the buyers are taking a zero defect approach – it is near impossible to manufacture a perfect loan from a TRID perspective. It’s clear to anyone in our business what could happen next. If I were a warehouse lender – I’d immediately cease funding non-agency loans. Same goes for any correspondent lender who doesn’t want a giant pipeline of unsaleable production. We’re large enough to be able to fund our unsaleable pipeline with cash. But many firms are not. What happens to a firm that has $5 million of cash on hand when its warehouse lender asks them to buy $6 million of jumbos (literally only 5 to 8 loans) off of the line? Game, set, match. Because TRID only affected new applications after 10/3 – the fundings are now only starting to be affected. This crisis is about to get real…”

Of course the reaction from the CFPB lawyers will undoubtedly be that these stooges in the mortgage banking industry just can’t get their act together. And they better start expanding credit in our targeted areas, or else!

The latest CoreLogic Market Pulse is out: They expect home prices to reach their previous peaks in mid 2017. Note that the FHFA House Price Index (which covers a subset of homes) is pretty much already there.

Fannie Mae reports that lenders are easing credit standards in their latest mortgage lender sentiment survey. They hope that easier credit will help mitigate the drop in home affordability.

Stocks are lower this morning, reversing the post FOMC rally. Bonds and MBS are up.

As expected, the Fed rose the Fed Funds target rate by 25 basis points. The statement generally focused on how the economy has improved. The biggest surprise in the statement and the projection materials was the forecast for rates going forward. The Fed lowered their expected Fed Funds range going forward. You can see the September versus December dot graphs below:

In response to the rate hike, banks hiked their prime rate to 3.5% from 3.25%. A lot of consumer debt, especially credit cards, are tied to the prime rate, which means consumers will feel the pinch.

The Philthy Fed Manufacturing Index fell to-5.9 from 1.9. while initial jobless claims fell from 282,000 to 271,000.

The Bloomberg Consumer Comfort Index rose to 40.9 from 40.1.

The Index of Leading Economic indicators fell from 0.6% to 0.4%.

Stocks are up this morning ahead of the FOMC meeting. The decision should be released around 2:00 EST. Given that this was the most telegraphed rate hike in history, I don’t necessarily expect a lot of volatility around the decision, however the language in the statement could always spook the markets. The consensus seems to be a hike of 25 basis points and very dovish language.

Housing starts increased to 1,173 million last month and building permits increased to 1,29 million. The increase in housing starts was in both single-fam and multi-fam, while the increase in permits was mainly in multi-fam. We still continue to under-build which is just creating more pent-up demand. We are in the seasonally slow period for housing, so I wouldn’t read too much into these numbers.

Mortgage Applications fell 1.1% last week as purchases fell 2,8% and refis rose 1.4%.

The strong dollar is still wreaking havoc on the manufacturing sector. Industrial Production fell 0.6% last month and capacity utilization fell to 77% from 77.5%. Manufacturing Production was flat.

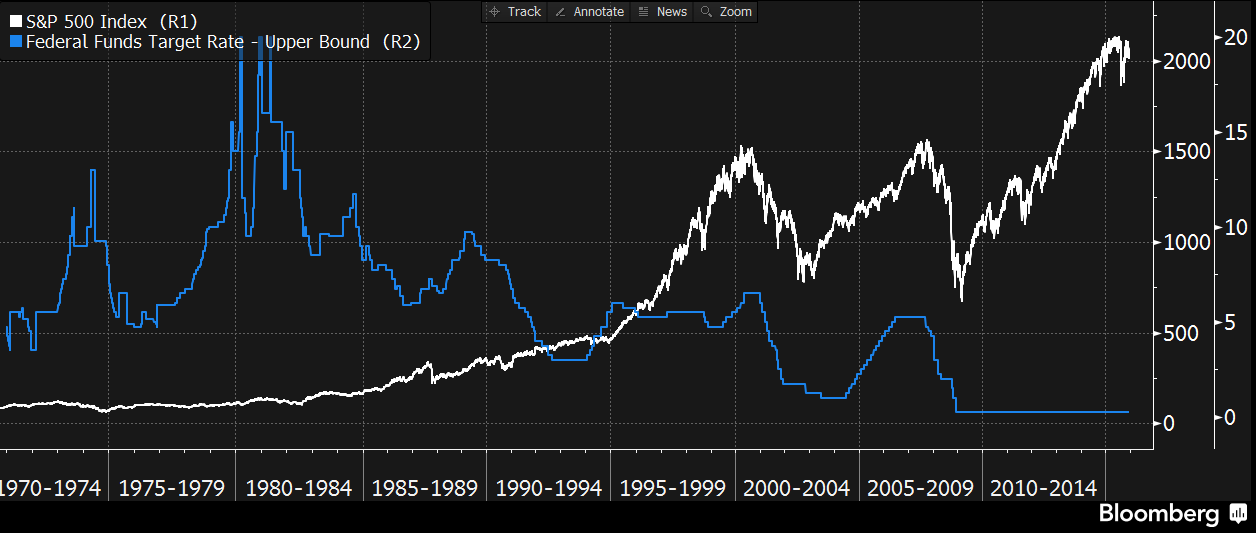

As the Fed begins to remove support from the market, stock market strategists are wondering what will happen to the stock market. Are current market levels a function of the Fed’s stimulus programs or are they supported by earnings and economic fundamentals? I can’t see a gradual tightening cycle collapsing the market, but it will mean that further increases in the market will have to be driven by earnings and economics and you can’t expect to see further multiple expansion. Dividends will become much more important. Here is a chart of the S&P 500 versus the Fed Funds rate over the past 45 years:

Interest rate cycles are long. The bull market in Treasuries started in 1982 or so is probably over, unless the economy rolls over again. The previous bear market in Treasuries ran from the mid-50s through the early 80s.

Note that the other central banks (especially Japan and Sweden) have tried to get off the zero bound, only to see rates fall back to 0% again. If that happens, then what? The Fed would have to raise its inflation target.

The story of Marty Whitman’s Third Avenue downfall. A value investor who simply didn’t fit with the current momentum-investor world. The current liquidity crunch in junk bonds is being attributed to Third Avenue’s Focused Credit Fund, which just put up gates preventing investor withdrawals. Daily liquidity, they promised.

Markets are higher this morning as oil and credit markets have an up day. Bonds and MBS are getting whacked.

There is no news in particular driving the rally in oil and other financial assets. Markets don’t go up in a straight line and they don’t go down in one either. Another possibility is that market participants are positioning themselves ahead of the Fed rate hike.

The problems in the credit markets are centered in distressed credits. The carnage is concentrated in the energy sector. For those keeping score at home, if you want to track how things are going, check out the Ishares high yield ETF HYG. The chart is below. You can see how it has been rolling over. I included the financial crisis years for perspective.

In economic data this morning, the consumer price index was flat on a month-over-month basis. Ex-food and energy, it increased 0.2%. On a year-over-year basis, it increased 2% ex- food and energy, which is right in line with the Fed’s target. The Bloomberg Real Average Hourly Earnings index increased to 1.6% annualized, up from an upward-revised 2.4% last week. Maybe, just maybe, wage inflation is upon us.

The Empire Manufacturing Index improved to -4.6, indicating that things are still tough in the manufacturing sector. Blame the dollar.

Homebuilder sentiment fell in December to 61 from 62. The index hit a 10 year high in October, so the sentiment is still pretty positive. The builders all reported pretty strong increases in orders and backlog, so it looks like 2016 could be a better year for the builders. The Spring Selling Season is about 2 months away. Note we will get numbers out of Lennar on Friday.

A survey of economists says that mortgage rates are going up. Probably a no-brainer, given the Fed is hiking rates. Does that mean a bad year for the housing sector? Not necessarily. Certainly an increase in rates is going to make lives tough for the refi shops. However if rates are rising because of a strengthening economy, that is probably great news for the purchase business as Millennials leave expensive rentals and buy property.

Mortgage fraud is making a comeback, according to CoreLogic. As credit loosens and purchase activity increases, you are going to see more risk of it.

Markets are lower this morning as oil continues to fall and problems at a high yield mutual fund begin to spill over.

No economic data today. The markets will be focused on the Fed and the evolving situation in distressed debt markets.

Marty Whitman’s Third Avenue Focused Credit Fund has suffered losses as the rout in high yield has reduced liquidity. Dodd-Frank has severely curtailed market-making operations at investment banks, and right now there are very few buyers of distressed credit as hedge funds face redemptions and investment banks cannot step in because of capital requirement. In fact, the regulators are considering additional steps to ensure a bank failure doesn’t bring down the entire financial system, which means that investment banks will probably de-risk further, making them even less likely to act as market-makers. This will be an interesting first test of a financial crisis in the new Dodd-Frank world.

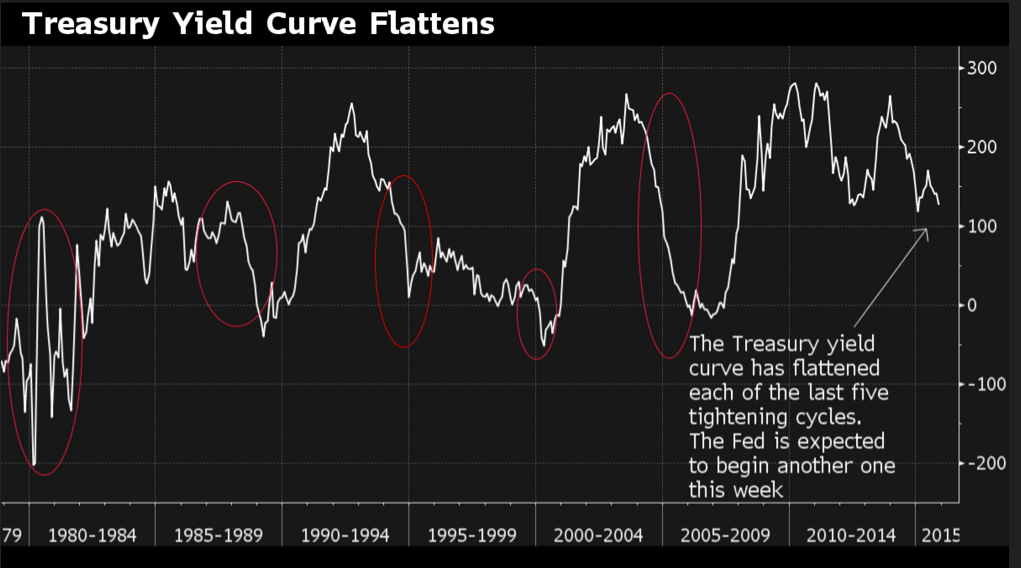

As a general rule, in credit crunches, the long bond rallies. You saw that on Friday, where the 10 year yield fell 10 basis points in spite of strong retail sales data. This week will be interesting between the evolving Third Avenue situation and the FOMC decision on Wednesday. LOs, expect bond market volatility this week. As a general rule, tightenings have not had a dramatic effect on mortgage rates. In fact, the yield curve has flattened during all the tightening cycles since 1979. Granted, these tightenings have taken place in context of a secular bull market in bonds, so take this analysis with a grain of salt. That said, unless the economy really starts taking off (and you start seeing wage inflation), chances are that the 10 year yield increases less than the amount of the rate hike. Note that CoreLogic is forecasting a 4.5% 30 year fixed rate mortgage by the end of 2016.

Mortgage loan performance has been improving, according to the OCC. Performing loans increased to 93.9% from 93% a year earlier. New foreclosures are down 22% YOY.

Ex GMAC Ally Financial is getting back in the mortgage business. Ally CEO said this about the move: “Don’t think of this as Ally going down the road of the old GMAC,” Brown said, referring to the home lending unit that brought Ally to the brink of collapse. The ironic thing is that the “new subprime” is auto loans, and that is Ally’s bread and butter these days. They are offering 8 year loans for new cars at rates at rates substantially below the 30-year fixed rate mortgage (think 3.5% range). Given that new cars depreciate like sushi, this is a very, very mispriced loan. If you are wondering why the Fed wants to get off the zero bound even in the face of zero inflation, there you go. Those sort of rates are a function of ZIRP and the impossibility of earning a decent rate of return. It would be ironic if the ne-er do well of mortgages had simply morphed into the ne-er to well of auto lending and we see a collapse in asset backed security liquidity.

Today, on the day Paul Krugman tells us that a bunch of politicians getting together and posing for photographs and brunching excessively has saved the planet, I feel motivated to ask this question:

What do people mean when they tell us, repeatedly, that climate is not weather? Or if you wonder how we’re predicting the climate and its effects 100 years from now, when we can’t reliably predict the weather 12 hours from now, and sometimes cannot accurately predict the weather as it’s happening, why does someone shake their head sadly about what a moron you are and explains: weather and climate are not the same thing, you sad, mentally-limited man-child.

I mean, why is the answer to the observation that we are not good at predicting the future for complex systems even in the near term essentially: “Well, the stock market is not the same thing as a large river with many tributaries”. I am aware that a watermelon is not a football, but if I want to say something about the shape of the football, the watermelon might still have some relevance. Just saying: “a watermelon is not a football” does not suddenly make a watermelon a trapezoid.

The official explanation is that climate is simple while weather is complex. Which, summarized thusly, seems an absurd statement. What they actually say, in their own words:

Weather is chaotic, making prediction difficult. However, climate takes a long term view, averaging weather out over time. This removes the chaotic element, enabling climate models to successfully predict future climate change.

… isn’t much better. There is very little evidence that climate models are able to successfully predict future climate change. And I find it interesting that a site that calls itself “skeptical science” blithely asserts that the climate models are predicting the future without the most basic evidence—the actual prediction of the future.

Also, you cannot reduce the complexity of a million or a billion inputs by averaging. Again, where are the skeptics (not to mention the mathematicians) at Skeptical Science? The assertion that climate can be accurately predicted (because averaging!) while the weather 12 hours from now, much less 3 days from now, cannot reminds me of that cartoon. You know the one.

I would also observe that every time there is a severe or unusual weather event, climate suddenly becomes the cause for the weather. Which, to me, begs the question why we cannot use our infinitely accurate climate models to start predicting the weather. Wait, I know! Because we’ve tried it, and it turns out those predictions were wrong, too.

I have come to the not unreasonable conclusion that climate ≠ weather in the context of anthropogenic climate change because we have ample, daily evidence that the behaviors of a complex system cannot be predicted with any degree of accuracy. The predictions of climate change are always far in the future, and evidence of inaccuracy of such predictions so far in the past they can be dismissed, or the data massaged. Harder the argue that, yes, it was sunny yesterday, even though the leaves are still wet from all the rain.

…

Tangentially related, even mainstream, largely liberal news organs like Time and Newsweek had to observe that the Paris talks were far less about climate or “saving the planet” than they were about making money, creating markets, and allocating capital.

Finally, How Climate Change Deniers Sound to Normal People:

Because anybody who doesn’t agree with me ideologically is abnormal. And sounds like an idiot to all the normal people. Conform, you abberants! Conform!