Posted on March 21, 2016 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are down.

Existing home sales fell 7.1% in February to an annualized pace of 5.08 million. Bad weather in the Northeast and the Midwest may have played a part. Sales are up 2.2% on a year-over-year basis. Lack of inventory and affordability remain the biggest issues. The median home price increased 4.4% to $210,800, and total inventory is about 4.4 month’s worth. All cash transactions were 25% of sales and investor purchases ticked up to 19%. The share of first time homebuyers slipped to 30% as affordability problems and worries about the economy kept many younger buyers on the sidelines.

Given the tight inventory, why aren’t homebuilders aggressively adding supply? Finding affordable land plots and skilled labor appear to be the problem. It is amazing that 10 years after the housing bust, we are still 25% below the long-term average in housing starts. I adjusted housing starts by population, and the graph below gives you an ideal of how much we have underbuilt. We still just barely reached the low of the 81-82 recession, which was the nastiest since the Great Depression. What is going on? My guess is that the government is the problem, via zoning laws in some localities, and general Washingtonian regulatory funk tying up the credit markets. Correcting whatever problem is holding back housing is the difference between a tepid, meh economy of 2% growth, and a recovery where we see 3% growth and wage inflation. It would be nice if someone running for office noticed this and said something. Unfortunately, they only acceptable answer these days is that the financial sector isn’t regulated and needs to be sat on more.

Investor demand for paper isn’t necessarily the issue either, as right now anyone who can fog a mirror can get an auto loan. It is the same old story: new entrants come into the market, take risks that the established players won’t take, and a new market takes off. One thing that is different these days is technology. Lower credit borrowers will get a GPS installed on their car (no, not a nice navigation system, but a transmitter that tells the lender where the car is). Lenders also now have the ability to disable the car remotely.

Filed under: Economy, Morning Report | 13 Comments »

Posted on March 21, 2016 by novahockey

I spent the weekend in Nashville for a college guys weekend. I did not know that it is bachelorette party central. But that’s neither here nor there.

Couple of things I heard of interest.

My uber drivers was a Trump voter. He’s always voted Democratic before, including for Obama who he likes very much. on of my friends in involved in Ohio Democratic politics. He is very concerned about Trump. A contacts is a lawyer who works on Muslim immigration issues. So the younger guys who work for him (all Muslims) are all Trump supporters. WTF is that about: “He can’t deport us or stop us from coming, but he can be more fair on the Israel matter.”

So there you go.

Filed under: Economy | 37 Comments »

Posted on March 17, 2016 by Brent Nyitray

Markets are lower this morning after the Fed maintained interest rates yesterday. Bonds and MBS are up small.

Surprising that bonds aren’t rallying harder this morning as European rates are moving aggressively lower, with the German Bund yield down 8 basis points to 24 bp. The dollar is getting hit a bit, which might explain the lack of follow-through.

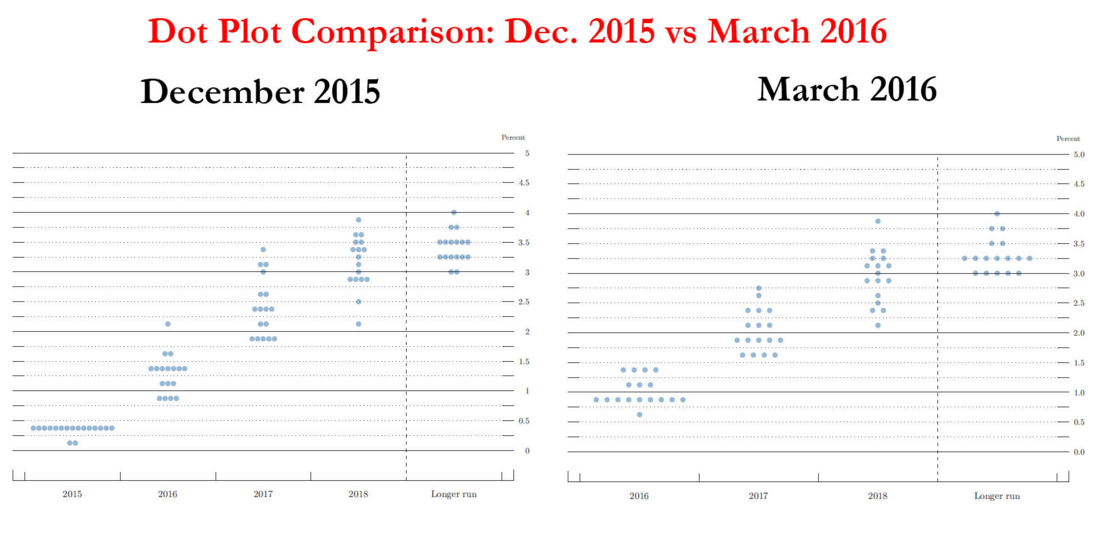

The Fed maintained interest rates and put out a relatively dovish statement. They took down their forecast for interest rates going out through 2018, which helped put a bid under bonds. In their updated economic forecasts, they took down their forecast for 2016 GDP to 2.2% from 2.4% and their estimate of 2016 inflation to 1.4% from 1.6%. They maintained their forecast for 4.7% unemployment. On the dot graph, the forecast looks for 2 more rate hikes this year, as opposed to their forecast of 4 in December.

After the FOMC statement, stocks and bonds rallied, with the 10 year yield dropping about 4 basis points and the 2 year yield dropping 11.

Initial Jobless Claims rose to 265k last week, while the Philly Fed Index improved.

The Bloomberg Consumer Comfort Index edged up last week to 44.3 from 43.8.

The Index of Leading Economic Indicators improved 0.1% in February, while job openings increased to 5.54 million.

CFPB Chairman Richard Cordray appeared before the House Financial Services Committee this morning. He said the CFPB will take a “sensitive” approach to TRID enforcement, meaning that if you are making a good-faith effort to comply, they won’t hammer you.

Filed under: Economy, Morning Report | 41 Comments »

Posted on March 17, 2016 by novahockey

Rep. Connolly was on WTOP this morning saying that those responsible for the failures at Metro need to be held accountable. I started my day with a laugh and thought you might get chuckle out of that too.

For those unfamiliar, see NPR

Also, if you are visiting the DC area, do not use Metro. It is not safe. It will never be safe.

Filed under: Economy | 22 Comments »

Posted on March 16, 2016 by Brent Nyitray

Markets are lower this morning after inflation comes in a little hotter than expected. Bonds and MBS are down.

The consumer price index fell 0.2% month-over month, but the core index, which excludes food and energy, rose 0.3% and is up 2.3% year-over-year. This makes the FOMC statement (and the press conference that follows) more significant this afternoon. Remember, the decision will be out at 2:00 pm EST, so expect some volatility in bonds around that time.

Bonds sold off on the CPI number and the more dramatic move was in the 2-year, not the 10-year. The 2 year yield increased 3 basis points on the news to .99%. Movements in the 2-year signify the market’s expectations about what the Fed is up to. The 10 year is more driven by longer-range economic forecasts. The 10 year was up, sold off on the news and is now flat on the day.

Housing starts rose to an annualized pace of 1.178 million in February and January was revised upward to 1.12 million. Building Permits fell however to 1.17million from 1.2 million. The drop in permits was driven by multi-family construction as single-fam remains slow and steady.

Mortgage Applications fell 3.3% as purchases rose 0.3% and refis fell 5.6%. Refis now constitute 55% of the total number of loans, down about 9 percentage points over the last month.

The strong dollar is still making life tough for manufacturers. Industrial production fell 0.5% month-over-month, while manufacturing production rose 0.2%. Capacity Utilization fell to 76.7%.

Marco Rubio is out after losing his home state of Florida to Donald Trump. John Kasich won Ohio, which keeps him in the race and makes him the de facto “Establishment Candidate. Ted Cruz is still in and he is probably going to split the Trump vote, while Kasich solidifies the establishment vote. Policy-wise, Kasich and Hillary are almost identical. Trump is warning that there will be riots if he has the delegates (or is close) and loses a contested convention. The convention is 4 months away. A lot can happen.

On the Democratic side, Hillary did well, so we can stick a fork in the #FeelTheBern hashtag.

Filed under: Economy, Morning Report | 92 Comments »

Posted on March 15, 2016 by Brent Nyitray

Markets are lower this morning as the dollar rallies and commodities fall. Bonds and MBS are up.

The FOMC meeting begins today. The decision will come out at 2:00 pm EST tomorrow, along with the new economic and Fed Funds forecasts. Here is Tim Duy’s take on the state of play. His take: while you could make an argument to tighten, the Fed still considers the bigger risks to be to the downside. The doves are ascendant on the Board.

Retail Sales fell 0.1% in February, although declining gasoline prices had a lot to do with it. Ex-autos and gas, they were up 0.3%. The control group, which also strips out building products was flat. The downward revisions to January got everyone’s attention however as the initial 0.2% estimate was revised downward to -0.4%.

Inflation at the wholesale level remains well below the Fed’s target. The Producer Price Index fell 0.2% in February as well. Ex-food and energy, it was flat on a month-over-month basis and is up 1.2% YOY.

The Empire Manufacturing Index rebounded smartly to .62 after a heavily negative start to the year.

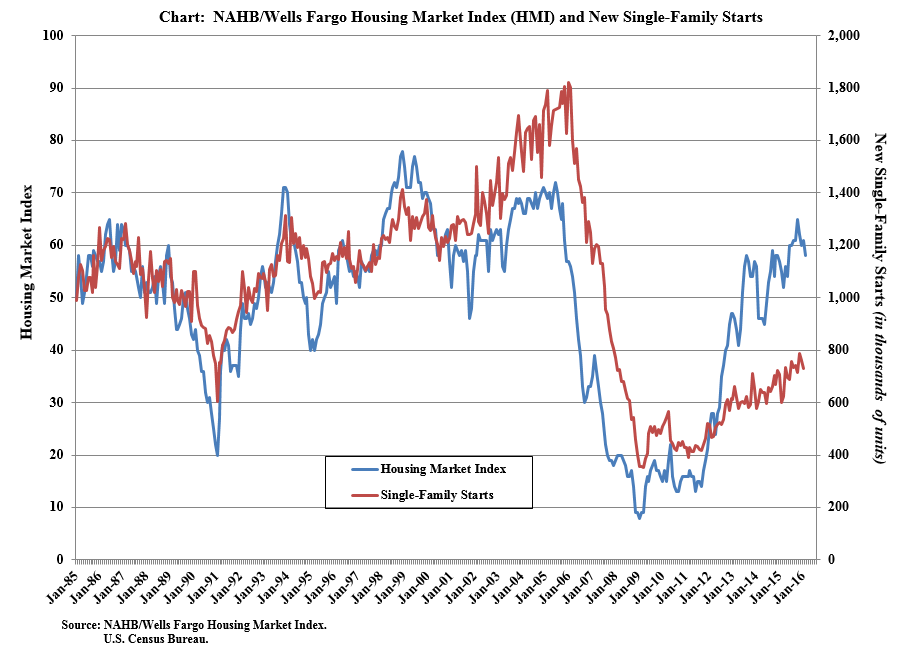

The NAHB Homebuilder Sentiment Index was unchanged at 58 in March. This is a 9 month low. A shortage of lots and labor continue to be the biggest headaches facing the sector. The builders have been able to drive the top line by raising prices, not by pushing volume. You can see below how the index has tracked versus housing starts. The divergence is as big as it has ever been.

Voters go to the polls in several states today, including Florida and Ohio, which are do-or-die races for Marco Rubio and John Kasich respectively. The Democratic side seems pretty much set at this point, unless Bernie Sanders pulls a free rabbit out of a hat.

Filed under: Economy, Morning Report | 20 Comments »

Posted on March 14, 2016 by Brent Nyitray

Stocks are lower this morning as oil gets roughed up. Bonds and MBS are up.

There is no economic data this morning, however the rest of the week looks pretty active, with retail sales, inflation data, housing starts, and industrial production. Of course we have the FOMC meeting Tuesday and Wednesday as well.

Mohammed El-Arian lays out his prediction for the FOMC meeting this week. Bottom line: No move in rates, and an emphasis on data-dependency. They will mention overseas weakness, but won’t make the statement that it will affect the US economy all that much. They will be sanguine on overall US data without becoming too hawkish on wages and inflation. So, generally a dovish take on things.

Note that the recent increase in US rates was driven at least partially by increases in Euro rates. That move seems to be unwinding (in other words, Euro rates are heading back down). This will probably help guide US rates lower as well, especially if we get a dovish statement on Wednesday.

Morgan Stanley is out with a call saying yields are going lower. Their forecast: 1.45% 10 year by the end of September. While the US economy is doing ok, the rest of the world is not. They think the next rate hike will be in December.

Why is the first time homebuyer sitting out? Freddie Mac attributes at least some of the reason to misconceptions about buying, specifically credit scores and down payments. Many young borrowers still believe you need 20% down and perfect credit to qualify for a mortgage. Freddie has launched their Real Estate Professionals Resource Center to give pros the lowdown on products that can get a young borrower into a home.

Filed under: Economy, Morning Report | 5 Comments »

Posted on March 10, 2016 by Brent Nyitray

Stocks are flat this morning after the ECB’s new stimulus plans earned a big yawn from the markets. Bonds and MBS are down.

Initial Jobless Claims came in at 259k, while the Bloomberg Consumer Comfort Index ticked up slightly to 43.8.

Filed under: Economy, Morning Report | 36 Comments »

Posted on March 9, 2016 by Brent Nyitray

Stocks are higher this morning as commodities rally and the market anticipates more stimulus from the European Central Bank tomorrow. Bonds and MBS are down small.

Mortgage Applications edged up 0.2% last week as purchases increased 4.2% and refis fell 2.3%. The 30 year fixed rate mortgage rose 6 basis points. We saw a big move up in ARM rates from 3.02% to 3.2%. In an environment where the yield curve is flattening, switching from an ARM to a 30 year fixed is the trade to make.

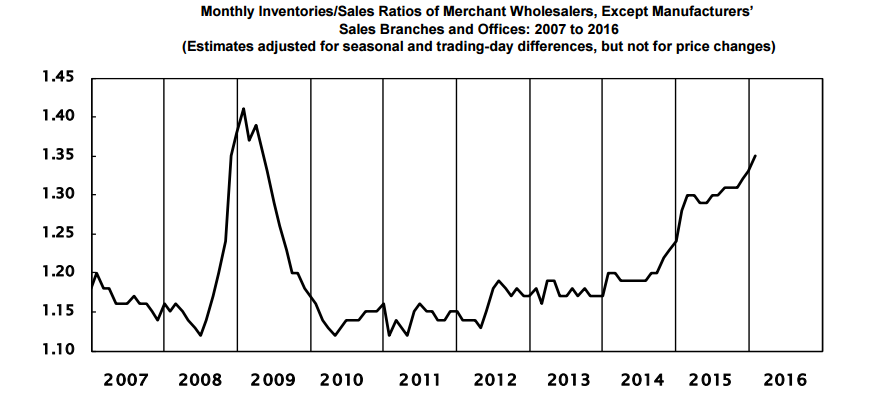

Wholesale sales fell 1.3% last month while inventories built up 0.3%. The inventory-to-sales ratio is 1.35 month’s worth, which is the highest since April of 2009. This is a negative sign for the economy going forward, as inventory build adds to GDP, and a buildup essentially “borrows” growth from future quarters. While this number doesn’t carry the same weight it did 20 years ago, it still matters.

Marco Rubio had a tough day yesterday. John Kasich is looking more and more like he could be the “establishment candidate.” Bernie Sanders beat Hillary in Michigan, as anti-trade populism resonates deeply in the hard-hit rust belt.

Consumers are becoming a touch less bullish on future home price appreciation, according to the latest Fannie Mae National Housing Survey. They anticipate that home prices will appreciate 1.7% next year, as opposed to 2.2% last month. We are certainly seeing some signs of softness in the oil states as well as the high end. Their view on the economy is about the most negative it has been since the big equity sell-off in August. 56% believe the economy is on the wrong track, and only 37% believe the economy is on the right track. This statistic explains the appeal of Sanders and Trump these days, two candidates who would ordinarily get zero traction.

Global financial markets are forecasting that the age of ZIRP will be with us for 10 years or more. Sound far-fetched? Japan has been at 0% interest rates for over 20 years. Interest rate cycles are long. While the US may not be in the sort of deflationary trap that Europe and Japan are in, relative value trading will help keep a lid on rates going forward. In fact, the US may be more at risk of future asset bubbles than deflation.

Filed under: Economy, Morning Report | 21 Comments »

Posted on March 8, 2016 by Brent Nyitray

Stocks are lower this morning on bad export numbers out of China. Bonds and MBS are up.

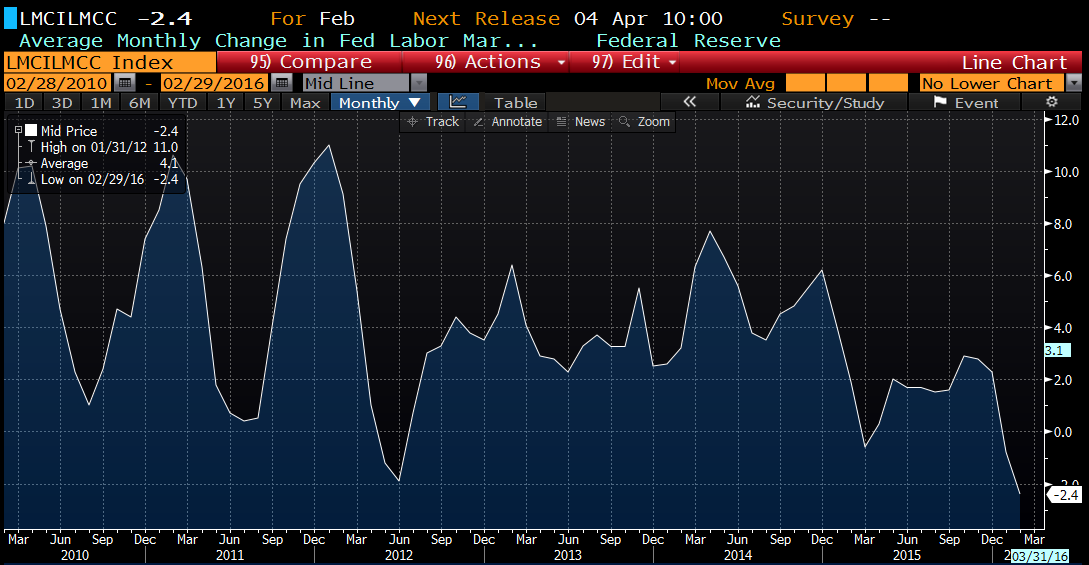

The US Labor Market Conditions Index fell in February, This is a relatively new index created of 19 different labor market indicators. Not sure what caused the recent drop in the index, as most of the big indicators are positive. Perhaps the disappointing wage growth in the last jobs report is causing it. Certainly the labor market does not seem to be the worst in four years..

Small Business Optimism hit a 2 year low, according to the NFIB. Worryingly, job creation fell for the first time in quite a while, as small businesses shed about .12 workers per firm. The difficulty in finding qualified workers also fell in importance, although it is still elevated. Washington remains the biggest impediment, with taxes and red tape occupying the #1 and #2 concerns for small business. The report summed it up this way: “Overall, a “ho hum” outcome, confirming that the small business sector is not headed up with any strength, just treading water waiting for a good reason to invest in the future.”

The big drop in interest rates has bumped up the refinanceable population to 6.7 million borrowers from 5.2 million last month, according to Black Knight Financial Services. An additional 15 basis point drop in rates would add another 2.1 million borrowers. This data is based on mid-February numbers, with a FHLMC 30 year rate of 3.65%. Just another reason why 2016 might be a little better than expected.

Foreclosure activity continues to fall, according to CoreLogic. Foreclosure inventory is down 21.7% to 456,000 homes, and completed foreclosures fell 16% in January. Serious delinquencies also fell to 1.2 million mortgages, the lowest since 2007. Foreclosure activity is making the home price recovery more durable: “The improvement in distressed properties continues across the country in every state which is contributing to the lack of stock of available homes and resulting price escalation in many markets,” said Anand Nallathambi, president and CEO of CoreLogic. “So far the trend toward lower delinquency and foreclosures has been immune from shocks from such things as the collapse in oil prices attesting to the durability of the housing recovery.”

Filed under: Economy, Morning Report | 21 Comments »