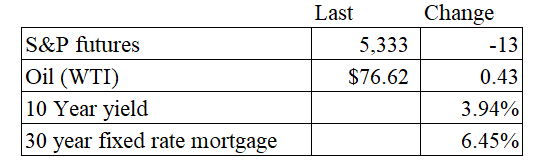

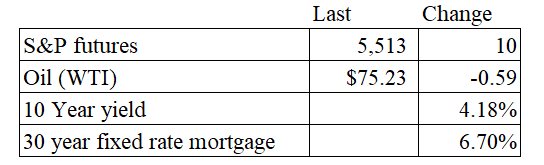

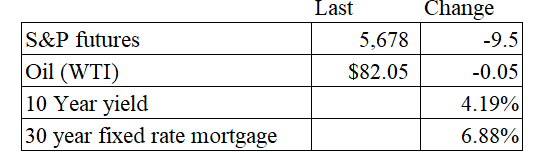

Stocks are lower as we finish up a turbulent week for markets. Bonds and MBS are up.

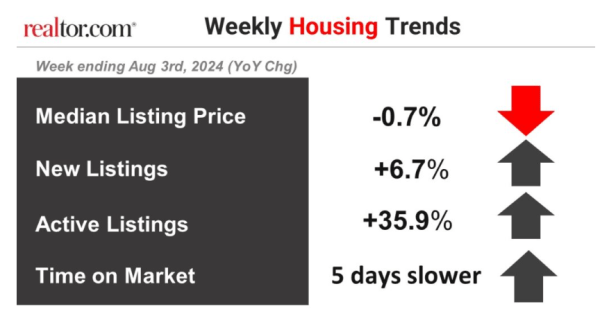

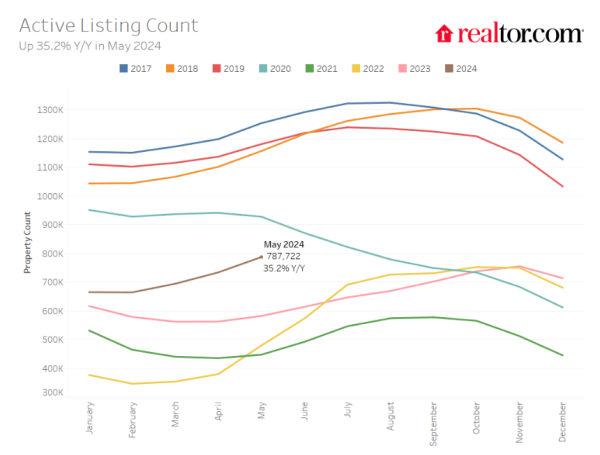

Active for-sale inventory rose 36% YOY, according to Realtor.com. The median listing price is down 0.7% YOY, while year-to-date listing prices are flat. Overall, we are getting to a more balanced home market.

The total value of US residential real estate rose to $49.6 trillion, according to research from Redfin. “The value of America’s housing market will likely cross the $50 trillion threshold in the next 12 months as there are not enough homes being listed to push prices down,” said Redfin Economics Research Lead Chen Zhao. “Mortgage rates have started falling, but many potential sellers and buyers are waiting to make a move, meaning we are likely to continue seeing a pattern where prices slowly tick up. That’s great news for the millions of American homeowners who see their equity rising, but first-time buyers are going to keep finding it tough to find an affordable home.”

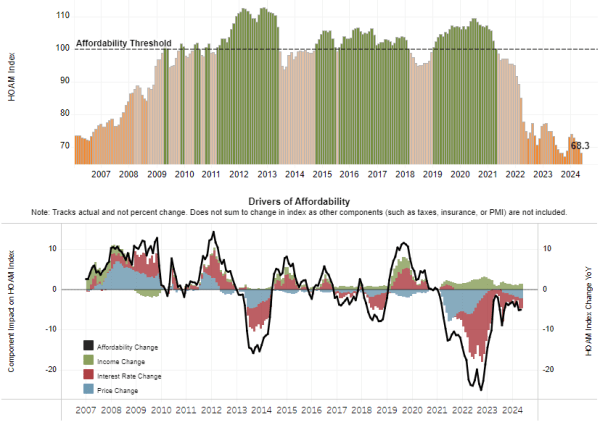

Affordability continues to be terrible however, according to the Atlanta Fed:

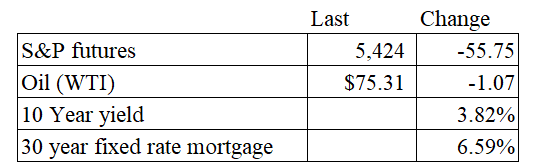

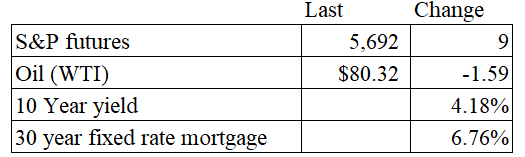

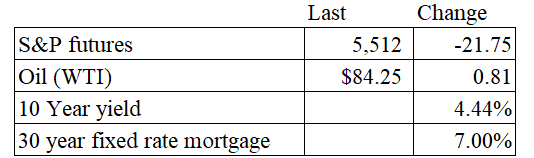

Stocks are lower this morning as tech continues to sell off. Bonds and MBS are up big on the disappointing jobs report.

The Bank of England cut rates this morning, which is also helping put global sovereign yields lower.

The economy added 114,000 jobs in July, which was below the Street estimate of 180,000. June was revised downward from 206,000 jobs to 179,000. The unemployment rate ticked up from 4.1% to 4.3%. The number of unemployed people ticked up to 352,000.

Average hourly earnings rose 3.6% YOY, and June’s 3.9% number was revised downward to 3.8%.

Overall, this was a disappointing jobs report, and strengthens the case for a September rate cut. The 10 year bond yield moved decisively lower, falling 14 basis points in the immediate aftermath of the report.

The manufacturing economy continues to deteriorate, according to the ISM Manufacturing Index. The index contracted for the fourth month in a row, and 20 out of the last 21 months. Employment contracted by quite a bit, however prices are still rising. “Demand remains subdued, as companies show an unwillingness to invest in capital and inventory due to current federal monetary policy and other conditions. Production execution was down compared to June, likely adding to revenue declines, putting additional pressure on profitability. Suppliers continue to have capacity, with lead times improving and shortages not as severe. Eighty-six percent of manufacturing gross domestic product (GDP) contracted in July, up from 62 percent in June. More concerning: The share of sector GDP registering a composite PMI® calculation at or below 45 percent (a good barometer of overall manufacturing weakness) was 53 percent in July, 39 percentage points higher than the 14 percent reported in June. Notably, all six of the largest manufacturing industries — Machinery; Transportation Equipment; Fabricated Metal Products; Food, Beverage & Tobacco Products; Chemical Products; and Computer & Electronic Products — contracted in July,” says Fiore.

Private residential construction spending fell for the second straight month in June, largely driven by a decline in single family building. We had been seeing a shift in building from multi-family to single family for the past 18 months or so, but now both are declining.

Stocks are higher this morning as earnings continue to come in. Bonds and MBS are down small.

The US Treasury expects to borrow $740 billion in the third quarter, which is down about $106 billion from the April estimate. It expects to borrow $565 billion in Q4.

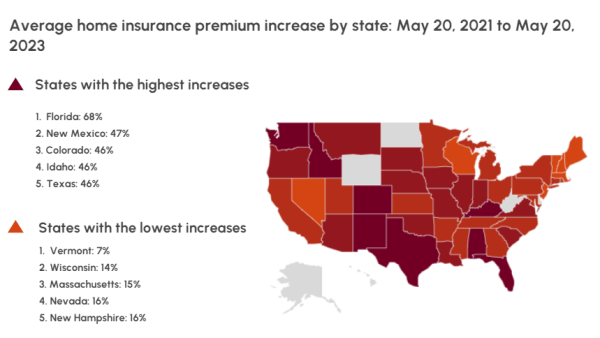

Home insurance premiums rose 21% last year. “The levels of risk and the kinds of hazards that a property can be exposed to are massively changing,” said Carlos Martín, director of the Remodeling Futures program at the Joint Center for Housing Studies of Harvard University.

“And right now there’s a lot of confusion, not just among the homeowners, but also among the insurers about how they should be pricing this actuarially,” he said.

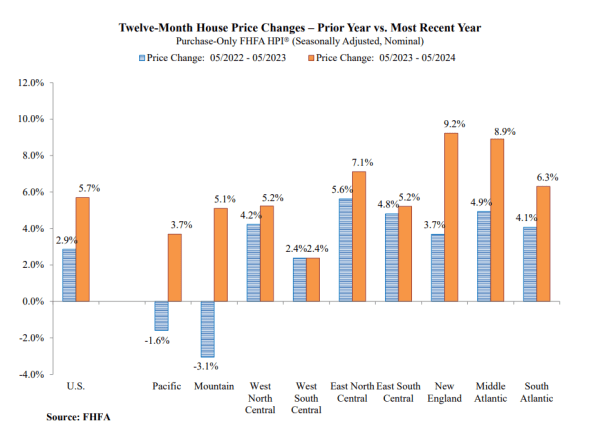

Home price appreciation was flat in May, according to the FHFA House Price Index. Over the past year, home prices rose 5.7%. “U.S. house price movement was flat in May,” said Dr. Anju Vajja, Deputy Director for FHFA’s Division of Research and Statistics. “The slowdown in U.S. house price appreciation continued in May amid a slight rise in both mortgage rates and housing inventory.”

The hot markets of the pandemic era are fading, while the post-2008 laggards are showing the most growth.

The Case-Shiller index showed a 5.9% annual gain in May. “While annual gains have decelerated recently, this may have more to do with 2023 than 2024, as recent performance remains encouraging,” says Brian D. Luke, Head of Commodities, Real & Digital Assets. “Our home price index has appreciated 4.1% year-to-date, the fastest start in two years. Covering the six-month period dating to when mortgage rates peaked, our national index has risen the past four months, erasing the stall experienced late last year. Collectively, all 20 markets covered continue to trade in a homogeneous pattern. Coming into the 2024 presidential election, traditional red states are in a dead heat with blue states, both averaging 5.9% gains annually.

“The Big Apple returned to the top of the leader boards, toppling San Diego from its six-month perch. New York’s 9.4% annual return outpaced San Diego and Las Vegas, by 0.3% and 0.7%, respectively. All 20 markets observed annual gains for the last six months. The last time we saw that long a streak was when all markets rose for three years consecutively during the COVID housing boom. This rally pales in comparison in both duration and annual gains, with above trend growth of 6.2%. The waiting game for the possibility of favorable changes in lending rates continues to be costly for potential buyers\ as home prices march forward.”

Stocks are lower this morning after lackluster earnings from Tesla. Bonds and MBS are flat.

Existing home sales fell 5.4% last month to a seasonally-adjusted annual rate of 3.89 million. “We’re seeing a slow shift from a seller’s market to a buyer’s market,” said NAR Chief Economist Lawrence Yun. “Homes are sitting on the market a bit longer, and sellers are receiving fewer offers. More buyers are insisting on home inspections and appraisals, and inventory is definitively rising on a national basis. Even as the median home price reached a new record high, further large accelerations are unlikely,” Yun added. “Supply and demand dynamics are nearing a balanced market condition. The months supply of inventory reached its highest level in more than four years.”

The median home price rose to 426,900, which was a 4.1% increase from a year ago. The first time homebuyer share fell from 31% to 29%, while investor purchases fell from 18% to 16%. The 3.9 million pace of existing home sales is pretty consistent for a housing recession. To put that number into perspective, we did something like 5.3 million in 2019.

Fannie Mae’s latest housing forecast is out. They see the 30 year fixed rate mortgage ending the year at 6.7%, and gradually falling to 6.2% by the end of 2025. Home price appreciation is expected to remain in the 6% range before falling into the 3% range in 2025. They expect to see 25 basis points in rate cuts this year and another 75 bp in 2025. The core PCE inflation rate is expected to fall to 2.7% this year and 2.3% next year.

PennyMac reported earnings that disappointed the Street. The company acquired $22.5 billion in loans in Q2, which was up 6% on a year-over-year basis. On the earnings conference call, CEO David Spector was asked about when we will start seeing more refi activity:

“Look, I think it’s a gradual decline down. I think if you look at originations post COVID, we kind of jumped and kind of ran through loans with 5% handle. And I think it’s really in the 6% to 7% range where you see a lot — and even north of 7%, where you see a lot of opportunity. It’s going to be — the way I think about it is it’s going to be the slow grind down. I think when rates get to 6.5%, that’s where it really picks up steam.

And I think at 6%, you’re in what I would deem a really robust refi market because it’s not just the existing first that are in the money. You could have loans that are 4% and 5%, taking out debt consolidation, cash refinance to either pay off existing HELOCs or closed-end seconds or other forms of debt. And so it’s really a function of what’s behind the first lien that helps drive the refinanceability. But I continue to believe that it’s 10-year around 3.75%, mortgage is down 50 basis points, that it really is to me, that’s the signal of a true new market or new phase of the refinanceability.”

Mortgage applications fell 2.2% last week as purchases fell 4% and refis rose 0.3%. “Mortgage rates continued to ease, with the 30-year fixed rate dipping to 6.82 percent, the lowest level since February 2024,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Refinance applications were up, driven by conventional and FHA application activity, as some borrowers took the opportunity to act. Furthermore, the conventional refi index was at its highest level since September 2022. Purchase applications decreased as ongoing affordability challenges persist with rates at their current levels and with home-price appreciation still strong in many markets.”

Stocks are higher this morning as earnings continue to come in. Bonds and MBS are up.

Jerome Powell spoke yesterday, and said that the Fed isn’t going to wait until inflation hits its 2% target before easing. “The implication of that is that if you wait until inflation gets all the way down to 2%, you’ve probably waited too long, because the tightening that you’re doing, or the level of tightness that you have, is still having effects which will probably drive inflation below 2%,” Powell said.

He also acknowledged the recent good inflation reports: “What increases that confidence in that is more good inflation data, and lately here we have been getting some of that,” he said.

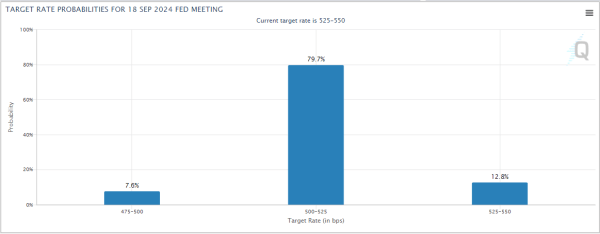

The September Fed Funds futures now see a rate cut as a certainty.

Retail Sales were flat month-over-month in June, according to the Census Bureau. They rose 2.3% on a year-over-year basis. Since these numbers are not adjusted for inflation, real retail sales fell.

Non-store retailers (i.e. online shopping) and restaurants saw big increases. If you strip out motor vehicles, sales rose 0.4% MOM and if you exclude vehicles and gasoline, they rose 0.8%.

May’s retail sales numbers were revised upward.

When inflation rises, politicians invariably return to one of the dumbest ideas ever put forward – price caps. The idea is that we beat inflation by simply putting a ceiling on prices. Of course this has unintended consequences – the most common is that price controls create shortages – but those effects take time to play out, so it can often give a politician the veneer of “doing something” long enough to get through the election cycle before the unintended effects are visible.

I mention this because the Biden Administration wants to impose rent control nationwide, capping annual price increases at 5%. Of course since this doesn’t affect the costs that landlords bear, it will act to lower cap rates for multi-family developments, which will discourage investment.

Needless to say, industry groups oppose this. The MBA said “There are endless examples in localities in America and around the world that prove that rent control is a counter-productive policy idea that ultimately harms renters by distorting market pricing, discouraging new construction, and degrading the quality of rental housing. While the odds are stacked against this proposal ever passing Congress, a federal rent control law would be catastrophic to renters and our nation’s rental housing market.

The measure requires Congressional approval, so has little-to-no chance of getting passed, let alone in an election year, but it does demonstrate yet again that bad ideas are like Freddy Kreuger – they keep coming back

Stocks are lower despite a good CPI print. Bonds and MBS are up.

Inflation fell 0.1% MOM and 3.0% year-over-year. The Street was expecting an increase of 0.1%, so this was a good surprise for the bond market. Energy prices fell overall, which was offset by increases in shelter. Used Car prices were down 10% on a year-over-year basis.

If you strip out food and energy, prices rose 0.1% month-over-month and 3.1% year-over-year. This was again below expectations. The bond market reacted positively to the report, with the 10 year yield falling over 10 basis points to below 4.2%.

The September Fed Funds futures now see a 80% chance of a rate cut at the September meeting.

Over the past year, we have seen a lot of eye-popping payroll gains, which get revised downward in later months. The average downward revision this year has been 50,000 per month. The typical headline number has been around 275k, so this is a pretty big downward revision. What is going on?

The explanation may be that the numbers are less reliable due to lower response rates. The government estimates payroll growth by sending out questionnaires to businesses who report how many people they hired during the month. It goes out to some 600,000 businesses nationwide.

The response rate fell to a 21 year low in 2023, and has fallen even more this year. If less businesses respond to the survey, the less accurate it is. And with the big downward revisions, the labor market might be worse off than it initially appears.

One recent phenomenon has been the posting of “ghost jobs” which are job listings where the company really doesn’t intend to hire any one. They are there for HR window dressing and resume collection, but they don’t represent real hiring needs. If this behavior is affecting the JOLTs job openings number, then that is another employment statistic that is hiding a broader deterioration in the labor market.

Stocks are flattish as we head into earnings season. Bonds and MBS are up small.

The week ahead will have some important events, with Jerome Powell heading to the Hill on Tuesday and Wednesday for his semi-annual Humphrey-Hawkins testimony. We will get the consumer price index on Thursday, and earnings season kicks off with the big banks reporting on Friday.

We are seeing for-sale inventory build, however we are still below pre-pandemic levels, according to research from Realtor.com. For-sale inventory rose 35% on a year-over-year basis, however median prices were flat. This might represent a mix shift, as prices rose on price per square foot basis.

While inventory is up 35% YOY, it is still about 35% below 2019 levels. Inventory is getting closer to balance in the South and West, where we saw a building boom over the past few years. Regions which saw muted growth post-2008 (lots of the Northeast and Midwest) are now catching up to the rest of the country.

Mark Zandi has come out in favor of rate cuts.

It’s time for the Federal Reserve to cut interest rates. That’s the message in today’s jobs report for June. Unemployment while still low is steadily notching higher. Job and wage growth while still strong are steadily moderating. The Fed has met its full employment mandate.…

Stocks are lower this morning on no real news. Bonds and MBS are up small.

Jerome Powell is speaking at 9:30 this morning.

The manufacturing economy contracted again in June, according to the ISM Manufacturing Report. “Demand remains subdued, as companies demonstrate an unwillingness to invest in capital and inventory due to current monetary policy and other conditions. Production execution was down compared to the previous month, likely causing revenue declines, putting pressure on profitability. Suppliers continue to have capacity, with lead times improving and shortages not as severe. Sixty-two percent of manufacturing gross domestic product (GDP) contracted in June, up from 55 percent in May. More concerning is the share of sector GDP registering a composite PMI® calculation at or below 45 percent — a good barometer of overall manufacturing weakness — was 14 percent in June, 10 percentage points higher than the 4 percent reported in May.”

Importantly, the prices index fell pretty dramatically, which helps support falling inflation.

The manufacturing economy expanded slightly in June, according to the S&P US Manufacturing PMI. New orders appear to be increasing, and input costs remain an issue. That said, business confidence hit a 19 month low. “Factories have been hit over the past two years by demand switching post-pandemic from goods to services, while at the same time household and business spending power has been diminished by higher prices and concerns over higher-for-longer interest rates. These headwinds persisted into June, accompanied by heightened uncertainty about the economic outlook as the presidential election draws closer. Business confidence has consequently fallen to the lowest for 19 months, suggesting the manufacturing sector is bracing itself for further tough times in the coming months.”

Stocks are higher this morning on no real news. Bonds and MBS are down.

The week ahead will have a lot of real estate data, with home prices and pending home sales. We will get the third revision to Q1 GDP and get personal incomes / outlays on Friday which will give us the all-important PCE Price Index.

Existing home sales fell 0.7% MOM in May, according to NAR. This is a decline of 2.8% compared to a year ago. The median home price rose 5.8% on a YOY basis to $419,300. There are about 1.28 million units for sale, which represents a 3.7 month supply at the current sales pace. A balanced market is 6 – 7 months’ worth of supply.

“Eventually, more inventory will help boost home sales and tame home price gains in the upcoming months,” said NAR Chief Economist Lawrence Yun. “Increased housing supply spells good news for consumers who want to see more properties before making purchasing decisions.” “Home prices reaching new highs are creating a wider divide between those owning properties and those who wish to be first-time buyers,” Yun added. “The mortgage payment for a typical home today is more than double that of homes purchased before 2020. Still, first-time buyers in the market understand the long-term benefits of owning.”

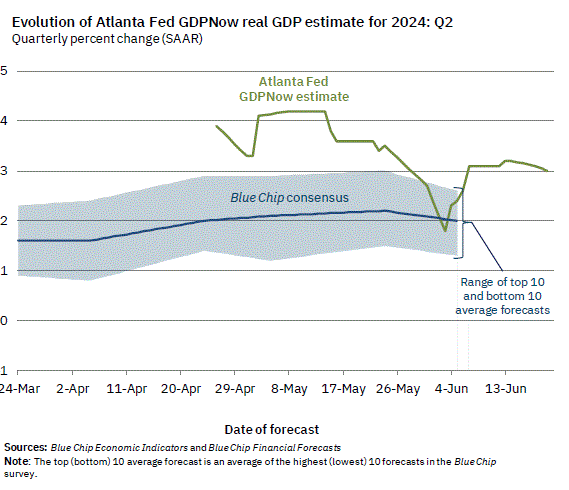

Q2 GDP is tracking around 3%, according to the Atlanta Fed GDP Now model.

Stocks are higher as markets digest the Fed decision. Bonds and MBS are down small.

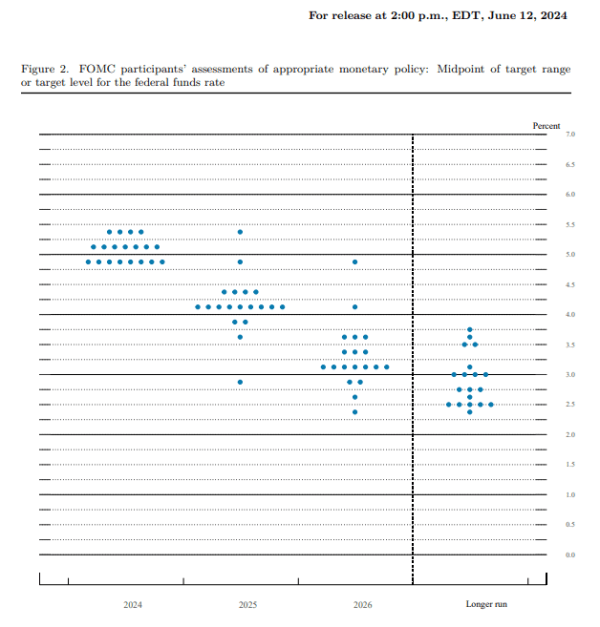

As expected, the Fed maintained the Fed Funds rate at current levels. “Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. In recent months, there has been modest further progress toward the Committee’s 2 percent inflation objective.” In the May statement, the Fed said that “In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.” So there is a bit of an improvement in the language.

The dot plot showed the Committee expects to cut rates once this year. The economic forecasts didn’t move much, however they did bump up their inflation forecasts a tad, with the headline PCE forecast increasing from 2.4% to 2.6% and the core rate increasing from 2.6% to 2.8%.

We have another benign inflation report, with the producer price index actually falling 0.2% on a month-over-month basis and 2.2% on a year-over-year basis. About 60% of the decline was due to falling gas prices. Ex-food and energy, the index was flat and rose 2.3% on a YOY basis. Both numbers were below expectations.

More evidence of a weakening job market: Initial Jobless Claims rose to 242k last week. This is the highest level since August of last year.

The median home sale price in the US hit a record last week, according to Redfin. The median sale price hit $394,000 which is up 4.4% on a year-over-year basis. Asking prices appear to be leveling off however. The median mortgage payment fell to $2,829 due to falling mortgage rates. “The latest inflation report is good for homebuyers because it has already sent mortgage rates down, though this week’s Fed meeting will temper mortgage-rate declines,” said Chen Zhao, Redfin’s economic research lead. “But on the other side of the coin, if lower mortgage rates bring back more demand than supply, that could erase the possibility that home-price growth softens, and push prices up even further. Lower rates and higher prices may ultimately cancel each other out when it comes to homebuyers’ monthly paym