Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1314.8 | -5.3 | -0.40% |

| Eurostoxx Index | 2142.0 | -1.4 | -0.07% |

| Oil (WTI) | 82.79 | -0.5 | -0.64% |

| LIBOR | 0.468 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 82.31 | -0.115 | -0.14% |

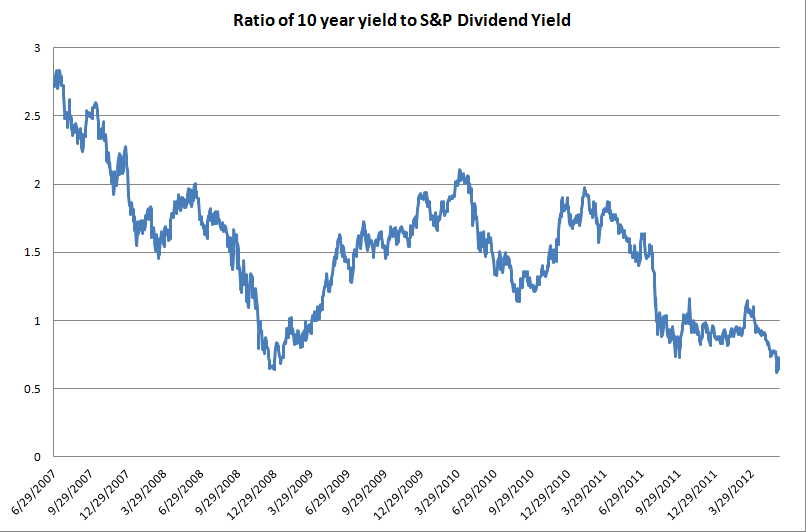

| 10 Year Govt Bond Yield | 1.68% | 0.01% | |

| RPX Composite Real Estate Index | 179.1 | 0.2 |

Markets are lower this morning on disappointing retail sales data. April numbers were also revised downward. The Producer Price Index showed inflation at the wholesale level remains under control. Bonds and MBS are lower in spite of the soggy tape. Jamie Dimon gets his close-up today in front of the Senate Banking Committee.

The Lender Processing Services Home Price Index rose .9% in March. This was the second consecutive monthly increase in the seasonally-adjusted index since 2006. The increase was broad-based geographically, with increases in almost every MSA. That said, March sales volume was extremely low – like mid-90s low – as inventory dried up. I mentioned a WSJ article yesterday that attempted to address the question why volumes are so low if shadow inventory is so high. Negative Equity is largely the culprit. Also in the report, distressed sales (short sales / foreclosures) made up 40% of the transactions. CNBC notes that new laws like Nevada’s foreclosure-reform law are having the unintended (maybe not) consequence of delaying foreclosures and delaying the market-clearing process. California is debating a “Homeowner Bill of Rights” as well. The net result is that the supply of foreclosed properties will continue to be artificially held back and helps explain the low volume of transactions.

In a story that is guaranteed to hit a lot of ideological nerves, the Washington Post profiles a loan officer who claims Wells Fargo steered minority borrowers into no-doc subprime loans. Needless to say, Wells disagrees claiming they never did no-docs in the first place and that the borrowers wouldn’t have qualified for prime loans anyway. Ironically, she is now in the mortgage-relief business, which has come under scrutiny by the FTC for charging up-front fees and not delivering anything. Needless to say, this article will produce a lot of heated CRA vs bankster debate.

Filed under: Uncategorized | 14 Comments »