Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1358.2 | 0.6 | 0.04% |

| Eurostoxx Index | 2309.4 | 17.3 | 0.75% |

| Oil (WTI) | 85.75 | 2.0 | 2.39% |

| LIBOR | 0.461 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 81.93 | 0.057 | 0.07% |

| 10 Year Govt Bond Yield | 1.59% | 0.00% | |

| RPX Composite Real Estate Index | 182.8 | 0.3 |

Markets are flat ahead of the 4th of July on a holiday-shortened day. Bonds will close at 1:00 pm, and stocks will close at 2:00. There is very little economic data this morning. We have the jobs report later this week and then earnings season kicks off with Alcoa on Monday.

Bob Diamond is out at Barclay’s after political pressure from the LIBOR pricing scandal forced him to resign. He will be in front of Parliament tomorrow to address questions regarding the scandal and is prepared to fight back with claims the regulators knew what was going on and didn’t object for fear the banking system would be further destabilized if the markets knew the truth. Needless to say, the politicians are shocked to find gambling in this establishment.

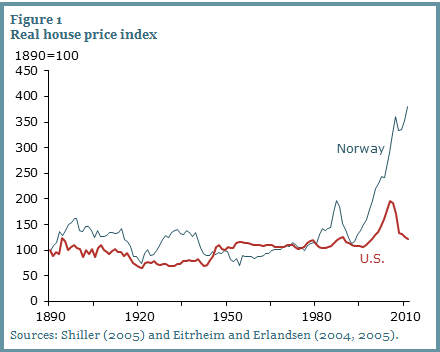

The Federal Reserve Bank of San Francisco has an interesting paper on housing bubbles. Needless to say, they let the Fed off the hook, and continue with the standard academic “angels dancing on the head of a pin” argument about how to identify a bubble. But that isn’t the most interesting part of the paper. Most people know that Scandinavia experienced a massive housing bubble in the late 80s. When it burst, many banks failed, and Sweden effectively nationalized its banking system.

However, in contrast to the Japanese experience, house prices in Norway had a V-shaped rebound and have subsequently passed their old peak by 130%. This has caused the household debt to income ratio to increase to 210%. By way of comparison, that ratio peaked at 130% in 2007 here. If oil prices collapse and that bubble bursts, Norway will undoubtedly hit the wall. It will be interesting to see how that government reacts. But the more interesting observation is how you can have a second bubble so soon after one bursts.

The US government is pulling out all the stops trying to put the air back into the housing bubble. Most people assume they will fail. Norway shows that it is possible they may be able to pull it off.

Right now, all the pundits and talking heads are discussing how smart the Scandinavians have been with their “smart regulation.” and how we should emulate them. Similarly, everyone loved the US model in the late 90s and everyone thought the Japanese had cracked the code in the 80s. Often times, the countries that are the flavor of the day just happen to be in the glory days of a bubble that will eventually burst. That prosperity is never permanent.

Have a happy 4th of July.

Filed under: Morning Report | 14 Comments »