Vital Statistics:

| |

Last |

Change |

Percent |

| S&P Futures |

1917.9 |

-3.9 |

-0.20% |

| Eurostoxx Index |

3240.1 |

-7.7 |

-0.24% |

| Oil (WTI) |

102.5 |

0.1 |

0.06% |

| LIBOR |

0.227 |

0.000 |

0.11% |

| US Dollar Index (DXY) |

80.49 |

-0.150 |

-0.19% |

| 10 Year Govt Bond Yield |

2.55% |

0.02% |

|

| Current Coupon Ginnie Mae TBA |

106.5 |

0.1 |

|

| Current Coupon Fannie Mae TBA |

105.5 |

0.1 |

|

| BankRate 30 Year Fixed Rate Mortgage |

4.18 |

|

|

Stocks are down (and bonds are up) after the weak ADP jobs report, which is signalling a weak nonfarm payrolls number on Friday.

ADP payrolls came in at 179k, below the 210k expectation. The Street is forecasting 215k jobs for Friday’s report. FWIW, the ADP report has been downright lousy at predicting the big number lately (notwithstanding last month), so I wouldn’t read too much into it.

Mortgage applications fell 3.1% last week, even though mortgage rates fell a couple bps. Purchasese fell 3.6%, while refis fell 2.9%.

The final revision for first quarter productivity came in at -3.2%. Unit labor costs rose 5.76%. Not sure how much of that was driven by obamacare / bad weather. Flattening productivity growth could be a good thing generally, as it means employers have squeezed just about all they can get from current employees and will need to hire more (or spend more on CAPEX). Either one is bullish for the economy.

The ISM Services index jumped to 56.3 in May, versus 55.2 in April and expectations of 55.5. Not quite post recession highs, but close. So we continue with the pattern of strong data, weak data.

The Markit US Services PMI and composite PMI were both strong, although a little weaker than April. Still a 58 handle is a good number regardless.

The census bureau has a

cool application where you can find out all about trends in home construction – things like typical number of bedrooms, number of bathrooms, square footage, amenities. One thing that jumps out is that the luxury end is doing better – we are building less homes under 1800 square feet, and the big percentage growth is in the 4000 + square feet bucket. The smaller starter homes probably won’t get built until the first time homebuyer feels confident enough about the future to buy. Household formation remains depressed, which is keeping housing starts depressed, which is keeping the economy stuck on a 2% growth trajectory instead of a 3% growth trajectory. The turnaround will happen – I thought it would be this year, but it is looking like a 2015 event. I’m starting to feel like Linus in the pumpkin patch preaching about pent-up demand, while waiting for a 1.5 million housing starts print.

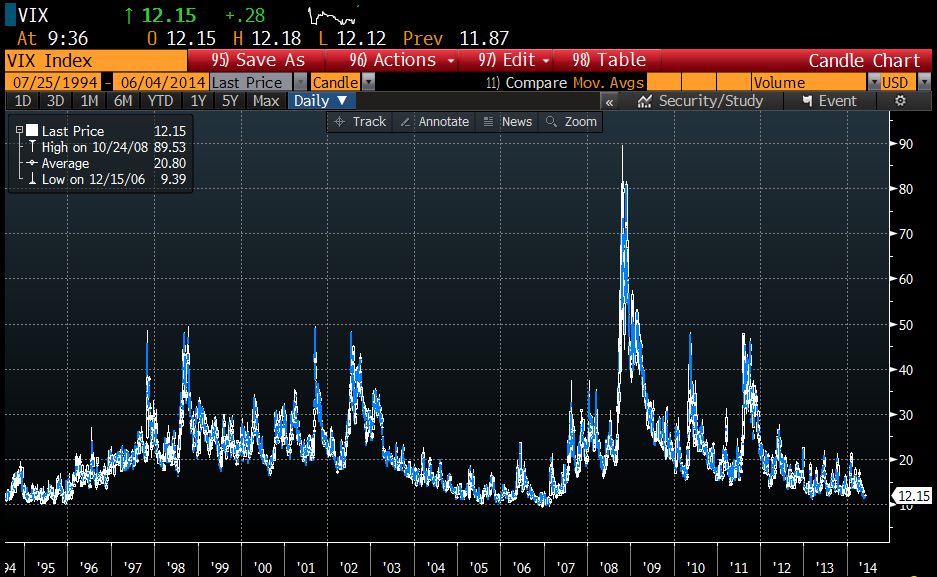

The calm before the storm? The Fed is worried about complacency in the markets. The VIX index has gone 74 straight weeks below its long-run average, which is a similar environment to 2006 – 2007. Junk spreads are widening, and junk issuance is growing as investors reach for yield. William Dudley commented: “Volatility in the markets is unusually low… I am a little bit nervous that people are taking too much comfort in this low-volatility period. As a consequence, they’ll take more risk that really what’s appropriate.” For what its worth, I think the VIX is useful for describing what has already happened in the market, not as a predictor of what is going to happen. Yes, there is the old market saw of “VIX is high, time to buy, VIX is low, time to go,” but a low VIX doesn’t necessarily mean markets are going to fall out of bed – look at the low VIX levels in 94-95, which preceded the mother of all stock market rallies. VIX invariably spikes AFTER the fit hits the shan, not before. It represents market players paying up for option protection, and that is a trailing indicator, not a leading one.

With respect to the junk issuance, investors (in particular defined benefit pension funds and insurance companies) are reaching for yield because the rate of inflation for their liabilities is largely insensitive to interest rates. The actuarial tables couldn’t care less if the Fed is driving down rates via QE – they need to earn X% on their fund to cover expected costs and that’s that. If they can’t get that in Treasuries, they’ll move to assets that can. Invariably that means they have to move out on the risk curve. We have seen this movie before, in the 1950s. FWIW, Dr. Cowbell thinks low rates are here to stay, and that “this time is different.” Most dangerous words in investing, ever. Anyway, it is nice to see the Fed muse about excessive risk taking, although IMO the biggest risk is probably in the so-called “risk free” long bond.

Filed under: Morning Report | 13 Comments »