Posted on August 29, 2014 by Brent Nyitray

Markets are flat this morning on no real news. Bonds and MBS are flat as well.

I don’t think bonds are closing early today, but for all intents and purposes they are as most of the Street will be gone by noon ahead of the 3 day weekend.

The ISM Milwaukee index fell to 59.6, however the Chicago Purchasing Managers Index rose to 64 and the University of Michigan Consumer Sentiment Survey rose to 82.5.

Ready to pop the champagne over the good consumer sentiment numbers? Well, it has yet to flow through to actual spending. Personal Spending fell .1% in July, however the reason was falling energy prices. Ex-food and energy, spending increased .1%. That said it isn’t that strong of a number. Personal Income rose .2%.

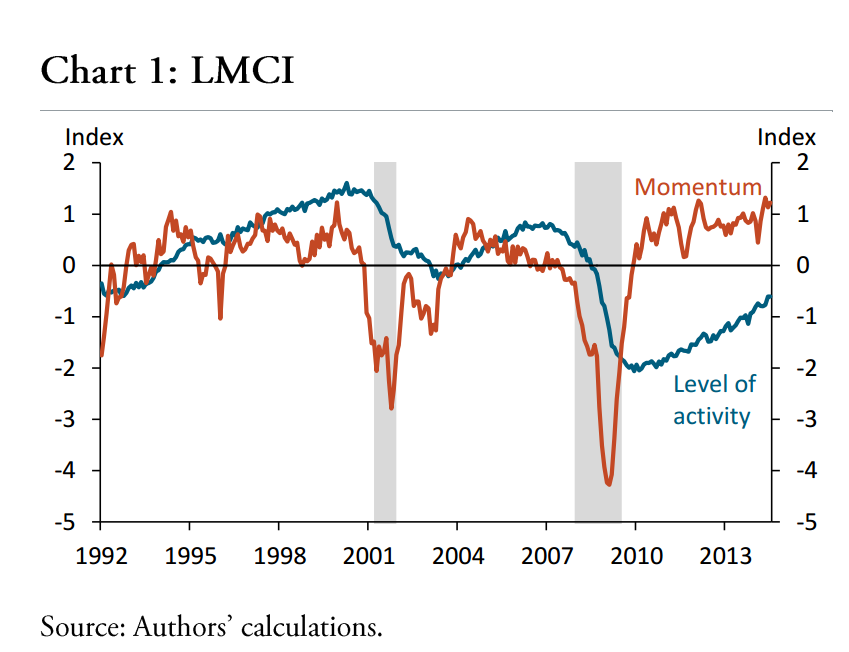

One of the interesting features of this recovery has been the disconnect between the reported unemployment rate and the actual health of the labor market. While unemployment keeps falling, the labor market still doesn’t feel much better. The Fed is now looking at an index comprised of 24 indicators called the Labor Market Conditions Index (LMCI) to describe the health of the labor market. There are two pieces to the index – the current level of activity and momentum. The momentum indicator gives you clues as to where the market is going in the future. Here is what it looks like at the moment – about a year away from normalcy.

Short missive as there is not much going on. Have a happy Labor Day everyone.

Filed under: Morning Report | 23 Comments »

Posted on August 28, 2014 by Brent Nyitray

Some strong economic data this morning, with the second revision to 2Q GDP coming in at 4.2%. Consumption rose to 2.5% and the PCE price index (the Fed’s preferred inflation indicator) came in at 2.1%, with the core at the Fed’s target rate of 2%.

Initial jobless Claims came in at 298,000, another strong number. The Bloomberg Consumer Comfort Index rose to a 5 week high.

Pending Home Sales rose 3.3% in July, but are down 2.7% year-over-year.

The Ellie Mae Origination Insight Report is out. Refis dropped to 32% of all loans in July. FHA accounted for 20%, Conventional 64%, VA 11% and other 5%. The average FICO dropped to 727.

New rules on PMI could raise rates on average 15 basis points.

The elderly are finding the amount they owe on their mortgages increasing. Not sure how much of this is due to reverse mortgages. The mortgage-burning party seems to be a thing of the past.

Consumers have confidence, but not the cash to do anything about it. This is why the consumer confidence numbers look good, but spending numbers are not. Asset prices can only do so much – the chief driver of spending is wages, not asset prices. In fact, home equity extraction during the bubble years masked the overall weakness in wage growth.

Filed under: Uncategorized | 9 Comments »

Posted on August 27, 2014 by Brent Nyitray

Stocks are higher this morning as the S&P 500 crossed the 2000 level yesterday. Bonds are following the rally in Europe. The German 10 year hit 90 basis points this morning.

Slow news day. Going to be a short missive because there isn’t much to talk about.

Mortgage Applications rose 2.8% last week. Purchases rose 2.6% while refis rose 2.8%. Refis were 55.7% of all mortgages originated.

As European economies continue to struggle, the speculation is that European Central Bank Head Mario Draghi will announce some sort of quantitative easing early in September. Blackrock was just appointed as the ECB consultant for the ABS purchase program, it looks like the ECB is serious about going down this route.

The 2008 meltdown was worse than the Great Depression, according to Ben Bernanke. “Of the 13 most important financial institutions in the United States, 12 were at risk of failure within the period of a week or two.”

Filed under: Morning Report | 10 Comments »

Posted on August 26, 2014 by Brent Nyitray

Rallies in European stocks and bonds are dragging US stocks and bonds along for the ride. Remember the PIIGS? The US 10 year yields just a touch less than Italian sovereign debt and about 20 basis points more than Spanish sovereign debt. Let that sink in.

Durable goods orders were all over the map due to a big jump in aircraft orders. The headline number increased 22.6%, however the number most pros focus on – Capital Goods Orders Non-defense / ex-aircraft was down .5%, however June was revised up big, from 1.4% to 5.4%.

The Richmond Fed Manufacturing Index rose to 12 from 7. Consumer Confidence rose to 92.4 in August, from 90.3 the prior month. This is a post-recession high and we are approaching historical normalcy. Lets see if this translates into good personal spending numbers on Friday.

It is official: Burger King is buying Tim Horton’s and plans to move its headquarters up north. Expect the usual kvetching about “corporate patriotism” out of the usual suspects. That said, Walgreens was jawboned into not moving their headquarters, but the stock was slammed on the decision. I am curious as to whether the left will go after the company by threatening a boycott or will go after Burger King Worldwide’s biggest shareholders – 3G and Pershing Square. That said, 3G is a Brazilian investment firm, and who knows if Ackman holds BKW in its onshore or offshore accounts. BKW could already be more or less foreign owned to begin with.

House prices are down month-over-month and year-over-year according to Case-Shiller. These are the seasonally-adjusted numbers – the non-seasonally adjusted numbers were still up .9% month over month.

Separately, home prices continue to rise, according to FHFA, with the index up .4% from May. Prices are up 5.1% year-over-year. The FHFA index is different than Case-Shiller in that it only looks at homes with a conforming mortgage, which means it excludes distressed and high end home. It is more of a central tendency index and tends to be less volatile than Case-Shiller.

Filed under: Morning Report | 105 Comments »

Posted on August 25, 2014 by Brent Nyitray

Markets are higher this morning on no real news. Bonds and MBS are up small.

Lots of economic data this week: Tomorrow we get durable goods, the FHFA Home Price Index and Case-Shiller. Thursday, we get the second revision to second quarter GDP, and Friday we get Personal Income and Personal Spending.

On GDP, note that the Street is forecasting the advance estimate of +4.0% gets revised downward to +2.4%. If that ends up being the case, we will have had almost no GDP growth for the first half of 2014.

Why have the strategists gotten it so wrong with their bond market predictions? (Mea Culpa – include me in that camp). One explanation is that they are looking only at the US and ignoring the weakness emanating out of Europe. The second explanation is that inflation just cannot be found – the rally in the dollar has depressed commodity prices and there is little to no upward pressure on wages. This also might help explain why the Fed is considering hitting some bids with its paper once QE ends.

Another corporate inversion story: Burger King is apparently in talks to buy Canadian-based Tim Horton’s. Note Walgreen’s decided to scrap their plans for moving their headquarters and the stock got demolished.

The takeaway from Jackson Hole? Labor markets need to heal more before the economy can weather higher interest rates. Wage growth is flat right now. In order to get to the Fed’s 2% target on inflation, we would need to see wage growth of around 4%, because productivity-driven increases are non-inflationary. This just goes to show how far we have to go. That said, the economic staff at the Fed has taken down its estimate of the potential non-inflationary GDP growth, so there might not be as much slack as people think.

Filed under: Morning Report | 12 Comments »

Posted on August 22, 2014 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are flat.

Dull Summer Friday with no economic news. Janet Yellen is scheduled to hold a press conference at 2:30 EST, so there is the possibility of something coming out that could move bonds.

The Washington Post has a breakdown on the Bank of America / DOJ settlement. Although the headline amount is $17 billion, it looks like they will actually pay closer to $12 billion. Of the homeowner relief, they may run out the clock on principal modifications and drag them out, as JP Morgan is doing.

Nonvoting St Louis Fed President James Bullard argues there is less slack in the labor market than the Fed’s statements imply. He argues that it is the unemployment rate and payroll growth that matters, and that the labor force participation rate doesn’t add much information and is outside the purview of monetary policy. He is probably correct in that regard – I don’t really see how 25 basis points one way or another on the Fed Funds rate is going to affect the long-term unemployed. That said, I don’t think they move meaningfully until we start seeing wage inflation. That doesn’t rule out a symbolic increase in the Fed Funds rate sometime next year. Separately, Charles Plosser thinks we should raise rates this year.

Filed under: Morning Report | 7 Comments »

Posted on August 21, 2014 by Brent Nyitray

Markets are higher after another sub 300k initial jobless claims number. Bonds and MBS are flat.

Existing home sales rose to a 5.15 million annual pace, according to NAR. Median Home Prices are up 4.9% to $222,900. Distressed sales made up 9% of all sales, the lowest percent since 2008. First time buyers inched up to 29%, and all-cash buyers ticked down to 29%. Days on Market increased to 48.

In other economic data, the Index of Leading Economic Indicators ticked up to .9% from an upward-revised .6% in June. The Philly Fed Manufacturing Index was strong at 28.

There was nothing earth-shattering in the FOMC minutes. One thing did jump out at me, and it was the fact that they lowered their estimate for the potential GDP growth rate. They revised their GDP forecast downward and also said that unemployment was closer to its natural rate. This effectively lowered the “speed limit” of the U.S. economy, and in a way, waves the white flag over the plight of the long-term unemployed. Of course there is probably not much monetary policy can do for the long-term unemployed in the first place, but that is a separate issue. I guess the Fed is seeing wage growth somewhere (not sure where, aside from skilled labor), and they think we are closer to seeing inflation flare up for the whole economy. The punch line is that, at the margin, rates may be going up sooner than anticipated.

Speaking of inflation, thanks to the recent rally in the US dollar, commodity prices are getting slammed. Oil is down 13% in the last two months, natural gas is down 20%, corn is down 17%, and bonds are rallying. Not seeing where the inflation is going to come from. Fun fact: Spanish 10 year bond yields are now lower than the US 10 year. Remember the PIIGS of the European Sovereign Debt Crisis? Their bond yields are generally in line with ours: Portugal is 3.26%, Italy is 2.59%, Ireland is 1.88%, Greece is 5.78% and Spain is 2.39%. Kind of amazing when you think about it. The point is that you can’t look at US rates in a vacuum – worldwide sovereign yields are rallying, and it is pulling US yields lower as well.

Bank of America settles with the DOJ for $17 billion. BOA’s purchase of Countrywide will probably go down in history as one of the most ill-advised mergers ever, along with Time Warner’s purchase of AOL, and Warren Buffet’s purchase Johns Manville’s asbestos liability stream. Separately, while the government dropped its criminal case against Angelo Mozillo, they are still going after him in a civil case.

Filed under: Morning Report | 26 Comments »

Posted on August 20, 2014 by Brent Nyitray

Stocks are lower this morning on no real news. Bonds and MBS are flat.

Mortgage Applications rose 1.4% last week. Purchases fell .4%, while refis rose 2.7%. The 30 year fixed rate mortgage finally fell six basis points after stubbornly resisting the moves in the bond market.

Later on today, we will get the FOMC minutes. While there were no changes to the economic forecasts, the markets will be looking to see if the circle of hawks is growing.

Job growth is mainly at the low end of the pay scale. But the wage growth is mainly at the high end. The US labor market is incredibly bifurcated at the moment. This is certainly what keeps Janet Yellen up at night, although the bigger question is whether the Fed can really do anything about it.

BlackRock chief investment strategist Russ Koesterich is saying that bonds have it right, stocks have it wrong with respect to the view of the economy. The higher debt levels will act as a drag on growth for the next decade or two. In other words, we are Japan, and Reinhart / Rogoff are right. This is of course heresy to Dr. Cowbell, who believes the solution to the economic morass is to borrow more (since rates are so low) and to spend it on infrastructure. Japan did exactly what Krugman wanted, and took their debt to GDP ratio to 2.2x and has had little to no economic growth for a generation. As a point of reference, our debt to GDP ratio just over 106%, however the Fed owns about a quarter of that (through QE) so it is really debt we owe ourselves.

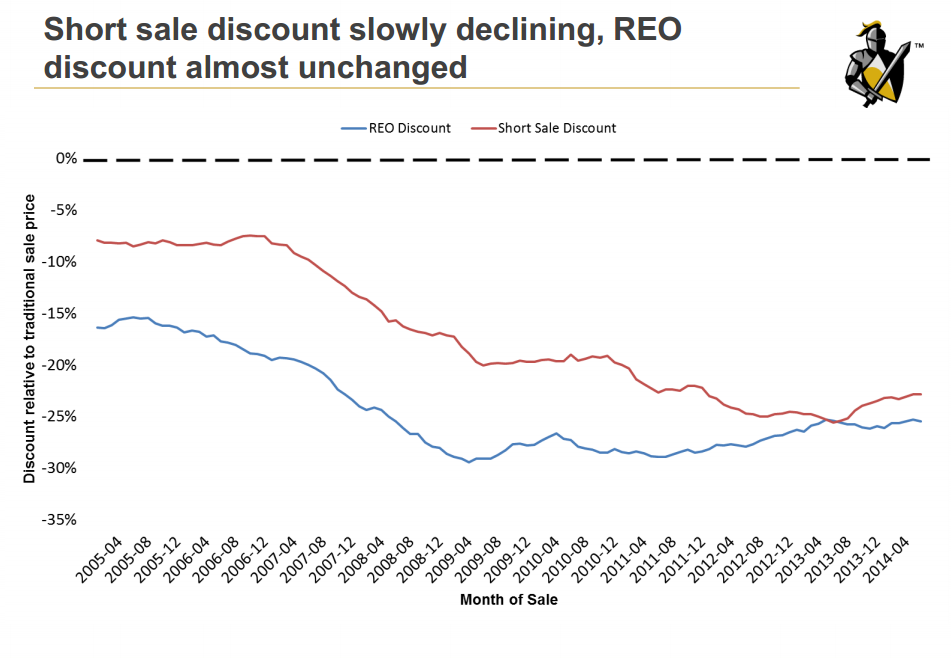

Foreclosure starts and Delinquencies ticked up in June, according to Black Knight Financial Services (formerly known as Lender Processing Services or LPS). DQs increased to 5.7% from 5.62% in May, while foreclosure starts ticked up to 88.3k vs 86.3k a month before. On a year over year basis, foreclosures starts are down 19%. Inventory continues to be concentrated in the judicial states of NY, NJ, and FL. Short sale discounts continue to narrow, while the REO discount is flat.

Filed under: Morning Report | 13 Comments »

Posted on August 19, 2014 by Brent Nyitray

Markets are higher this morning after housing starts hit the highest level in eight months and inflation at the consumer level remains muted. Bonds and MBS are up.

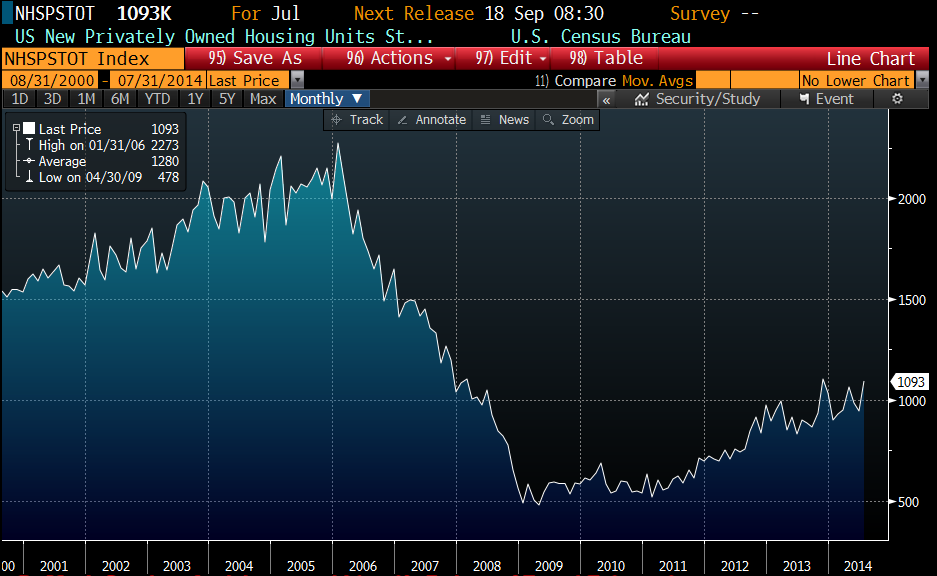

Housing starts in July were at a seasonally-adjusted annual rate of 1.09 million, which is 15.7% above June and almost 22% above last year. Building Permits were 1.05 million, up 8.1% month-over-month and up 7.7% year-over-year. Multi-fam drove the increase, although single fam did increase as well. Multi-fam starts are notoriously volatile. We saw big increases in the Northeast, while the Midwest was flat. The South and West were up slightly. Can’t complain about the number, which was the highest in eight months. Still, “normalcy” is around 1.5 million units per year, which goes to show how depressed housing still is. We probably will not hit historical numbers until the first time homebuyer returns.

The Consumer Price Index rose .1% in July, which is up 2% year over year. Ex food and energy, it rose 1.9% year over year. This cheered the bond market.

The Despot reported earnings that beat estimates, with comp store sales up 5.8%. People are starting to spend money on home improvement. The stock is up about 4 bucks this morning.

What will the world’s finance chiefs be talking about this week at Jackson Hole? First, don’t look for any market-moving statements, but there is always the possibility. Second, the labor market and the issue of the economy’s speed limit. Is it possible to have unemployment continue to fall without increasing the labor force participation rate? Are the long-term unemployed now permanently unemployed? If so, the amount of improvement we can expect to see without causing inflation is limited. FWIW, the most dangerous words in economics and financial markets are “this time is different.” I am more sanguine than most.

Is the lock-in effect going to matter as rates rise? In other words, as rates rise, home buyers will experience an increase in their mortgage rates, which could prevent people from moving. If so, will this be a drag on mortgage production? Zillow convened a panel of experts who believe this effect will probably be muted. Unless we suddenly get a bout of hyperinflation, rates are probably moving up to 5% or so over the next few years. This is probably a gradual enough increase that it won’t affect things too much.

Filed under: Morning Report | 10 Comments »

Posted on August 18, 2014 by Brent Nyitray

Markets are higher as European stocks rally. Bonds and MBS are down on decreasing pressure in Ukraine.

The National Association of Homebuilders Sentiment Index rose to 55, the highest level in seven months.

This week will have some important data, with housing starts and building permits tomorrow, and the FOMC minutes on Wednesday. The minutes will be especially interesting as “lift off” (the Fed’s euphemism for increasing rates) approaches. Finally, central bankers, finance ministers, and other officials will meet at Jackson Hole on Thursday. There will be the possibility of market moving quotes so be aware.

The labor market is improving, at least at the higher end. Skilled labor is tough to find, and we are finally seeing some job growth in professional services. Low skilled labor and the long term unemployed are still struggling. Separately, part time workers who want to work full time are presenting a problem for the Fed. Which means don’t focus on the unemployment rate, focus on wage growth when thinking about the Fed’s posture towards interest rates.

What has QM succeeded at doing? Raising compliance costs. Has it changed business practices? Nope.

Filed under: Morning Report | 22 Comments »