Markets are lower this morning on no real news. Bonds and MBS are flat.

The ECB decision is tomorrow. The market has priced in a lot of optimism for QE, so if they disappoint, rates could reverse hard. Keep in mind that US rates have been pulled down by Europe. The fundamentals of the US economy mean rates should be higher.

A headline just crossed the tape saying the ECB is set to propose QE of 50 billion euros a month through 2016. Assuming they start next month, that works out to be $1.1 trillion – I believe the expectations were for the mid $500s billion. Bonds are not reacting to the news. Again, this is just a leak or speculation, not the actual decision.

Housing Starts rose to 1.09 million in December, an increase from the upward-revised 1.04 million in November. Building Permits fell however.

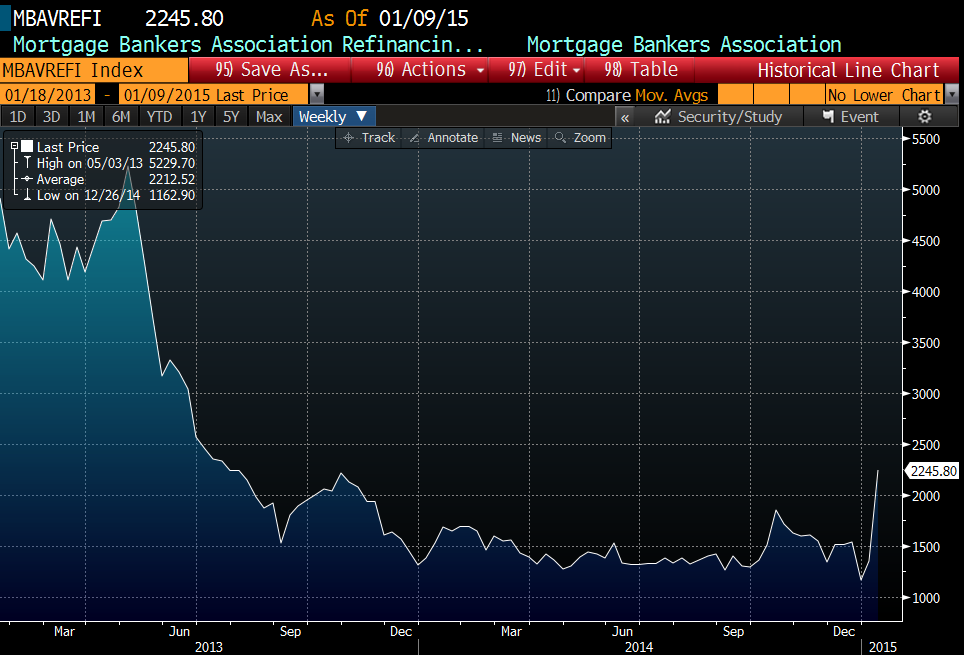

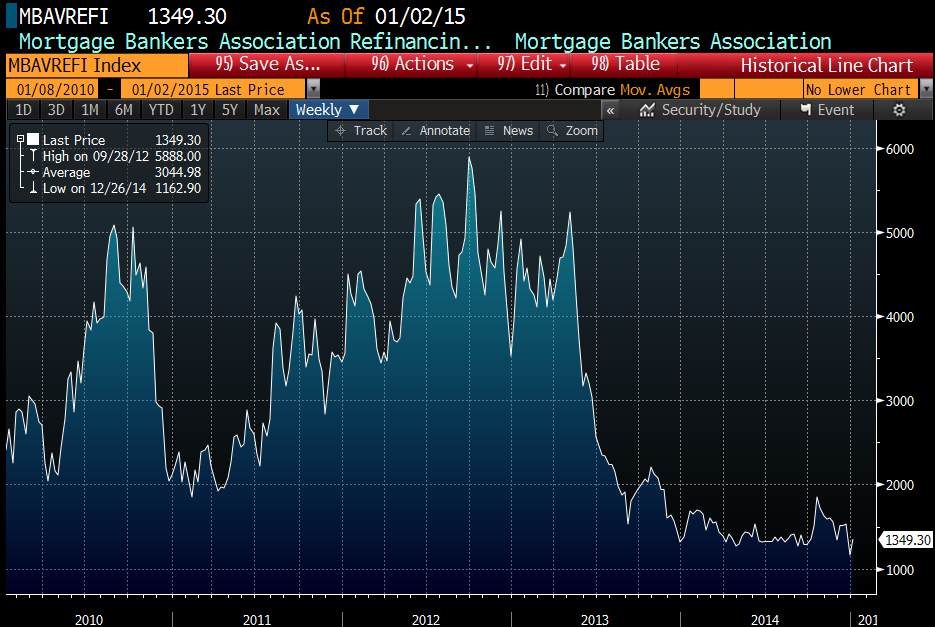

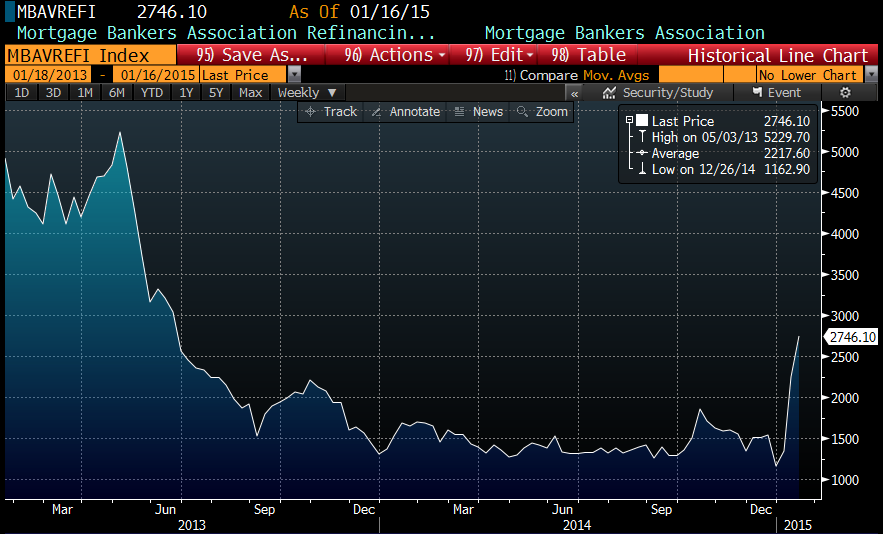

Mortgage Applications rose 14.2% last week following up on an increase of 49% the week before. Purchases fell 2.2% while refis rose 22.3%. Refis are now 74% of all applications, a 10% increase from the beginning of the year. The MBA refi index is the highest it has been June of 2013, when the taper tantrum was beginning.

Obama gave the State of the Union speech last night. If you are interested, here is the take on it. I don’t think he had anything to say affecting housing although he wants to increase the capital gains tax and he vowed not to roll back banking regulations.

The Supreme Court is hearing arguments today challenging the Administration’s novel theory called “disparate impact” to prove discrimination. Basically, the Administration wants to be able to declare a lender guilty of lending discrimination if the numbers don’t comport with the demographic make-up of their market, even if the lender did not intend to discriminate. The Court is expected to rule in June.

The rise in the dollar has been giving foreign real estate investors sticker shock. Foreign investment demand is behind a lot of the buying in big cities like NY, DC, SF, etc. The woes in Russia are having a big impact as well.

Filed under: Morning Report | 12 Comments »