Markets are higher this morning as oil rebounds. Bonds and MBS are down.

Initial Jobless Claims came in at 316k, higher than expected, while the producer price index fell .3% in December. The Empire Manufacturing Survey rebounded back into positive territory.

I wanted to talk a little about TBAs this morning given some questions I have had from LOs. (Those of you not in the origination business can skip it). Someone had priced a VA loan last week and found that pricing was worse a week later (not by a little, but by a point), even though the bond market rallied. How was that possible given that the 10 year fell 17 basis points in yield? I will explain. It is a function of the new FHA mortgage insurance premiums.

Some background: The TBA (stands for To Be Announced) is the basic input to a rate sheet. If I was to sell a pool of FHA or VA loans today, the price I would get would be the TBA price plus some carry (interest for a few days). So, when we put out our rate sheets, we start with the TBA prices and then add on our costs to originate, margins, etc.

Look what happened last week. When the government announced lower mortgage insurance premiums for FHA loans, the Ginnie Mae TBAs underperformed versus the Fannie Mae TBAs, which set pricing for conforming loans. The reason for this was the market re-assessed prepayment speeds. By lowing the MI going forward, it made refinancing more attractive. This means that prepayment speeds are increasing and that makes the existing TBAs worth less. Think about it: If you bought a Ginnie 4% TBA for 106, and it prepays in a year, what to you get? Par, or a loss of 6%. The higher up the coupon, the bigger the incentive to prepay is.

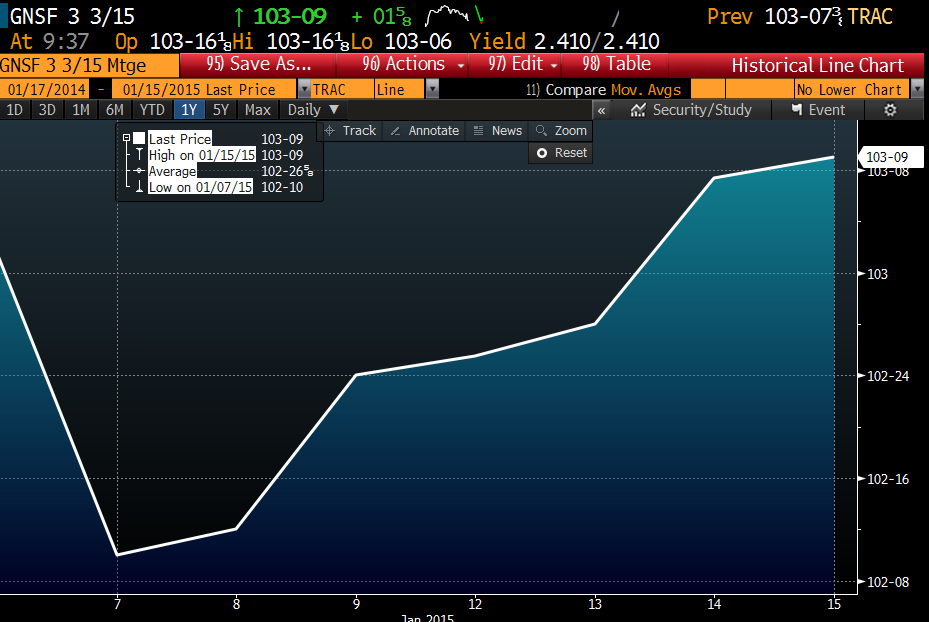

Here are a couple charts of Ginnie Mae TBAs from last week. The first is the March Ginnie Mae 3% TBA. It rose about 9 ticks, following an initial sell-off on the MI news. This underperformed the Fannie Mae 3% TBA by about 9 ticks. Remember, as bond prices rise, yields fall. The falling yield meant that if you quoted a customer a 3.5% FHA or VA loan last week, and locked it this week, the customer would probably have some points coming to them. This was to be expected, since rates fell:

Now, let’s look at what happened to the Ginnie Mae 4% TBAs. This would include loans with rates between 4.25% and 4.625%. The 4% TBA actually fell. By a lot. This means if you quoted a borrower a 4.5% VA loan last week and tried to lock it today, the borrower would have to pay more points. Why? Prepayment speeds. The 4% Ginnie security is much more likely to prepay than a 3% security. Therefore, investors have to price in the new information, and that meant the 4% security was worth less, and that means borrowers are going to be treated as if rates rose, even though they didn’t in the bond market.

Note that the government may have inadvertently increased the risk to the taxpayer on the FHFA insurance fund and gotten nothing out of it. If they cut the MI, but rates increase, they have accomplished nothing except for further subsidizing MI and increasing the risk of a future taxpayer-funded bailout. The law of unintended consequences rears its ugly head once again…

This is real “inside baseball” stuff, but if you wondered about the mechanics of loan pricing and interest rates, hopefully this helped. And if you have a borrower who is asking why there hasn’t been this massive move in FHA and VA pricing since rates fell so much last week, you can explain why.

Filed under: Morning Report |

Pope: Your 1st Amendment Riggs end at my ears.

http://hosted.ap.org/dynamic/stories/A/AS_REL_FRANCE_ATTACKS_POPE?SITE=AP&SECTION=HOME&TEMPLATE=DEFAULT

LikeLike

Connecticut rejects the right of 17 yr old girls to control their own bodies. (Not to worry, though. Teen abortion on demand is still legal.)

http://www.foxnews.com/health/2015/01/08/connecticut-supreme-court-upholds-ruling-that-teen-must-undergo-chemo/

LikeLike

Making your big play Brent?

“Investors Put More Than $100 Million Into the Marijuana Industry Over the Past Two Years

By Will Yakowicz ”

http://www.slate.com/blogs/moneybox/2015/01/15/peter_thiel_and_marijuana_tech_giants_across_the_country_have_spent_over.html

LikeLike

Everything in government is corrupt.

http://www.washingtonpost.com/blogs/federal-eye/wp/2015/01/14/panel-clears-u-s-prosecutors-accused-of-botching-sen-ted-stevenss-corruption-trial/

Defend increasing it’s power.

LikeLike