Markets are flat this morning on no real news. Bonds and MBS are up.

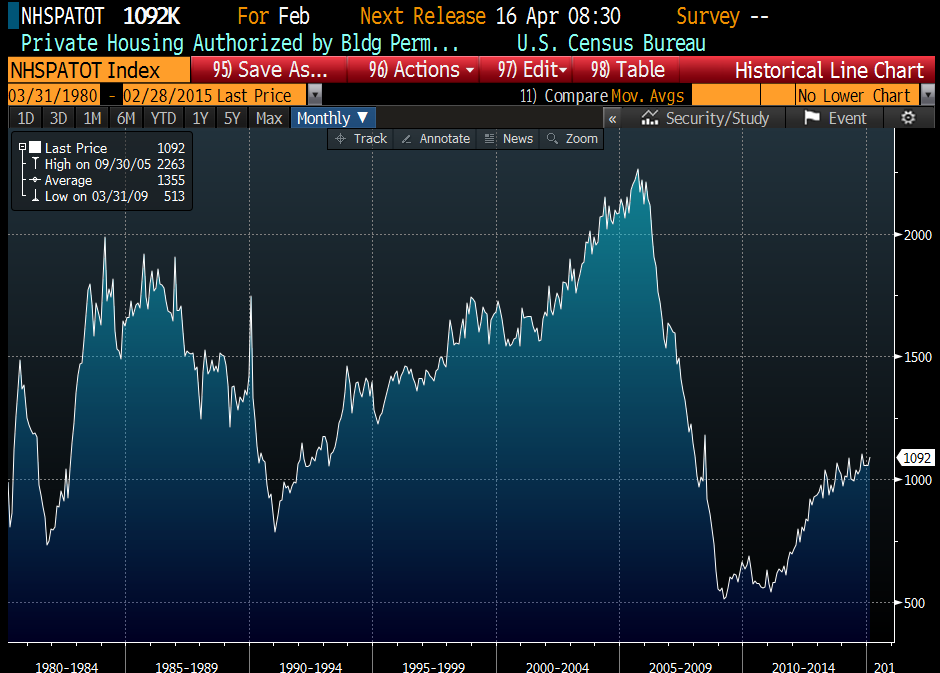

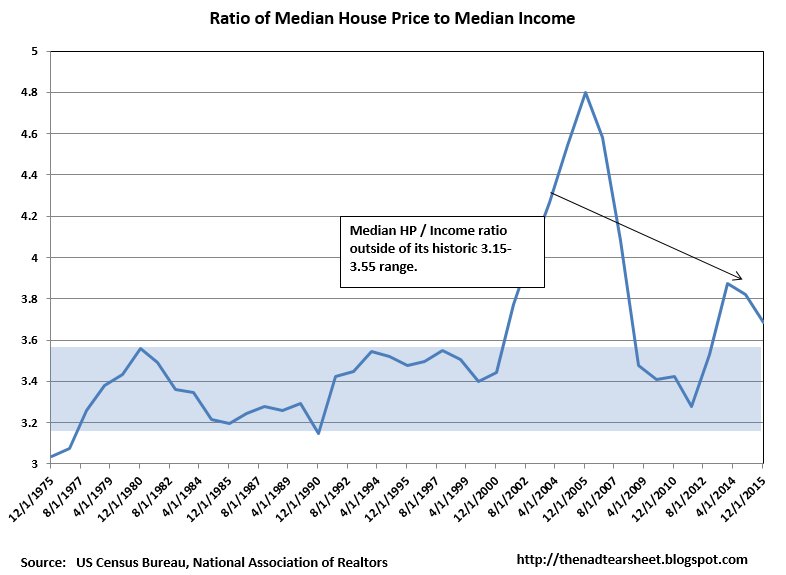

Existing Home Sales rose to an annualized pace of 4.88 million in February, up slightly from 4.82 million in January. Note this is probably a weather-driven number and February is still in the seasonally slow period. The median home price was $202,700 which is up 7.5% year-over-year. Median income is about $55,000 or so, which means the median house price to median income ratio is sitting at 3.68x, which is on the high side. Historically, that ratio has sat in a range of 3.15x – 3.55x. It means that house prices are probably not going to flatten until we start seeing wage inflation.

The Chicago Fed National Activity Index slipped in February as production-related indicators fell. Employment related indicators slipped however were still positive. Poor weather undoubtedly played a role.

The housing reform bill is making its way into the House. This bill, called The Partnership to Strengthen Homeownership Act envisions winding down Fan and Fred, and increasing the role of Ginnie Mae. Private mortgage insurance will bear the first 5% of severity with the government bearing losses beyond that. It sounds like this bill is gaining support of Congressional Republicans as well, however understand this bill is the left’s wish list. The left wants to continue social engineering via the housing market while the right wants to decrease the government’s footprint. The social engineering (aka “affordable housing”) stuff will probably be the biggest sticking point. The plan envisions Ginnie Mae’s 10 basis point guarantee fee will be used for affordable housing goals. Note the government plans to wipe out Fannie and Freddie stockholders, although those two stocks are litigation lottery tickets at this point.

The low price points in urban areas are beginning to decline again. In many urban areas, the suburbs have recovered, while the inner cities remain weak. I wonder how much property in the inner cities was bought by professional investors who are starting to eye the exit. Rental prices continue to rise, but at some point pros will want to monetize these investments. Of course this also demonstrates one of the issues with the CRA: it demands that bankers ignore location when considering the riskiness of the underlying collateral when pricing credit, when location clearly matters.

Filed under: Morning Report | 34 Comments »