Posted on April 24, 2015 by Brent Nyitray

Markets are higher this morning on good earnings out of US companies. Bonds and MBS are up small.

Durable Goods rose 4% in March, however if you strip away transportation, they fell .2%. February was revised downward. Capital Goods orders (a proxy for business capital expenditures) fell .5% and February was revised down to -2.2%. We have seen a slew of disappointing data this quarter – Merrill Lynch is now forecasting Q1 GDP growth of 1.5%.

Comcast has officially pulled the plug on its merger with Time Warner Cable. Washington hated this deal from Day 1, and it became apparent this week that neither the FCC nor the DOJ was going to wave this through.

Yesterday was a monumental day (of sorts) for stocks. The Nasdaq finally eclipsed its high from March 2000. Back then the mentality was to buy quality stocks, don’t worry about the price, just hold out for the long term. For a trip down memory lane, remember the “four horsemen” of tech – the supposedly bulletproof stocks according to Jim Cramer were INTC, DELL, MSFT, and CSCO. Where are they now? Intel is down 57% from the peak, Dell was taken private in 2013 at $13.75, a 77% discount to its 2000 peak, If you were in Mr. Softee, you would be up 10% over 15 years, and almost all of your return would have beeen via the 2.7% dividend. Finally, you would have been much better off in the “other Cisco” – food service company Sysco (SYY) – than you would have been in CSCO, which is down 60% from its peak. No, Virginia, you cannot simply “buy good companies whatever the price, and expect to make money over the long term.”

That era’s madness was perfectly encapsulated in the stock split beeper – a pager that would go off when a company announced a stock split. Cause nothing creates value like a stock split.

In many ways, the four horsemen of tech were similar to the Nifty Fifty of the 1970s – one decision stocks like Avon and Polaroid. They worked until they didn’t. In the physical sciences, knowledge is cumulative. In the financial markets, it is cyclical.

In other words, don’t worry about a bubble in the NASDAQ. People realize that stocks are just an asset that can go up or down – there is nothing special about them. Without that mentality of investors, you aren’t going to have a bubble. Bonds on the other hand…

The NAHB is forecasting 2015 will be “slow and steady” for housing and 2016 will be the breakout year. The pent up demand of the first time homebuyer will be the catalyst, but we have been waiting for a long time for that.

Filed under: Morning Report | 10 Comments »

Posted on April 23, 2015 by Brent Nyitray

Stocks are lower on overseas economic weakness. Bonds and MBS are flattish.

Initial Jobless Claims came in at 295, a little higher than expected. The Bloomberg Consumer Comfort index slipped to 45.4 from 46.6.

New Home Sales dropped to an annualized pace of 481k in March, from 543k in February. This was a big miss – the Street was at 515k.

We heard from homebuilder D.R. Horton yesterday. They beat expectations, but the margin and revenue guidance was on the light side, so the stock was sold off. D.R. Horton is very exposed to Texas and has yet to see any evidence of an slowdown in that economy. Horton was encouraged by the demand and is seeing strong growth in its Express brand, which is targeted at the first time homebuyer. The downside is that the margins in Express are lower.

Pulte reported this morning, and missed expectations. Revenues were light, however orders were up 6% and ASPs were up 2% to 323k. The company noted at strong start to the spring selling season, and characterized the housing recovery as “sustained but slow.”

Interesting stuff on the state of part-time workers. US part-time employment is reaching historical norms and that indicates the slack in the labor market is going away. Interestingly they polled workers who put in 30 hours a week or less. Of those people, a third were happy with their hours or wanted to work less. Only 23% wanted a traditional 40 hour a week job. Of those working more than 30 hours, about a quarter wanted to work less. Punch line: as the slack is taken up, wages are going to have to go up. Which means the Fed is more likely to mover sooner rather than later.

The Clinton Foundation is under the microscope right now, and the New York Times has a piece about how the State Department approved a Russian nuclear deal after a big donation to the Clinton Foundation. WaPo has a piece on the foundation and Bill Clinton’s speaking fees. There is supposedly a tell-all book coming out on the Clinton Foundation as well. Whatever comes out of it, the Democratic Party is all-in on Hillary and will dismiss any revelations as partisan poo-flinging regardless of the merits.

Filed under: Morning Report | 1 Comment »

Posted on April 22, 2015 by Brent Nyitray

Stocks are up this morning as struggling Greek banks get a bit more breathing room. Bonds and MBS are down.

Mortgage Applications rose 2.3% last week, according to the MBA. Purchases were up 5% while refis were up .6% and accounted for 56% of all loans.

Existing Home Sales rebounded to 5.19 million in March, according to the National Association of Realtors. Inventory remains tight at roughly 4.6 months (6 months is considered “balanced”). The median home price was 212,100, which is 7.6% higher than a year ago. The first time homebuyer was 30% of all sales, which is starting to inch up. More inventory and more construction is needed to see these numbers improve. Cash sales as a percent dropped to 24% as professional investors exit and “real” buyers return.

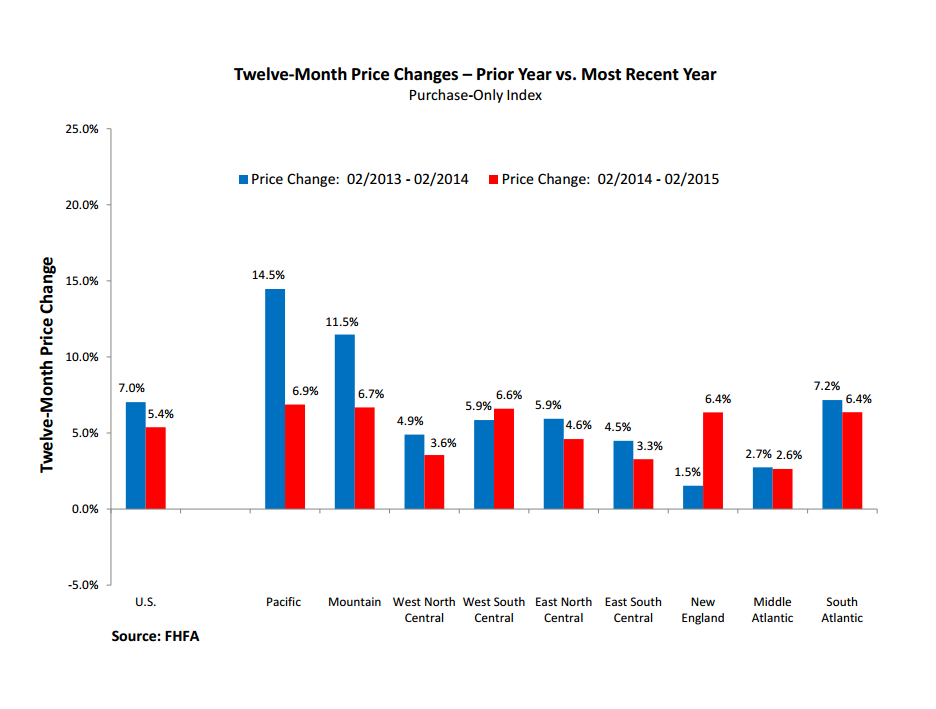

The FHFA Home Price increased .7% in February, well above the .5% expectation. On a year-over-year basis, prices were up 5.4% and we are now within 3% of peak levels, which puts it roughly at January 2006 levels. If you take a look at the geographic returns, the West Coast is slowing down from its torrid pace in 2014, however it is still strong. The bright spot seems to be the turnaround in the Northeast, where home price appreciation is finally higher than the national average. For a long time, Southern California and New England have been polar opposites, with a red-hot market out west and an ice cold market in New England. The big Northeast judicial states appear to be finally cleaning out the inventory of foreclosed homes, which has been weighing on the market.

If you were wondering how Treasury views Fannie mae stock, look no further. Senator Chuck Grassley (R., Iowa) sent a letter to Treasury asking how the government was going to treat Fannie Mae shareholders now that taxpayers have recouped their bailout funds. Treasury’s response – that was not a “loan” that can be paid back – it was an “investment” that should earn a huge return given the risk that taxpayers took. In other words, this will come down to litigation between Fannie Mae shareholders and the government and Fannie Mae stock is a litigation lottery ticket.

The German Bund is the “short of a lifetime” according to Bill Gross. Separately, Paul Singer of Elliott Management characterized the sovereign debt bubble as on par with the subprime bubble. The Fed inflated the stock market bubble which subsequently burst, then inflated a residential real estate bubble to ease the pain of the burst stock market bubble, and then inflated a sovereign debt bubble to ease the pain of the burst residential real estate bubble. As I have said before, stock prices are pricing in a 100% probability that the Fed can raise rates with no one blowing up. Not sure that is a good bet. It also raises on more thing to think about – Hillary’s most formidable opponent will not be the GOP candidate – it will be Janet Yellen.

Filed under: Morning Report | 11 Comments »

Posted on April 21, 2015 by Brent Nyitray

Stocks are higher this morning as earnings come in better than expected. Bonds and MBS are up.

Housing advocates are urging the government to investigate and intervene in communications between MBS holders and servicers. They claim that MBS investors (read Wall Street Sharpies) are urging servicers to forego modifications and to pursue “unnecessary foreclosures.” Surprisingly, they hold up Ocwen as pillar of servicing virtue. Of course Ocwen is fighting for its life and will do anything it possibly can to make the government happy.

New simpler mortgage disclosure forms are coming August 1, and

they could slow closings as professionals learn to navigate the new system.

M&A activity is picking up, with an interesting situation in the pharma sector. Mylan, who last week launched a hostile bid for Perrigo,

now faces an unsolicited bid from Teva. A combination of low interest rates and high stock prices make growth by acquisition an attractive strategy. Teva’s biggest drug faces generic competition so they need to replace that revenue. Mylan / Teva is going to face antitrust scrutiny. This situation looks like a fun one for the arbs.

While ZIRP is helping to drive M&A activity,

the unintended consequence is that insurers and pension funds are getting hammered as they cannot earn enough on their assets to cover their estimated liabilities. There are two ways out of the box: either assume it away with rosy estimates of asset return and liability inflation, or take a lot more risk. This is part of the reason why the Fed wants to get rates up to a more normal level. I suspect they fear we are going to have to bail out the state pension funds and / or insurance companies.

High end real estate has replaced gold as the go-to asset for storing wealth. Real Estate and contemporary art are the new store of value of choice for foreign investors. Gold, which used to have that role, cannot get out of its own way. Why? Blame the financial crisis, where gold sold off just like every other asset in a situation tailor-made for it. If gold was unable to rally in that sort of crisis, what good is it? Note that high end real estate in places like London, New York, and Vancouver are owned largely by Chinese investors, and China has its own issues, as even state-owned companies

are now defaulting on their debt. As their real estate bubble bursts, it will be interesting to see if they liquidate overseas property. Generally in a crisis, you sell what you can, not necessarily what you want to.

Filed under: Morning Report | 13 Comments »

Posted on April 20, 2015 by Brent Nyitray

Markets are higher this morning on overseas strength. Bonds and MBS are flattish.

This week doesn’t have any data which will move the bond market, but we do have some important numbers nonetheless. On Wednesday, we will get existing home sales and the FHFA House Price Index. On Thursday, we will get New Home Sales. Finally, we will get earnings from Pulte an D.R. Horton. Hopefully their comments will help reconcile the strong builder sentiment with the lousy housing starts numbers.

The Chicago Fed National Activity Index fell to -.42 in March, giving further ammo to the argument that the deceleration that started in January and February was not simply weather driven. The 3 month moving average, which is a more stable, indicates that the economy is operating below its historical trend.

William Dudley is speaking at the Bloomberg Americas Monetary Summit this morning. His main points – the Fed will be data-dependent (boilerplate), and the Fed is cognizant of the risks or liftoff on emerging markets. Even if rates do go up, monetary policy will still be easy. That said, ECB and BOJ easing does make credit conditions more supportive. The stock market is blithely assuming that the economy will handle rate hikes as easily as it handled the end of QE and is therefore vulnerable, IMO.

The Fannie Mae and Freddie Mac guarantee fee review is finished, and it looks like not much is going to change. The 25 basis point adverse delivery fee is gone, but there are new fees imposed, so it looks to be more or less a wash. Borrowers with lower credit are going to pay slightly less, while high bal, investment properties, and cash out refis will become slightly more expensive.

Filed under: Morning Report | 1 Comment »

Posted on April 17, 2015 by Brent Nyitray

Stocks are lower this morning after Chinese shares got roughed up overnight. Bonds and MBS are down small.

Inflation remains well contained and below the Fed’s target. Consumer Prices rose .2% in March. On a year over year basis, they were down .1%. Ex food and energy, they were up 1.8%. Real weekly earnings were up 2.2%. The wage inflation number is encouraging, as wage growth is the last piece of the puzzle.

Consumer Sentiment rose, according to the University of Michigan Consumer Sentiment Survey. Current conditions and expectations both increased.

The Index of Leading Economic Indicators improved slightly in in March, to 0.2% from a downward-revised 0.1% in February.

The NAHB is pushing Congress to pass the Mortgage Choice Act, which makes some modifications to the definitions of points and fees in order for a mortgage to be considered a qualified mortgage. They believe credit is too tight, and the regulatory agencies are part of the reason why. Interesting given the lousy housing starts number this week.

Filed under: Morning Report | 20 Comments »

Posted on April 16, 2015 by Brent Nyitray

Markets are lower this morning on European profit-taking. Bonds and MBS are up small.

Very disappointing housing starts numbers this morning – 926k versus expectations of 1.04M. Building permits fell to 1.04M as well. The weakness was both in single fam and mult-fam. It is hard to reconcile these numbers with the NAHB Homebuilder sentiment survey from yesterday, or the trading in the XHB ETF but here we are. You might be able to blame starts on the weather (and even that is a stretch) but you can’t blame permits on that. Punch line: supply will remain tight, and prices will probably be a touch higher than people are forecasting.

The Philly Fed Index improved to 7.5 versus 5 last month.

The Bloomberg Consumer Comfort Index fell to 46.6 last week The perception of the buying climate is improving the most, while people’s perception of the economy and their personal financial situation is improving more slowly.

Initial Jobless Claims increased to 294k last week. At least the labor market seems to be holding up, although wage growth is still lackluster.

The left continues to agitate for “living wage” legislation and is hoping they have the beginnings of a movement. Set aside the fact that these protests are largely rent-a-mobs of union people, professional protesters, bums, and college students, there is something bigger happening here. This is at its core a war between “shareholder capitalism” and “stakeholder capitalism” as the left moves to seize ideological ground it lost 30 years ago. Expect to hear a lot of “If Company XYZ just suspended its stock buyback program, they could pay everyone a living wage” claims.

We will undoubtedly see a lot of demagoguery about wages from politicians, but there really isn’t much anyone can do about it. The Democrats will agitate for minimum wage hikes and living wage legislation while Republicans will blame regulation and an anti-business environment. The only thing that will change it is economic growth, and as long as we have slack in the labor market, wages aren’t going up. Growth will happen, but we are still in the aftermath of a burst asset bubble, and recoveries from burst bubbles can be maddeningly slow. Of course this gives the Fed an excuse to stand pat, although they are creating bigger and bigger imbalances as ZIRP continues.

The German Bund yield is now a single-digit midget. If you lend money to the German government for 10 years, you will get 9 bps. Guess we are headed to negative rates there as well. How are insurance companies like Allianz and Munich Re at 52 week highs? There is no way they can cover their actuarial liabilities in sovereign debt these days. I know the stock has a fat dividend yield of 4.1%, but I wouldn’t bet on that dividend getting maintained. As I have said before, the actuarial tables don’t care that money is free. Insurers are stuck between having to take a lot of risk for a little return or to simply use unrealistic future growth assumptions to remain solvent.

Filed under: Morning Report | 4 Comments »

Posted on April 15, 2015 by Brent Nyitray

Markets are higher this morning as ECB President Mario Draghi speaks and bank earnings continue to trickle in.

Mortgage Applications fell 2.3% last week. Purchases were down 3.1%, while refis were down 1.8%.

Some weaker economic data this morning: the Empire Manufacturing Index fell steeply in April, to -1.19 vs. 6.9 expected, while industrial production fell .6% and capacity utilization fell to 78.4%. Can’t blame this on the weather – blame the dollar.

Bank of America reported that mortgage originations increased 18% QOQ and 54% on a YOY basis. Between JPM, BAC, and WFC, it looks like the mortgage business is improving quite a bit. Maybe the long-awaited turn in the real estate sector is upon us. We will get more data tomorrow with housing starts and building permits.

Hillary officially launched her campaign over the weekend, unveiling her new logo, which looks like “Hospital Thataway.” Suffice it to say, the H logo appears to be a bomb, and the interwebs are already making fun of it.

Best one so far:

Filed under: Morning Report | 17 Comments »

Posted on April 14, 2015 by Brent Nyitray

Markets are lower this morning as bank earnings pile in. Bonds and MBS are up on the back of a strong bond market rally in Europe.

Retail Sales came in weaker than expected, although some of that is due to falling commodity prices (especially gasoline). The headline number was +0.9% versus +1.1% expected. The control group, which strips out some of the more volatile components increased .3%.

Wells reported that originations increased to $49 billion in Q1 versus $44 billion in Q4. Margins expanded, with gain on sale margins increasing from 1.80% to 2.06%. Given that mortgage banking is so seasonal, it is surprising Wells reports quarter over quarter comparisons. J.P. Morgan reported first quarter originations were up 7% QOQ and up 45% YOY. MSR valuations got hit – their MSR book is valued at 2.53x versus 2.8x at the end of the year and 2.86x last year.

Inflation remains muted at the wholesale level, with the Producer Price Index coming in at .2% month-over-month and falling 0.8% year over year. While the Fed prefers to look at Personal Consumption Expenditure Inflation instead of CPI / PPI, markets still pay attention. This is the other reason why bond yields are so much lower this morning.

We haven’t talked about European bond yields in a while, but they continue to fall, which is keeping a bid under Treasuries. The German Bund (their 10 year bond) yields 13.7 basis points. The Swiss 10 year yields negative 12.4 basis points. Yes, it will cost you money to lend to the Swiss government for 10 years. How about the PIIGS (remember them? Portugal, Ireland, Italy, Greece, and Spain) The Irish 10 year yields 68.3 basis points. The US 10 year yield is higher than all but one of the erstwhile PIIGS – Greece.

Bubbles, bubbles everywhere, but especially in Asia. where the Chinese real estate bubble is beginning to deflate, and the Chinese economy begins to slow. Asian stocks are ignoring this however – the Nikkei 225 is up 43% over the past year, while the Hang Seng is up almost 11% in the first two weeks of April. While these markets are still well below their all-time highs, and no one is suggesting stock market bubbles, the Asian markets look frothy. China’s real estate bubble is epic and as it bursts, China will export deflation around the world. Yet another reason for the Fed to sit on their hands.

But we don’t have any bubbles in the US, right? Well, according to Bill Ackman, we do. The student loan debt market is about $1.3 trillion all in, and about 9% is in default. As he points out, there is almost no way that gets repaid. He sees some administration doing a mass debt forgiveness.

Filed under: Morning Report | 10 Comments »

Posted on April 10, 2015 by Brent Nyitray

Stocks are higher this mornings on no real news. Bonds and MBS are up.

Import prices fell .3% in March and are down 10.5% year over year. As we are seeing in the data elsewhere, the strong dollar is beginning to affect the economy. Q1 earnings will be interesting – how many multinationals will report weaker numbers due to weaker overseas demand.

Christine Lagarde of the IMF is warning that the financial markets could get bumpy when the Fed starts raising rates. Consider this: the Fed hiked rates in 94, 99, and 05. In the process, they blew up the MBS market (remember Orange County?), the stock market, and the real estate market. Asset prices are handicapping a 100% probability that the Fed can raise interest rates without any one blowing up. The Fed may in fact be able to stick the landing and exit ZIRP without a crisis, but that is not a foregone conclusion. The old market saw of “sell in May and go away” may turn out to be good advice this year.

Filed under: Morning Report | 41 Comments »