Vital Statistics:

| Last | Change | |

| S&P futures | 2915 | -6.25 |

| Oil (WTI) | 53.07 | 0.54 |

| 10 year government bond yield | 1.61% | |

| 30 year fixed rate mortgage | 3.84% |

Stocks are down this morning on no real news. Bonds and MBS are down as well.

Consumer inflation was flat in September, and is up 1.7% YOY. The core rate, which excludes some volatile commodities, rose 0.1% MOM and 2.4% YOY. Inflation continues to sit right in the range it has been historically.

Job openings fell from a downward-revised 7.17 million to 7.05 million, while initial jobless claims ticked up to 214k.

Mortgage Applications rose 5.2% last week as purchases fell 1% and refis rose 10%. The rate on a 30 year fixed conforming loan fell 9 basis points to 3.9%. Weaker-than-expected economic data drove the decrease.

Good news for the financial community: Trump is planning to sign a couple of executive orders, which will bring more sunlight on rulemaking, and will permit more public input in the federal guidance. Much of this guidance had been “rulemaking in secret” and this will give companies more of a head’s up when the regulatory agencies plan major changes in guidance. The CFPB sprung a nasty surprise on auto lenders during the Obama Administration, where they determined that any lenders who provide auto loans through dealerships are responsible for “discriminatory pricing.” It is this sort of the thing the order intends to limit.

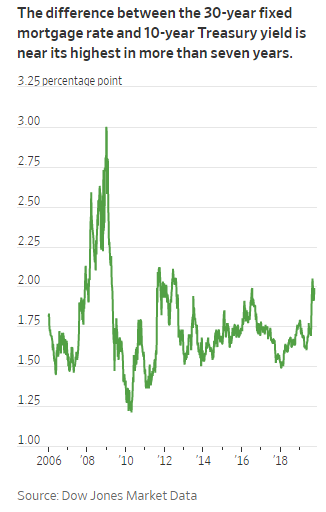

“CNBC is saying the 10 year bond yield is way lower, but I just ran a scenario and my borrower still has to pay a point and a half. What is going on?” This is a common observation these days, and it can be frustrating for both loan officers and borrowers. As the Wall Street Journal notes, that the difference between the typical mortgage rate and the 10 year bond is at a 7 year high. What is going on? First, and most important, mortgage rates are not determined by the 10 year. They are determined by mortgage backed securities, which have entirely different financial characteristics than a government bond. When rates are volatile (i.e. changing a lot in a short time period) mortgage backed security pricing will be negatively affected. In practical terms, it means that when the 10 year bond yield abruptly moves lower, it will take a few days for mortgage rates to catch up, while the time it takes to adjust to big upward moves in Treasury rates is often shorter. It also explains why it can be hard to get par pricing when you have a lot of loan level hits from Fannie (i.e. investment property, cash out refinancing, etc). The “rate stack” gets compressed and MBS investors are wary of buying high coupon securities. Bond geeks have a term for this – negative convexity – but in practical terms it means that moves in the 10 year don’t directly carry over to mortgage rates.

Filed under: Economy, Morning Report | 23 Comments »