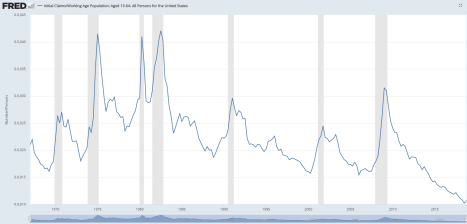

Initial Jobless Claims broke 200k, falling to 199k last week. This is the lowest level since the 1960s. For all of those fretting over a possible economic slowdown, we aren’t seeing any evidence of that in the initial jobless claims numbers. These numbers are impressive enough in of themselves, however if you correct for population growth, we are in pretty much uncharted territory.

The Index of Leading Economic Indicators fell 0.1% in December, according to the Conference Board. This follows a 0.2% increase in November. “The US LEI declined slightly in December and the recent moderation in the LEI suggests that the US economic

growth rate may slow down this year,” said Ataman Ozyildirim, Director of Economic Research at The Conference Board. “While the effects of the government shutdown are not yet reflected here, the LEI suggests that the economy could decelerate towards 2 percent growth by the end of 2019.”

Adjustable rate mortgage are making a comeback, at least according to the latest Ellie Mae Origination Insight Report. ARMs accounted for 9.2% of all originations in December, up from 8.8% in November. Purchases accounted for 71% of all originations, and other indicators like FICO, DTIs, and cycle times were largely unchanged.

Dueling bills to re-open government failed in the Senate yesterday. Talks have resumed between the parties to find a compromise everyone can live with.

The Fed is contemplating an earlier end to the tapering process than the market has been anticipating. The Fed’s balance sheet pre-crisis was about $800 billion. It peaked around $4.5 trillion and has fallen to something like $4.1 trillion since they began letting some of the portfolio run off (i.e letting bonds mature and not re-investing the proceeds). The market thought the Fed would likely return to pre-crisis levels, however the consensus is that probably won’t happen as it could create issues with banking reserves. What does that mean for the mortgage industry? At least for the moment it means that there will be more incremental demand for TBAs from the Fed, which will mean lower rates, at least at the margin.

Housing reform may be a front-burner issue again, as lawmakers pledge to do something with Fan and Fred.

Filed under: Economy | 7 Comments »