Vital Statistics:

| Last | Change | |

| S&P futures | 2653.73 | -17.75 |

| Eurostoxx index | 355.2 | -1.16 |

| Oil (WTI) | 52.83 | -0.97 |

| 10 year government bond yield | 2.76% | |

| 30 year fixed rate mortgage | 4.48% |

Stocks are down this morning on overseas weakness. Bonds and MBS are up.

Today begins the World Economic Forum in Davos. For the most part, it is basically an event where CNBC interviews hedge fund managers and government officials in the snow, however there is always the chance that someone could say something market moving.

Dave Stevens (formerly head of the MBA) outlines some of the effects of the shutdown on the mortgage business. For most lenders, the shutdown is a non-issue. 4506-Ts, social security, and flood insurance is not impacted. Lenders located in areas where there are a high quantity of government workers are unable to get VOEs for furloughed workers. This is beginning to impact closings – while the GSEs will permit loans to close without a VVOE from the government, these loans are ineligible for sale until this is done. While this won’t impact lenders with a balance sheet (i.e. banks), most independent mortgage originators won’t be able to hold a funded loan and wait out the shutdown.

Industrial Production rose 0.3% in December, while manufacturing production rose 1.1%. Capacity Utilization ticked up to 78.7%. Motor vehicles and construction products drove the increase.

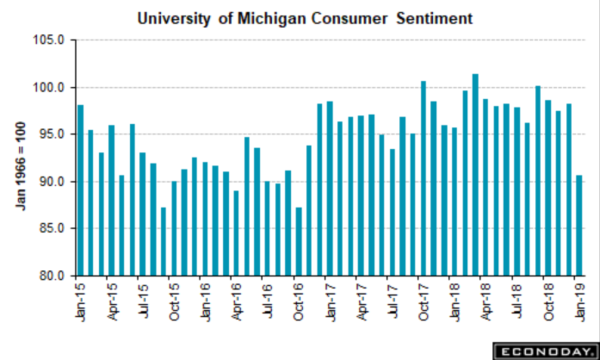

Consumer sentiment plunged in early January according to the University of Michigan consumer sentiment survey. Whether this is shutdown driven or not is anyone’s guess, but it does add fuel to the argument that the Fed went too far in 2018. The big change – future expectations.

China’s growth has slowed to the lowest levels in almost 3 decades – falling to 6.4% in the fourth quarter. The government does have some levers to push, however the bigger concern is their real estate bubble, which is vulnerable. Consumer spending is also decelerating as well, albeit from a torrid pace. The biggest effect on the US would be to hold a lid on interest rate increases and to slow down global growth. The effect of a Chinese recession will probably have the same sort of effect that Japan had in 1990 – depressing global growth, lowering import prices and allowing countries to grow without goods and services inflation.

The FHFA is not going to defend the constitutionality of its structure. The Fifth Circuit ruled in July that the FHFA is unconstitutional in that it has too much power and violates the separation of powers. The previous head of FHFA – Mel Watt – planned to appeal the decision, however the Trump Administration agrees with the ruling and will not contest it. The decision from the Fifth also ruled that the government’s current net worth sweep (in other words, all profits from the GSEs go straight to Treasury) is Constitutional. So, basically the net effect would maintain the current structure, but also allow the President to fire the head of the FHFA at will.

Note that Mark Calabria (the Trump nominee to run FHFA) is not a huge fan of securitization in general and all of the general subsidies the government puts in the US residential real estate market.

Filed under: Economy, Morning Report | 23 Comments »