Vital Statistics:

| Last | Change | |

| S&P Futures | 2689.8 | 2.0 |

| Eurostoxx Index | 390.0 | -0.7 |

| Oil (WTI) | 58.0 | -0.4 |

| US dollar index | 86.8 | 0.0 |

| 10 Year Govt Bond Yield | 2.49% | |

| Current Coupon Fannie Mae TBA | 102.531 | |

| Current Coupon Ginnie Mae TBA | 103.375 | |

| 30 Year Fixed Rate Mortgage | 3.88 |

Stocks are up this morning on no real news. Bonds and MBS are flat.

This should be a relatively quiet day as bonds close early heading into the long holiday weekend.

Durable Goods orders increase 1.3% MOM / 8.2% YOY in November, coming in below analyst estimates. A surge in aircraft orders drove the increase. Core capital goods orders (a good proxy for business capital expenditures) rose 8.1% YOY.

Personal incomes rose 0.3% in October, slightly below the Street estimate of 0.4%. Consumer spending was better than expected, rising smartly at 0.6%. Inflation remains nowhere to be found, with the core PCE up 0.1% MOM and 1.5% YOY. The low inflation numbers certainly give the Fed some breathing room, although tax reform will probably push them to be more aggressive. Especially since 9 companies so far have announced wage increases based on tax reform.

The Fed Funds futures are currently handicapping a 5% probability of no hikes in 2018, a 21% probability of a single 25 basis point hike, a 35% chance of 50, a 27% chance of 75, and a 10% chance of 100.

Bitcoin is crashing right now, down 25% from yesterday. I was asked how Bitcoin would affect the real estate market. My view was that Bitcoin is simply so volatile that I cannot imagine both a buyer and seller being comfortable quoting a house in bitcoin. I just don’t see someone trying to sell their house for 25 bitcoin. Second, the financing has to be in dollars as no banks lend in bitcoin yet, and I cannot imagine what the interest rate for a bitcoin loan would be. So no, it may be accepted by your local store, however it is more of a novelty at this point. Will that change? Who knows? Will Bitcoin be dominant cryptocurrency or will it be like Classmates.com or MySpace – early adopters that got crushed later on by Facebook?

Bloomberg takes a look at the state of housing entering 2018. Tight inventory, builder confidence, and a growing economy point to a strong housing market next year. On the other side of the coin, the drop in the mortgage interest deduction could hurt homes at the top end, while the larger standard deduction may lower the incentive to buy versus rent for many at the lower end of the income scale. IMO, the negatives are marginal compared to the positives.

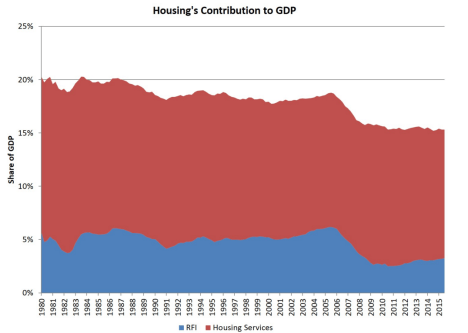

Don’t forget, housing’s contribution to GDP is way, way below historical levels. If 2018 is the year homebuilding finally breaks out, it will have an ousized effect on GDP growth. Labor shortages might be the bottleneck, but as wages rise, they attract new workers so that state of affairs doesn’t last long. Swinging a hammer pays a lot more than slinging burgers.

90 day delinquencies spiked in November, according to Black Knight Financial Services. 85% of the spike is attributed to the hurricanes, so it doesn’t really tell us anything about the state of the economy.

Finally, happy holidays to all!

Filed under: Economy, Morning Report | 10 Comments »