Vital Statistics:

| Last | Change | |

| S&P Futures | 2465.3 | -7.0 |

| Eurostoxx Index | 378.7 | -3.6 |

| Oil (WTI) | 49.1 | 0.0 |

| US dollar index | 86.2 | -0.3 |

| 10 Year Govt Bond Yield | 2.30% | |

| Current Coupon Fannie Mae TBA | 102.93 | |

| Current Coupon Ginnie Mae TBA | 103.81 | |

| 30 Year Fixed Rate Mortgage | 3.95 |

Stocks are lower this morning on overseas weakness. Bonds and MBS are flat.

The advance estimate for second quarter GDP came in at 2.6%, in line with expectations. This is an increase from the first quarter estimate of 1.2%. Personal consumption increased 2.8%, while the price index increased 1% while the savings rate inched down. This should give the Fed the room to maintain interest rates at this level if they choose to do so.

The employment cost index rose 0.5% in the second quarter and is up 2.2% YOY. Wages and salaries increased 0.5% and benefit costs increased 0.6%.

Consumer sentiment edged up in July, according to the University of Michigan survey.

I had some questions yesterday regarding LIBOR and what happens to ARMs once it is gone in 2021? The short answer is that nobody knows for sure. The US will probably migrate to some other repo rate to set short term rates. Perhaps once LIBOR goes away, there will be a LIBOR reference rate which is pegged to whatever short term rate is being used and will move at a constant spread to that rate.

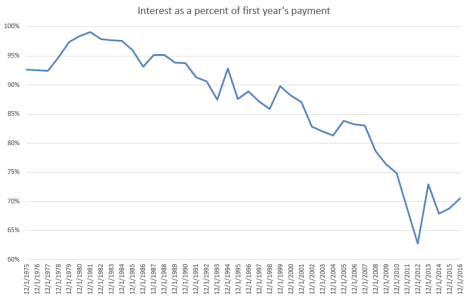

I was discussing housing affordability a couple days ago and talked about mortgage payments as a function of income over time. I showed that the post bubble days hit 40 year lows (at least) and that we are still well below historical levels. The issue with that analysis is that it ignores the tax effects of the mortgage interest deduction, which really mattered in the late 70s / early 80s when tax rates and interest rates were much higher. Up until the mid 80s, the marginal tax rate for the median income was between 22% and 24%. It has been 15% ever since. Also, when interest rates were much higher, the vast majority of your payments for the first few years went to interest, not principal – in fact when mortgage rates were 17%, 99% of your first year’s payment went to interest. Today, that number is much lower, and even ticked below 70% in 2012. Check out the chart below:

That chart also speaks to how much quicker one can build equity simply by paying their mortgage on time. Back in the 70s / 80s, you were probably lucky to have enough home price appreciation and principal paid to cover your closing costs if you moved after a few years. Today, you have both strong home price appreciation and a higher principal payment percentage. This helps emphasize how real estate is a great way to build wealth.

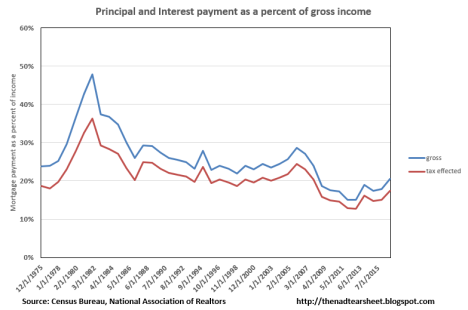

Here is the chart comparing the gross percentage of income that a mortgage payment consumed over time and also the tax effected percentage: As you can see, it is pretty linear, and we are still in a great position now compared to 30 years ago.

Filed under: Economy, Morning Report | 23 Comments »