Vital Statistics:

| Last | Change | |

| S&P Futures | 2475.8 | 4.3 |

| Eurostoxx Index | 387.3 | 1.8 |

| Oil (WTI) | 47.4 | 0.3 |

| US dollar index | 87.2 | 0.2 |

| 10 Year Govt Bond Yield | 2.26% | |

| Current Coupon Fannie Mae TBA | 103.31 | |

| Current Coupon Ginnie Mae TBA | 104.375 | |

| 30 Year Fixed Rate Mortgage | 3.96 |

Stocks are up this morning as global central banks remain easy. Bonds and MBS are up small.

The Index of Leading Economic Indicators jumped 0.6% in June, which is forecasting an acceleration in the economy going forward.

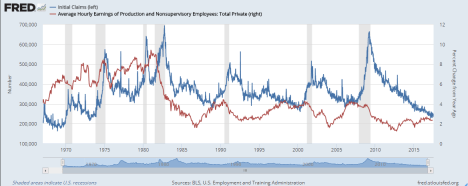

Initial Jobless claims fell to 233k, which is a 9 week low. The last time we were at similar levels was the early 1970s, when the Vietnam War was still raging. I have plotted initial jobless claims (left axis) versus wage inflation (right axis). You can see the inverse correlation, and it also suggests that with claims this low, we should be seeing wage inflation. Of course inflation has an influence as well, and the late 60s / 70s were characterized by inflation. However, pressures seem to be building, and we are seeing wage inflation at the lowest end of the spectrum – low wage workers.

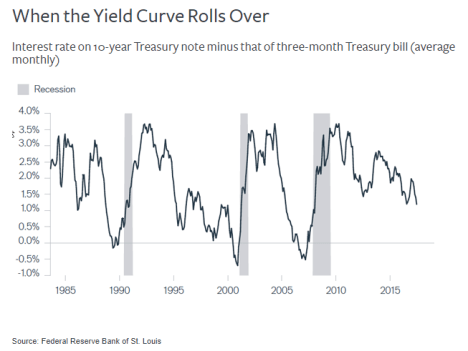

Bill Gross looks at the shape of the yield curve and warns investors not to read too much into it, since the curve is being manipulated by central bankers worldwide. The chart below shows the difference in yield between the 10 year bond and the 3 month T-bill. That difference has historically been somewhat predictive of recessions, especially when it has inverted. While the current spread is nowhere near zero, the trend is certainly heading that way. Does that mean a recession is imminent? His point is that we are really in an apples-to-oranges comparison with QE. Global central bank buying of sovereign debt is pushing that spread downward, and the relevant question is where would the yield curve be without the Fed’s (and other global central banks’) buying?

He does make the point that Corporate America is more leveraged than before, however with rates so low, the debt service (actual interest paid) is much less than it was historically. You see that in households too. Total debt has risen past the old highs, however the debt service (interest paid as a percent of disposable income) is close to the lows.

The NYC luxury real estate market is soft, and many luxury sellers in Greenwich, CT are pulling the plug on sales. Of the homes in this market ($4.5 million+) days on market was 319, up by over 100 days. Some sellers have had to cut their price by 60% to entice a buyer. FWIW, I see very little building in this area of the country – only a handful of spec homes have been built, and they haven’t sold yet.

Filed under: Economy, Morning Report | 46 Comments »