Vital Statistics:

| Last | Change | |

| S&P Futures | 2379.0 | -3.0 |

| Eurostoxx Index | 374.5 | -1.1 |

| Oil (WTI) | 52.8 | 0.2 |

| US dollar index | 91.8 | |

| 10 Year Govt Bond Yield | 2.49% | |

| Current Coupon Fannie Mae TBA | 101.72 | |

| Current Coupon Ginnie Mae TBA | 103.15 | |

| 30 Year Fixed Rate Mortgage | 4.09 |

Stocks are still taking a breather after a nice run. Bonds and MBS are down.

The focus today will be all of the Fed-speak, with Janet Yellen and Stanley Fischer speaking around lunchtime. The Fed enters their quiet period ahead of the March FOMC meeting tomorrow. The markets have gone from pricing a March hike as a 30% chance to an almost certainty over the past several weeks.

The ISM Non-Manufacturing index improved in January, as business activity and new orders (especially exports) led the charge. Employment ticked up slightly. The reading of 57.6 was the highest since October 2015.

Ben Carson was confirmed as the new HUD Secretary yesterday on a 58-41 vote. HUD probably won’t have a lot to do with GSE reform, as that is largely a Treasury function. Ben Carson is a neurosurgeon by trade, and his public record on housing was limited to an editorial criticizing Obama’s enforcement of the Fair Housing Act. During his hearing, however he praised the Fair Housing Act as an important piece of legislation. The safety of public housing is a priority for him, and he plans to increase HUD’s efforts to eliminate lead paint, mold, etc from public housing. He wants to continue to advance HUD’s mission of financing low income / credit / first time homebuyers while introducing private capital and protecting taxpayers.

Snap priced its IPO yesterday, where it had a 44% gain on the first day of trading. Many IPOs lately have not seen a big pop on day 1, so this is a bit of an anomaly. The lack of big gains from IPOs represents the drop in commission revenue and the balance of power between issuers and the buy side (a big jump in price on the first day means that the IPO was underpriced and the issuer is leaving money on the table). In the past, the banks were more worried about keeping the big mutual funds happy since they were a steady source of commission revenue, while issuers would typically do a deal and then go away for a while. Nowadays, commissions are basically nothing, so banks are more concerned with keeping issuers happy than they are with keeping, say Fidelity happy. When I started in the business, commissions were 5 cents a share, and bid-ask spreads were an eighth. Today, commissions are less than half a penny a share and bid-ask spreads are 1/10 of a cent on big liquid stocks.

As a general rule, when the stock price is telling you one thing and the bonds are telling you another, go with what the bonds are telling you. We are seeing a bit of that right now with stocks and bonds – as stocks are off to the races on the reflation trade, bonds have been in a range post-election. Bonds are saying either (a) fiscal stimulus is not going to happen or (b) fiscal stimulus isn’t going to work. That is certainly a fair take, and I do think rates have gotten a bit ahead of themselves. On the other hand, interest rates have been so heavily manipulated by central banks over the past decade, that the signal-to-noise ratio is lower than normal. Ultimately this is a criticism of monetary policy has gotten short shrift in the public debate: that interest rates are an important signal that the economy uses to allocate capital. When central banks manipulate rates to help goose the economy, those signals are distorted, and the typical effect is a bubble. Keynes and Hayek explain it to you here.

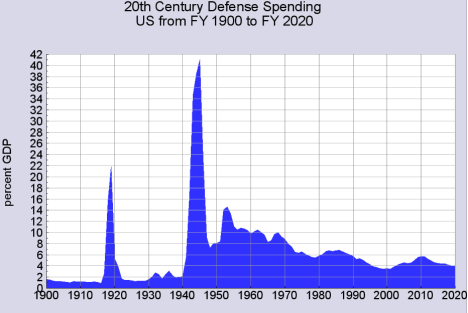

One of Donald Trump’s plans is to increase defense spending. The proposed increase is anywhere from $20 billion to $54 billion, from the current $582 billion level (or 3.1% of GDP). Here is a chart of defense spending over the past century as a percent of GDP in order to put current levels into perspective:

Solid tips for doing your taxes this year.

Filed under: Economy, Morning Report | 41 Comments »