Posted on May 14, 2015 by Brent Nyitray

Markets are higher this morning as bonds are rallying and the dollar weakens

Initial jobless claims came in at 264k, another strong reading. The fear that there would be mass layoffs in the oil patch so far has not come true. Plus, oil is now rebounding as firms have adjusted to the new price levels.

Inflation remains nowhere to be found, with the producer price index falling 0.4% in April. Ex food and energy, prices are up .7% on a year over year basis. This is about 1/3 of the level the Fed would like to see.

The Bloomberg Consumer Comfort Index fell slightly to 43.5 last week. 1/3 think the state of the economy is positive, while 2/3 think it is negative. Personal finances, are a net positive however. So it seems the perception of the economy is a bit worse than people’ actual financial situations.

Former Maryland Governor Martin O’Malley is planning to enter the 2016 race, adding at least the appearance of a speed bump to Hillary’s coronation as the Democratic candidate. Both O’Malley and Bernie Sanders (I-VT) plan to run to Hillary’s left. So far, Hillary has managed to avoid taking any questions about the Trans Pacific Partnership, the trade deal that has become a litmus test on the left. The media doesn’t want to mess up Hillary’s candidacy, so they are leaving her alone on this one.

Filed under: Morning Report | 17 Comments »

Posted on May 13, 2015 by Brent Nyitray

Markets are flattish this morning after a disappointing retail sales number. Bonds and MBS are up after European bond markets mount a small rally.

Retail Sales were flat in April after an upward-revised increase of 1.1% in March. While economists had hoped that consumers would spend their gasoline savings at the mall, they aren’t – they are paying down debt. The control group number, which strips out some of the more volatile elements and is an input to GDP was flat as well. Expect strategists to start taking down Q2 GDP estimates and moving out their forecast for the first rate hike.

Mortgage Applications fell 3.5% last week, which was unsurprising given the bond market sell off. Purchases were down .2%, while refis were down 5.9%. The 30 year fixed rate mortgage increased 7 basis points last week.

Who says the US cannot compete in low value-added manufacturing? It turns out we can, at least in energy-intensive manufacturing. Cheap natural gas in the US are offsetting the cheap labor costs overseas (which are rising) and manufacturing is returning. Case in point: plastics. It isn’t just the cheaper electricity – it is the feedstocks that come from natural gas. This will do more to turn around our economy than anything will.

Filed under: Morning Report | 32 Comments »

Posted on May 12, 2015 by Brent Nyitray

Stocks and bonds are lower as the bloodbath in European bonds continues. The German Bund is trading at 67 basis points. The reversal in Eurobonds has been nothing short of astounding.

Small business optimism bounced back in April, according to the NFIB. That said, optimism still has not fully recovered from Q1’s weakness. Labor markets continue to improve slowly but surely.

The National Fair Housing Alliance is suing Fannie Mae for racial discrimination in lending. “Fannie Mae fails to perform basic maintenance and marketing tasks for foreclosed homes it owns in African

American and Latino neighborhoods, while consistently maintaining its foreclosed properties in white neighborhoods.” I wonder how much of this is due to the fact that in some places like Toledo OH, Detroit MI, and Camden NJ, there simply isn’t a bid for these properties given their stripped state and unpaid back taxes.

Filed under: Morning Report | 43 Comments »

Posted on May 11, 2015 by Brent Nyitray

Stocks are flattish on no real news. Bonds and MBS are down.

The week after the jobs report is usually pretty data-light and this week is no exception. The highlights will be retail sales on Wednesday and industrial data on Friday.

The Fed may not pursue a path of steady consecutive 25 basis point increases in the Fed Funds rate when they start hiking rates. Interestingly, the article posits that the Fed wants to learn the lesson of the last hike cycle – in which they tightened too predictably, and which some believe caused the real estate bubble. If the Fed truly believes that rate hikes caused the real estate bubble, and everything was fine in the markets before then, it shows we have learned absolutely nothing from 2008.

Filed under: Morning Report | 26 Comments »

Posted on May 8, 2015 by Brent Nyitray

Stocks are higher this morning after the jobs report. Bonds and MBS are up big. European sovereign debt is rallying hard this morning.

- Nonfarm payrolls 223k

- two month payroll revision -39

- March payrolls revised to 85k from 126k

- Unemployment rate 5.4%

- Average Hourly earnings +.1%

- Labor Force Participation rate 62.8%

Overall, the report isn’t bad, and it had something for everyone to like. Stocks liked the unemployment rate and the fact that payrolls rebounded in April, while bonds could hang their hat on the weak hourly earnings number.

Wellington Denahan, CEO of mortgage REIT Annaly Capital had some criticism of the Fed and the effects of QE. Money quote: “Since 2009 when the experiment began, global bond markets have increased in value by roughly $17 trillion, or the size of the U.S. economy, while global equity markets have increased in value by a staggering $40 trillion. Yet the American wage earners have gained a relatively paltry $722 billion in comparison during the same period. Or to put it more clearly, for every dollar gained by the American worker, the global equity markets have the gained $55.” As much as people complain about inequality, almost nobody asks if Fed policy in general, not just QE, is behind the rising inequality as the Fed creates serial bubbles. The left loves to point out that inequality began accelerating in 1979 (in order to blame it all on Reagan), however the dual mandate began right around that time as well, and as such began the mother of all rallies in stocks, bonds, and real estate.

Filed under: Morning Report | 44 Comments »

Posted on May 7, 2015 by Brent Nyitray

Stocks are down small as we get a few mixed signals on the job market. Bonds and MBS are holding in there despite another big sell-off in the German Bund, which now yields almost 65 basis points – this is an increase of 57 basis points in about two weeks. Welcome to the new QE normal, where sovereign debt trades with the volatility of tech stocks.

Note that the volatility in the Bund has hurt Bill Gross, who considers it “the short of a lifetime.” Unfortunately, it looks like Bill sold options against the Bund, betting it would trade in a narrow range, and is now taking some gas on his position given the furious sell-off Euro sovereign debt. Welcome to the wonderful world of negative convexity, which is the bane of mortgage bankers globally.

The volatility in bonds has hurt the mortgage REITs, the latest of which is Annaly Capital, which missed yesterday. American Capital Agency struggled with the volatility as well. Interestingly, American Capital Agency was responsible for some of the outperformance in FHA / VA pricing at the end of the quarter. Ordinarily, they don’t buy Ginnie Mae TBAs as Fannies offer higher returns, but they viewed the Ginnie Mae sell off due to the change in MI was overdone, and took a position the other way. Mortgage REITs are generally most active in the secondary market for MBS, however they do dabble in TBAs and can affect loan pricing at the margin.

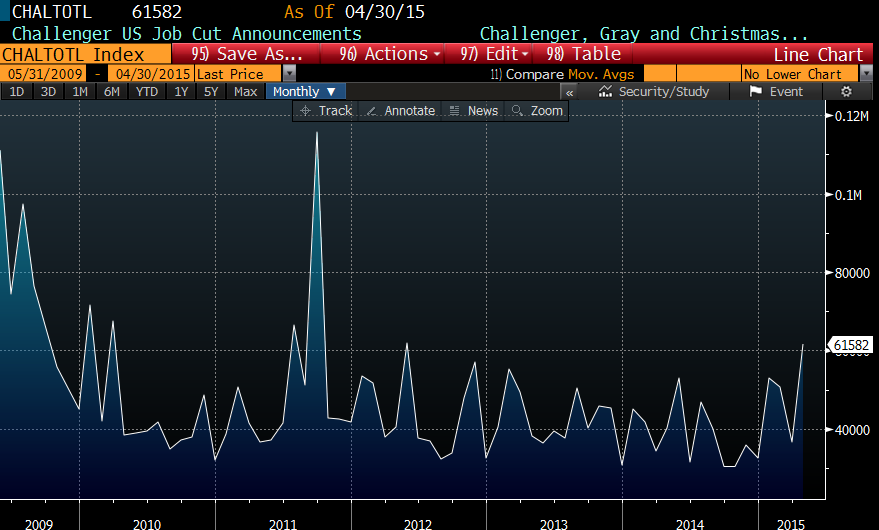

We have some mixed employment data this morning, with Challenger and Gray announced job cuts increasing 53% to 61,582 in April, which is the highest number in 3 years. About a third of these cuts are in the oil patch, as Schlumberger, Baker Hughes, and Halliburton all announced layoffs. The other big category is retail, where you are seeing layoffs as well. Ordinarily, you would expect lower energy prices to translate into higher spending at the mall, but it isn’t working out that way this time around. Blame broke Millennials who can’t find jobs, Gen-Xers who drew the candy cane card as they were hitting their peak earning years, and Baby Boomers who had to retire a little earlier than they had planned.

On the plus side, initial jobless claims hit 265,000 last week, which is still flirting with 15 year lows. One thing to keep in mind between the initial jobless claims report and Challenger: Challenger looks at announced job cuts. Often, those cuts end up not happening because the business turns around first.

The Bloomberg Consumer Comfort Index fell to 43.7 last week as consumers still fret about the state of the economy. An index reading of 50 is considered “normalcy.”

Janet Yellen ventured into Alan Greenspan territory yesterday when she remarked stock prices are still “quite high.” It didn’t have the effect on markets that Alan Greenspan’s “irrational exuberance” comments did, as stocks largely ignored the warning. Memo to central bankers: You don’t have a bubble in stocks. You have a bubble in sovereign debt

Filed under: Morning Report | 19 Comments »

Posted on May 6, 2015 by Brent Nyitray

Stocks are higher this morning after yesterday’s bloodbath. Bonds and MBS are flat

The ADP Employment Change index is forecasting a weak employment report this Friday. They report shows 169,000 jobs were created in April, which was lower than the 200,000 estimate. The Street is forecasting an increase of 230,000 for Friday. This is the weakest report in over a year, and you can see the marked slowdown beginning this year. If the early weakness was just weather-related, then you should see some sort of rebound. You aren’t.

Some more disappointing data this morning – productivity fell 1.9% in the first quarter after falling 2.1% in the fourth quarter. Output fell .2% while compensation increased 6.2%. Unit Labor Costs rose 5%. Lower productivity has been driven by a combination of a stronger labor market and weak GDP growth, so it isn’t necessarily a bad thing, at least in the short term. It means that we could still see improvement in the labor market despite weak economic growth.

Mortgage Applications fell 4.6% last week as purchases rose .8% and refis fell 8.3%. Bonds got slammed last week, so that isn’t a surprise. The 30 year fixed rate mortgage rate rose to 3.93% from 3.85%. Refis as a percentage of loans fell to 52.5%.

Foreclosures fell to 2.22%, according to the MBA. Delinquencies fell to 5.54%.

As the rhetoric between Greek Prime Minister Alexis Tsipras and the EU gets more and more heated, the ECB is wrestling with how much of a haircut to demand on Greek collateral. The machinations between the Greeks and the EU are driving Euro yields, which are driving US yields. “The fundamentals have not changed, but bond markets have,” said Christoph Rieger, the Frankfurt-based head of fixed income strategy at Commerzbank AG. “The European bond markets are broken, hampered by low yields, high regulation and central bank intervention. Markets will have to get used to these erratic swings.” The European situation is why so many bond strategists got it so wrong in the US over the past year and explains why bonds are selling off in the US despite some weaker economic data.

Home Prices rose 5.9% annually, according to CoreLogic. A combination of tight inventory, low mortgage rates, and improving confidence is the culprit. Of course we need wage growth to make this actually sustainable, and it looks like we could be seeing the start of wage growth, at least according to the Employment Cost Index.

Filed under: Morning Report | 35 Comments »

Posted on May 5, 2015 by Brent Nyitray

Stocks are lower this morning on economic data. Bonds and MBS are getting slammed.

Bonds in the US have been buffeted by the volatility in the European bond markets as

optimism and pessimism over a bailout wax and wane. The German Bund is now trading at 51 basis points after hitting 7.5 bps about two weeks ago. The snapback has been vicious and caught a lot of people on the wrong side of the boat.

Chart: German 10 year bond yield:

The ISM Services Index rose to 57.8 in April from 56.5 in March. These are strong numbers, which should bode well for the jobs report on Friday.

Economic optimism fell, however from 51.3 to 49.7. While a lot of things figure into these sentiment statistics, they are very sensitive to gasoline prices.

Oil is back over $60 a barrel as the supply glut begins to dry up. This could bump up the inflation numbers a bit, which would be good news for the Fed, as long as it is stays muted and inflation holds around 2%. If it goes above, get ready for all the “The Fed is Behind The Curve” handwringing. That would be Hillary’s nightmare scenario.

Note David Einhorn

took aim at fracking (and specifically Pioneer Natural Resources) with regard to profitability at a value investing conference.

Filed under: Morning Report | 9 Comments »

Posted on May 4, 2015 by Brent Nyitray

Stocks are higher this morning after a stronger-than-expected European manufacturing report eased fears of deflation. Bonds and MBS are up small.

This week has some important economic data, with the biggest being the jobs report on Friday. The market has been backing away from the June rate hike forecast, and IMO the jobs report will have to be outstanding (300k+ payrolls, and a meaningful increase in wages) to bring a June tightening back into play. We will also get productivity and unit labor costs this week, which will figure heavily into the Fed’s thinking.

The ISM New York Index increased to 58.1 from 50 in March. Factory Orders rose 2.1%, topping the analyst 2% forecast.

A few stronger than expected economic reports turned around G7 debt in a hurry. The German Bund, which hit a record low of 7.5 basis points two weeks ago is now trading at a 41.5 basis point yield, which is a 3 month high. G7 sovereigns have been a one-way bet for a long time, so a sell-off is to be expected.

Bill Gross’s latest Investment Outlook is good. He is calling for the end of the secular bull market in bonds and is recommending shorting the Bund (good trade over the past two weeks). He also believes that cheap credit, which has fueled the bull market in stocks is going to slowly dry up. Is he suggesting to sell your portfolio and bury the cash in the back yard? Not at all. However he is arguing that the trade going forward may be focusing on lightly levered income trades instead of searching for capital gains.

Filed under: Morning Report | 9 Comments »

Posted on May 1, 2015 by markinaustin

About Labour, this: Mr Miliband is fond of comparing his progressivism to that of Teddy Roosevelt, America’s trustbusting president. But the comparison is false. Rather than using the state to boost competition, Mr Miliband wants a heavier state hand in markets—which betrays an ill-founded faith in the ingenuity and wisdom of government. Even a brief, limited intervention can cast a lasting pall over investment and enterprise—witness the 75% income-tax rate of France’s president, François Hollande. The danger is all the greater because a Labour government looks fated to depend on the SNP, which leans strongly to the left. http://tinyurl.com/nwqjron

Filed under: Elections, EU, UK | 1 Comment »