Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1925.0 | -3.3 | -0.17% |

| Eurostoxx Index | 3263.1 | -19.8 | -0.60% |

| Oil (WTI) | 107.1 | 0.2 | 0.22% |

| LIBOR | 0.231 | -0.002 | -0.65% |

| US Dollar Index (DXY) | 80.61 | 0.035 | 0.04% |

| 10 Year Govt Bond Yield | 2.59% | -0.02% | |

| Current Coupon Ginnie Mae TBA | 106.5 | 0.0 | |

| Current Coupon Fannie Mae TBA | 105.3 | 0.1 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.22 |

Markets are lower this morning on no real news. Bonds and MBS are up

Big week coming up with respect to economic data and potential bond market moves. First, we have some important data today with industrial production / capacity utilization. Tomorrow, we get housing starts and building permits. Finally on Wednesday, we get the results of the FOMC meeting. I believe the Fed will be refreshing its economic forecasts at this meeting as well.

The NAHB Homebuilder Sentiment Index rose to 49 in June from 45 in May. An index level of 50 is considered to be “good building conditions.” The homebuilding industry has a couple of headwinds to deal with – first the lack of skilled labor, and second caution on the part of

Empire Manufacturing came in at 19.28, the highest reading since 2010. New orders drove the increase. Employment conditions continue to improve, as we are seeing a small increase in employment levels and hours worked. The six month outlook remains optimistic.

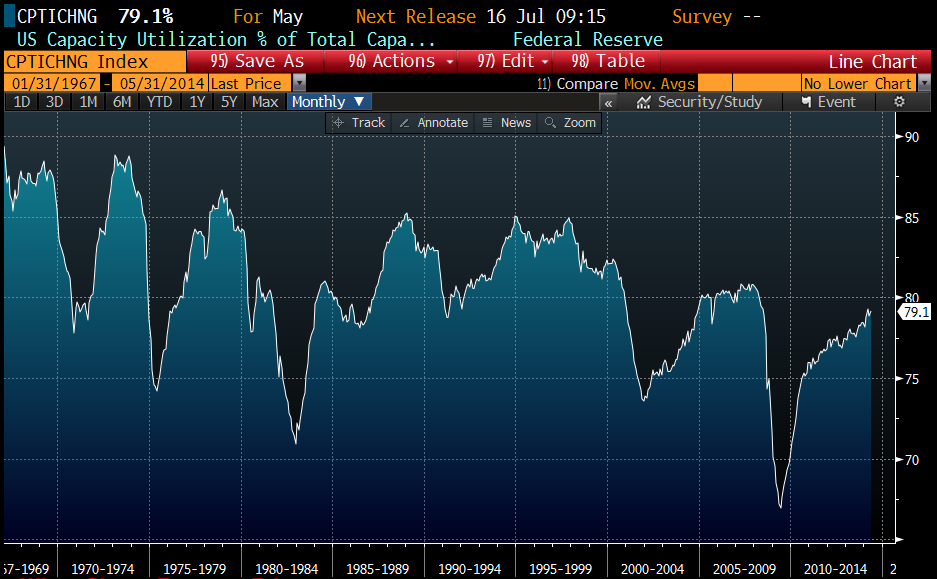

Industrial Production increased .6% in May. Capacity Utilization rose to 79.1% and Manufacturing production rose .6%. April’s numbers were revised upward. Durable goods production was up 5.3% year-over-year.

Another Merger Monday with a couple of big deals. Medtronic agrees to buy Covidien for $43 billion and Level 3 agrees to buy TW Telecom for $7 billion. A combination of inflated stock prices and low interest rates pretty much means we should continue to see M&A activity. The Medtronic / Covidien deal is partially driven by tax considerations (remember that obamacare increased taxes on medical device companies), so expect a lot of kvetching out of the left about this deal.

The IMF cut its 2014 growth estimate for the US from 2.8% to 2%. They are forecasting 2015 growth of 3%. They expect the US to maintain ZIRP past mid-2015. Interestingly, the IMF calls for raising taxes, increasing spending, and raising the minimum wage. Christine Lagarde must have been drinking Dr. Cowbell’s kool aid.

Filed under: Morning Report | 28 Comments »