Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1886.0 | 1.1 | 0.06% |

| Eurostoxx Index | 3178.4 | -8.7 | -0.27% |

| Oil (WTI) | 103.9 | -0.2 | -0.18% |

| LIBOR | 0.227 | 0.000 | -0.09% |

| US Dollar Index (DXY) | 80.17 | 0.076 | 0.09% |

| 10 Year Govt Bond Yield | 2.54% | 0.00% | |

| Current Coupon Ginnie Mae TBA | 106.5 | 0.0 | |

| Current Coupon Fannie Mae TBA | 105.6 | 0.0 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.17 |

Markets are flattish after retailers Best Buy and Sears missed earnings estimates. Bonds and MBS are flat.

We finally got some economic data this morning, starting with the Chicago Fed National Activity Index, which came in below expectations. Initial Jobless Claims rose from 298k to 326k. The Markit May preliminary PMI came in at 56.2, a little better than expectations and consumer comfort remained on the low side. Finally, the Index of Leading Economic Indicators fell to .4%

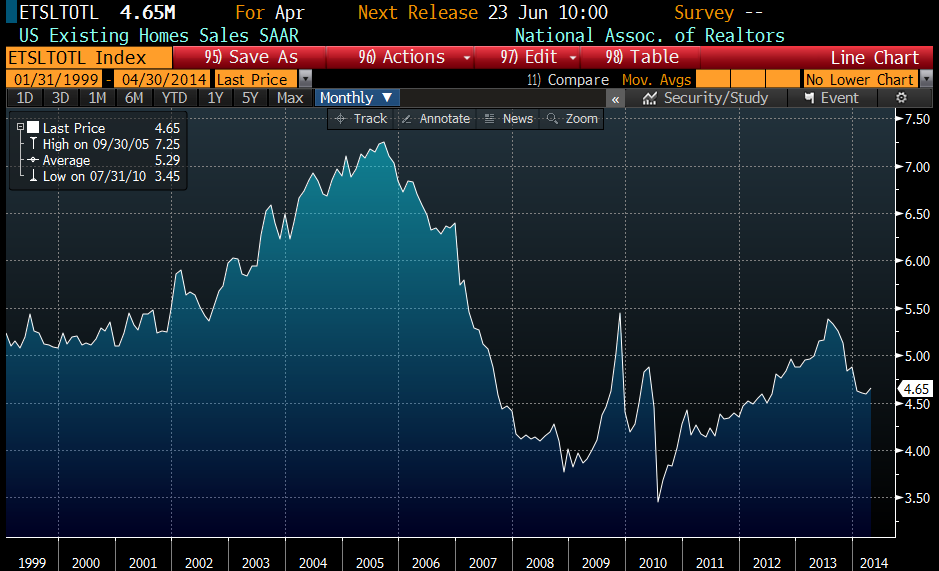

Existing home sales increased to a 4.65 million rate in April, which was an increase from the prior month, but below street expectations. As anyone in the mortgage business can tell you, it is tough out there. Housing continues to punch below its weight and sales continue to be at depressed levels. On the bright side, between 40% and 50% of these transactions are all cash, compared to 20% historically. So, there is a lot of potential business out there, but we need the first time homebuyer to step up.

The new buzzword for the Fed is now “normalization,” which is all honesty is simply a euphemism for “raising rates.” There was nothing earth-shattering in the FOMC minutes yesterday (the bond market barely noticed), but the Fed did muse a bit on how monetary policy will function with a balance sheet the size of Jupiter. People forget that we are truly in uncharted territory here, with a Fed balance sheet of 4.3 trillion in assets vs 900 billion at the beginning of 2008.

The Fed noted the strength in the March industrial data, but did not pick up on the reversal in the April numbers. Even though Q1 GDP growth was below the Fed’s forecast, they chose not to revise their 2014 GDP estimates downward, as they expect a rebound in the second half of the year. Overall, if you look at the trend of the Fed’s forecasts and revisions, GDP, unemployment, and inflation forecasts have been progressively lowered. I almost wonder if the Fed’s economic models were created during an environment where recessions were caused by the classic inflation / inventory buildup cycle and that model is simply irrelevant in this climate, where the recession is caused by a burst asset bubble.

The latest CoreLogic Market Pulse is out, and it has some good articles as usual. They address short sales and the expiration of the Mortgage Debt Forgiveness Relief Act. So far, it looks like the expiration of the tax relief (mortgage debt principal mods are now treated as taxable income, where before they were not) is crimping short sales, exacerbating an already tight inventory situation. Conversely, construction employment is beginning to increase, especially in Florida. I expect construction (especially residential construction) will be the catalyst that sends us from 2% GDP growth to 3% + GDP growth. The homebuilders have been able to report increased revenues primarily by increasing average selling prices. The typical publicly-traded homebuilder was reporting double digit increases in ASPs and high single digit drops in deliveries. Once they hit the ceiling on prices (and traffic patterns suggest we are close), they will simply have to push through volume if they want to report growth. That will begin the virtuous cycle. I was hoping this would be a 2014 event, but it is looking more and more like a 2015 event. CoreLogic also discusses the excuse du jour for weak housing starts – bad weather – and finds that it doesn’t fully explain what has been going on. RTWT.

Filed under: Morning Report | 40 Comments »