Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1742.2 | -7.2 | -0.41% |

| Eurostoxx Index | 3021.7 | -24.1 | -0.79% |

| Oil (WTI) | 96.59 | -1.7 | -1.74% |

| LIBOR | 0.238 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 79.31 | 0.083 | 0.10% |

| 10 Year Govt Bond Yield | 2.50% | -0.01% | |

| Current Coupon Ginnie Mae TBA | 103.9 | 0.1 | |

| Current Coupon Fannie Mae TBA | 102.7 | 0.1 | |

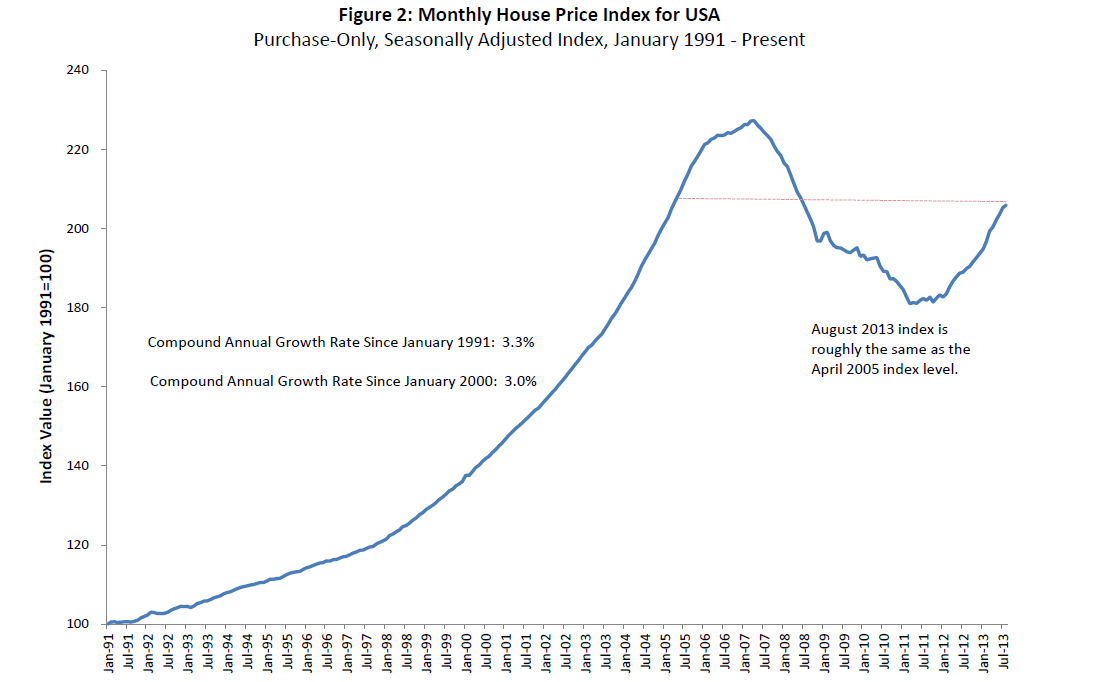

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.29 |

Markets are lower on an earnings miss from Caterpillar. Import prices rose .2% month-over-month. Bonds and MBS are up small.

Mortgage Applications fell .6% last week, which is surprising given that rates fell so much later in the week. The refi index actually fell while the Bankrate 30 year fixed rate mortgage fell 5 basis points to 4.23%. The purchase index was up small.

The FHFA Home Price index rose .3% month-over-month in August, which was lower than expected. Prices are up 8.5% year-over-year. The FHFA index only looks at houses with conforming mortgages, so it is a bit of a central tendency index in that it ignores the jumbos and the cash sales (which are usually distressed sales). The FHFA index shows the strongest recovery in home prices of all the indices out there.

Regulators gave originators a bit of breathing room by saying that originators that focus only on QM loans will not have EEOC issues if they choose to go this route. Of course that can easily change if they find that loans are not getting made in certain areas, so I would take that assurance with a grain of salt. Now that the points / fee caps pretty much make sub-$100k loans uneconomic, lets see how the Administration reacts when credit dries up at the lower price points. You think Eric Holder is going to care that CFPB made these loans money-losers? Me neither.

Flagstar Bank reported better than expected earnings this morning, although mortgage origination suffered. Total originations declined 28.9% to $7.7 billion from $10.9 billion in Q2 and $14.5 billion in Q312. Purchase activity was up 17% though. Gain on sale margin fell to 1.14% from 1.47% based on “lower hedge performance.” This is surprising given that the 30 year fixed rate mortgage started the quarter at 4.39% and ended it at 4.33%. Volatility is what kills mortgage pipeline hedging and Q3 was a bit more volatile than Q2, but not by much. Surprising result. They also made no bulk MSR sales in Q3, after having made them in Q2. Given that MSR valuations have been going up, it is surprising they haven’t been ringing the register. Perhaps they are done with their Basel III MSR selling.

One of the unintended consequences of taper-talk has been the slowing of the private label market. Lewis Ranieri’s (of Liar’s Poker fame) Shellpoint Partners pulled a jumbo bond deal after finding it could get better pricing by selling the loans outright. Investors are shunning the bonds because they are afraid that they will be holding long-duration / low yielding assets for a long time.

Filed under: Morning Report | 49 Comments »