Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1690.7 | -1.8 | -0.11% |

| Eurostoxx Index | 2918.0 | -4.9 | -0.17% |

| Oil (WTI) | 103.9 | 0.7 | 0.70% |

| LIBOR | 0.248 | -0.003 | -1.04% |

| US Dollar Index (DXY) | 80.44 | -0.120 | -0.15% |

| 10 Year Govt Bond Yield | 2.64% | -0.01% | |

| Current Coupon Ginnie Mae TBA | 105.4 | 0.0 | |

| Current Coupon Fannie Mae TBA | 104.5 | 0.0 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.32 |

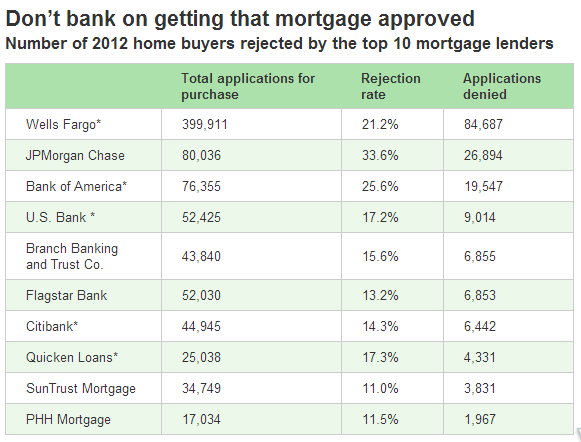

So, LOs the next time a borrower says that “Wells or JP Morgan is quoting me X% with so many points, tell them that unless they have a commitment, they are taking a risk going with a big bank. It would be a shame to go all the way through the process, only to get rejected at the last minute.

Moody’s is warning that a government shutdown may slow economic activity and would damage the nation’s credit quality. I suspect Ted Cruz knows that we aren’t going to shut down the government over obamacare, and this “filibuster” – is his last stand on the issue. Once he sits down, we’ll get a continuing resolution and a debt ceiling increase in short order. Certainly the stock market, the bond market, and the US dollar are taking that view. The risk: Democrats demand an end to the sequester and try and stick in tax hikes. I don’t think they do that because Republicans will reject that and then a government shutdown becomes a case of “he said, she said” where Democrats take some risk of getting dirty with the Republicans. Here is a list of cuts that can avert a government shutdown.

Filed under: Morning Report |

“The speech is basically a shot at mortgage bankers, payday lenders, servicers, debt collectors and other unsavory financial services folks.”

Did he address the large banks selling their servicing arms as an unintended consequences of the National Mortgage Settlement?

http://www.salon.com/2013/09/24/banks_find_appalling_new_way_to_cheat_homeowners_partner/

With regards to consumers and servicers, I would have liked to see a provision that a bank has to get consent from the mortgagee before it could sell the loan or the servicing rights.

LikeLike

“Here is a list of cuts that can avert a government shutdown.”

I think the cuts are going to be attached to the debt ceiling increase. The CR is going to be at FY2013 levels.

LikeLike

Thank you Kevin Drum.

“Even if we have a debt limit crisis, there’s zero chance that holders of treasurys will miss any payments.”

http://www.motherjones.com/kevin-drum/2013/09/investors-america-default-debt-limit-cds

LikeLike

With regards to consumers and servicers, I would have liked to see a provision that a bank has to get consent from the mortgagee before it could sell the loan or the servicing rights.

This would be impossible for mortgages – they are packaged into securities which may contain thousands of individual mortgages.

Servicing is more of an over the counter market, but for the most part, but they trade in a minimum of $100 million worth of unpaid principal balances. FWIW, I believe the MO of the CFPB is to destroy the economic value of MSRs in order to make it okay to take the servicing “asset” away from the lender to do just that. I don’t know what the unintended consequences of that would be…

LikeLike

Even without packaging, impairing the negotiability of a note would be a body blow to the market to which that note is fundamental.

LikeLike

I’d get rid of securitization entirely. Mortgages should be transferred as whole loans.

LikeLike

jnc:

I’d get rid of securitization entirely. Mortgages should be transferred as whole loans.

I don’t understand the reference to “whole loans” (a reference you have made before). Securitizations bundle loans together, they do not split a single loan into multiple parts. The loan always remains “whole”, even if sold as part of a bundle of loans. What am I missing?

LikeLike

I am surprised Kevin Drum was able to discuss credit default swaps without using the terms fraud, bankster, or sham, and attributing all of our economic woes to this toxic, completely unregulated product.

Also, why would anyone buy a CDS on a Treasury? There is a liquid market in Treasury options, so why anyone would tie themselves up with all the headaches of a CDS transaction is beyond me.

LikeLike

Worth noting

LikeLike

Brent, if the Salon piece is accurate and transferring servicers invalidates an existing modification, that’s a problem.

LikeLike

I’d get rid of securitization entirely. Mortgages should be transferred as whole loans.

I think the benefits of securitization outweigh the costs..

LikeLike

The results of the financial crisis have lead me to conclude that it has underpriced the risk of the loans, and created a Gordian Knot on actual modifications and writedowns due to the servicers not having the authority (or not wanting to exercise it due to the fear of lawsuits from the MBS holders) to cut deals.

And there’s also the various loan documentation issues associated with MERS that I would argue were a result of securitzation.

LikeLike

” Securitizations bundle loans together, they do not split a single loan into multiple parts. ”

Yes it does. See tranches.

LikeLike

jnc:

Yes it does. See tranches.

I still don’t get it. Tranches are relevant to investors, not borrowers. Tranches divide the risk of default into different pieces so that different investors face different costs on the default of a given loan. It doesn’t divide the loan itself. Basically it makes the “owners” of a defaulting loan a subset of the investors in the MBS rather than all of the investors together.

Suppose a particular CDO was not tranched (and therefore, in your view, still “whole”), and the risk of any given default within the packaged loans was equally shared by all the investors. How would this have any impact on a defaulting borrower, or the ability to modify/write down the loan?

LikeLike

I may be misunderstanding, but that was what I took to be one of the reasons why the various CDS and other instruments were so hard to unwind. They were written against tranches of the MBS’s.

LikeLike

jnc:

I may be misunderstanding, but that was what I took to be one of the reasons why the various CDS and other instruments were so hard to unwind. They were written against tranches of the MBS’s.

First a caveat…I am familiar with and have some experience with CDS, but am certainly no expert, so I may misunderstand some things myself. That being said…

We need to make sure we properly distinguish between hard assets like MBS/CDOs and derivatives like synthetic CDOs (which are, essentially, a type of CDS). It is definitely true that CDS’ were written and tranched on packages of mortgages, and I can certainly understand how these may be difficult to unwind. But they should have no impact at all on the disposition of the underlying loans, because the CDS exist entirely independently of either the underlying loan or any MBS/CDO into which the loan might have been packaged. In fact, far from the CDS making it difficult to modify or otherwise dispose of a non-performing loan, I can imagine how the exact opposite would be the case, ie it would be uncertainty over the disposition of the underlying loan that complicates the valuation/unwinding of the CDS. Remember, it being a derivative, the terms of the CDS depend upon the status of the underlying loan, not vice-versa.

When you say that servicers are unwilling to modify/write down over fears of being sued by the holders of the MBS, that makes sense to me. But I think that has to do with the fact that the “decider” of what to do with the loan is someone other than the owner(s), not because the loan is not “whole”.

LikeLike

jnc:

I’ve been trying to find out more about the history of AT&T’s monopoly. This site doesn’t really give any details, but does describe AT&T thus:

AT&T was a government-supported monopoly – a public utility – that would have to be considered a coercive monopoly.

LikeLike

Fascinating.

@PostReid: Rand Paul raised more for NJ SEN candidate Steve Lonegan than Chris Christie did — http://t.co/2H5hAvls8e

LikeLike

When a wingnut does it, it’s not a filibuster.

http://m.washingtonexaminer.com/when-is-a-filibuster-not-a-filibuster/article/2536357

Calm down freaks.

LikeLike

yesterday 2 co-workers reported each of their primary care docs is going boutique. pay $1600 a year for a membership or GTFO.

once you pay the fee, they will accept insurance.

LikeLike

“Brent, if the Salon piece is accurate and transferring servicers invalidates an existing modification, that’s a problem.”

Some surprising allegations in that article

Regarding the invalidation of an existing mod, I don’t see why Nationstar would even do that…Unless you think they are trying to fraudulently push people into foreclosure in order to get more fees, there is no incentive to do that. They just collect the money and transfer it to the bondholder less their servicing fee. If anything, sending someone into foreclosure will probably make them stop making payments, and the servicer has to pay the bondholder the principal and interest payment even if the borrower doesn’t pay it. This is how many servicers got wrapped around the axle in the beginning of the crisis – homeowners stopped paying and they lost their advances lines from the banks, couldn’t pay the bondholders and ended up defaulting and going under.

The part where they discuss Nationstar selling whole loans makes no sense. No servicing contract gives the servicer the right to do that. (And I have read a few and negotiated a subservicing contract, so I am reasonably familiar with them). The servicer has the right to dispose of the underlying property, as long as they fulfill their fiduciary duty to the investor, but they can’t just sell loans or servicing rights.

Don’t forget that a big reason why banks are selling MSRs is because the government doesn’t want them to own them. Basel III includes a very punitive hit (they have to reserve 110% against them).

LikeLike

Yes it does. See tranches

Tranches subdivide pools, not loans. All they say is that the most senior tranches get paid first and the most junior tranches take losses first.

And MERS does for the mortgage market what a trust bank does for bond issues….Just keep record of who has a claim on what..

LikeLike

Heh.

@charlescwcooke: As we all know, anarchists are notorious for asking permission and observing parliamentary procedure to the letter.

LikeLike

Nomination for a future quote of the day:

“NoVAHockey

1:16 PM EST

ruk — the only thing that would make me richer than the ACA would be single payer.

grafting Medicare onto the entire system. sweet jesus, it would be like putting an gold spitting oil well in my backyard. “

LikeLike

Warning, counter-narrative.

Democrats have never been shy about using to oppose laws they don’t like on principle. Harry Reid, Hillary Clinton, John Kerry, and Barack Obama have all cast votes to cut off funding for things they dislike even in the face of opposition from the majority. Did Reid, Obama, Clinton, and Kerry vote against Iraq War funding because they didn’t want to give the troops what they needed? Did they do it because they believed such a vote would alter the course of U.S. foreign policy? Of course not. They did it for the sake of optics, the same optics that are driving Cruz and Boehner today, an attempt to leverage public opinion in their favor and highlight a disagreement where they believed the people were on their side.

http://thefederalist.com/2013/09/25/ted-cruzs-lost-cause-worth-fighting-for/

I’m pretty sure that was different.

LikeLike

“But they should have no impact at all on the disposition of the underlying loans, ”

“should” doesn’t seem to be born out by actual events, at least given the explanations that the various servicers have offered to date for why they haven’t done more modifications.

I think it makes for a more straightforward system when the same decision makers who hold the note and can say yes or no to a modification are also the same ones who will have to deal with an actual foreclosure and subsequent sale.

My thinking is informed by this piece:

http://www.ritholtz.com/blog/2010/10/why-foreclosure-fraud-is-so-dangerous-to-property-rights/

If it’s not criminal fraud, then it’s a systemic failure.

LikeLike

jnc:

I missed this from earlier:

“should” doesn’t seem to be born out by actual events, at least given the explanations that the various servicers have offered to date for why they haven’t done more modifications.

I read the piece you linked to and I couldn’t find any mention of CDS or any other derivative contracts. Again, I cannot think of any imaginable reasons why the existence of a derivative contract, a synthetic CDO, in which a particular mortgage was a referenced credit, would have any impact whatsoever on the disposition of a non-performing loan. The underlying loan is independent of, and has no dependency on, the derivative contract.

I think you must be misunderstanding the explanations if it seems like they are blaming derivative contracts for the inability to modify the loan. In all seriousness, the derivative contracts have absolutely nothing to do with the process.

LikeLike

“ScottC, on September 25, 2013 at 12:04 pm said:

jnc:

I’ve been trying to find out more about the history of AT&T’s monopoly. This site doesn’t really give any details, but does describe AT&T thus:

AT&T was a government-supported monopoly – a public utility – that would have to be considered a coercive monopoly.”

Do you have an example in mind of a monopoly that’s the natural result of the free market that wouldn’t be considered a coercive monopoly?

If not, then the practical effect of our disagreement over natural vs coercive monopolies would seem to be moot.

LikeLike

jnc:

Do you have an example in mind of a monopoly that’s the natural result of the free market that wouldn’t be considered a coercive monopoly?

In my reading of the history of AT&T, it seems that it was developing into free-market created monopoly until the feds threatened it with anti-trust action, at which point it negotiated with the government, making certain concessions (including agreeing to government setting of rates) in exchange for government protection of its monopoly, ie in exchange for becoming a coercive monopoly.

To whatever extent Microsoft is or has been a monopoly, that too is a non-coercive monopoly.

When I speak of a coercive monopoly, I mean one that is protected from competition by laws, not one that has achieved dominance through the market.

LikeLike

“Don’t forget that a big reason why banks are selling MSRs is because the government doesn’t want them to own them. Basel III includes a very punitive hit (they have to reserve 110% against them).”

I don’t dispute that at all. Like I wrote originally, it’s an unintended (or intended consequence) of the mortgage settlement and apparently Basel III too.

My point is that if Nationstar’s behavior is as alleged, it’s a problem. I suspect it’s illegal, but even if there’s some contract clause that allows a servicer to invalidate an existing modification upon transfer of the servicing rights it’s still a policy problem.

LikeLike

Here’s the trade and non-partisian press accounts of the same events

http://abclocal.go.com/kabc/story?section=news/local/los_angeles&id=9246636

Honoring a previous loan modification agreed to by the servicer at the time shouldn’t be optional. Either the contract was legally changed or it wasn’t. If these modifications aren’t legally binding on future servicers, this is another disaster waiting to happen.

LikeLike

Google?

LikeLike

That’s probably a good example.

LikeLike

jnc:

That’s probably a good example.

Google or Microsoft? Or both?

LikeLike

Maybe IBM at one time.

LikeLike

JNC – i think what people truly don’t understand is just how political everything about Medicare is. not some of it. all of it.

and the idea that in this country, the USA, we’ll have a “top men” run health care system that is isolated from political influence, is just crazy.

LikeLike

Yeah, it’s not like Medicare users are the most likely to vote either. Sure, they’d LOVE the IPAB!

LikeLike

FYI…Decisive America’s Cup race starts in 5 mins. US had been down 8-1 in the first-to-nine competition, but has unbelievably won a record-shattering 7 straight races to tie it up. All will be decided within the next 30 mins.

Live race blog here.

(In fact the US has already won 10 races, but since they started the final series with a 2-race penalty, they need to win 11 in order to take the Cup.)

LikeLike

US completes the comeback…takes the final race.

LikeLike

Google.

LikeLike

i think “single payer” for most people means a system that pays bills when you get sick that is free from influence from patients, providers, insurers, suppliers, employers. it’s doctors providing individualized care whenever you need it.

but, nobody is interested in actually reforming the system, so the only sane thing to do is profit of the mess. i didn’t wreck it. someobody else did

LikeLike

i think “single payer” for most people means a system that pays bills when you get sick that is free from influence from patients, providers, insurers, suppliers, employers. it’s doctors providing individualized care whenever you need it.

I just don’t understand how a rational person can believe that.

LikeLike

“I think you must be misunderstanding the explanations if it seems like they are blaming derivative contracts for the inability to modify the loan.”

No, they are blaming securitization. The derivative contract is for the related issue of slicing the loans into tranches.

LikeLike

I was probably off base in conflating the two issues.

LikeLike

jnc:

I was probably off base in conflating the two issues.

As I said earlier, I think your point that securitization might make it more difficult to modify a given loan makes sense because the party with the power to make the decision is not the actual owner, and so may have other interests beyond the straight economics of the modification. But I don’t see how that has aything at all to do with the tranching of default risk among the owners of the security.

LikeLike

The WSJ spots the real story on the CR breaking the sequester caps.

If Democrats pull this off, it will be a total and complete victory over the Republicans.

http://online.wsj.com/article/SB10001424052702304526204579097442586704618.html?mod=WSJ_Opinion_LEADTop

LikeLike

Heh.

Anyway, two reasons to post something this stupid. One: It’s a minor illustration of the obnoxiousness of what Sonny Bunch at the Free Beacon calls “the politicized life.” Dreier, a man of the left himself, is obviously irritated to see right-wing gargoyle Cruz doing something that every parent in America, liberal or conservative, has done at one point or another. You’d think a Dr. Seuss fan would be pleased to see him given a plum spot on a stage like this, especially since Cruz didn’t try to appropriate Seuss’s message for his own cause. (That fell to Democrats like Chuck Schumer, as you’ll see below.) But no, Cruz is the devil and therefore him reading Seuss to his kids on TV can’t pass uncommented-upon. And two: It gives me an excuse to link the single most charming element of last night’s marathon speech. If you didn’t catch this photo on Twitter when it was posted, make amends now. Adorable.

From HotAir.

http://hotair.com/archives/2013/09/25/bad-news-from-politico-dr-seuss-would-have-hated-ted-cruz/

LikeLike

people who are upset about cruz complete missed the point. and that they’re reduced to criticizing his choice of bed time story shows how hopeless out of touch they are.

LikeLike