Vital Statistics

| Last | Change | Percent | |

| S&P Futures | 1550.7 | -6.5 | -0.42% |

| Eurostoxx Index | 2597.6 | -43.6 | -1.65% |

| Oil (WTI) | 95.95 | -0.4 | -0.40% |

| LIBOR | 0.284 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 83.21 | 0.328 | 0.40% |

| 10 Year Govt Bond Yield | 1.86% | -0.05% | |

| RPX Composite Real Estate Index | 190.8 | -0.2 |

Markets are lower this morning as Euro sovereign yields widen on the Cyprus situation. Mortgage applications rose 7.7% last week. This is the last full trading day of the week (Thurs is a half day), so volume should start to dry up as traders square their books for quarter-end and leave for the long weekend. Bonds and MBS are up on the flight to safety trade.

We will have some Fed-speak today with Rosengren of Boston, Pianalto of Cleveland, and Kocherlakota speaking at various events during lunch. Hints about QE could move MBS, so watch your locks.

Consumer confidence fell in March to 57.9 from 61.4 a month earlier. The report blames Washington for the decrease. You certainly wouldn’t guess it from watching the stock market indices. It will be interesting to see how the spending numbers shake out.

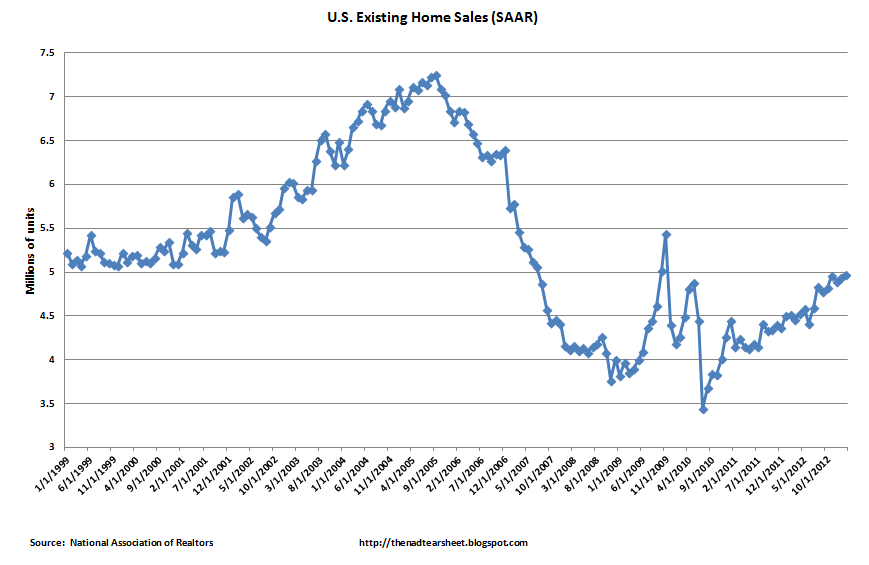

New Home sales fell 4.6% MOM in February, but were up 12.3 YOY to a seasonally adjusted annual rate of 411,000 units. The median sales price was $246,800, an increase of 3% YOY. There definitely seems to be a bifurcation of the market, where existing homes are rising at a high single digit rate, yet the new home market is experiencing more modest price increases. Investor activity is probably driving the difference, as professional investors are purchasing distressed property for rentals, while new home sales are driven by actual homeowners. Volume is picking up, with the sales in Feb up 13% from last summer.

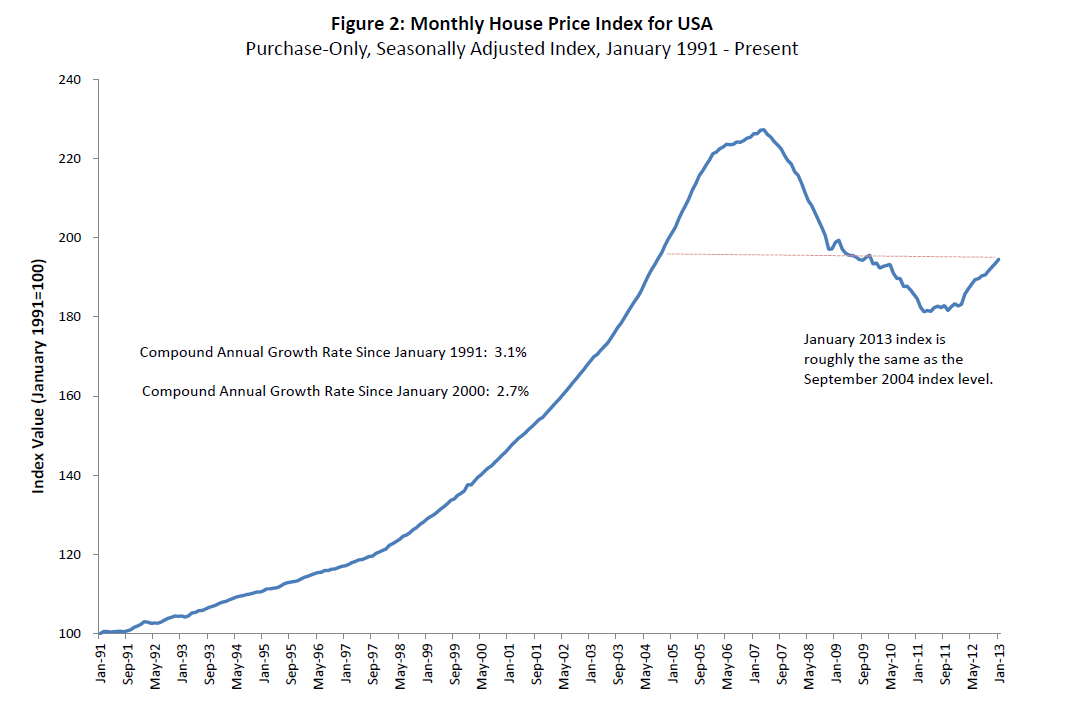

Bob Schiller pointed out that the latest housing data should be approached with caution. He points out that markets like Phoenix and Las Vegas are “frothy” and says that the recovery may even be a bubble. FWIW, I disagree that we are in another bubble – bubbles are psychological phenomenons that start with the view that “this time is different” and that the asset in question can only go up. That was the view of residential real estate in 2006. It isn’t now. Our grandkids may experience another real estate bubble, but we won’t. Schiller believes that it will take 40 years for home prices to rise to pre-2007 levels. Yes, that is an eye-opening forecast, but he is talking about inflation-adjusted numbers.

The government wants to impose a surcharge (through higher capital requirements) for the too big to fail banks. This will undoubtedly be another impetus for the big banks to break up voluntarily.

Filed under: Morning Report | 15 Comments »