Slap it and give it a name.

Filed under: Open Thread | 6 Comments »

Slap it and give it a name.

Filed under: Open Thread | 6 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1836.9 | 0.5 | 0.03% |

| Eurostoxx Index | 3099.5 | 26.6 | 0.87% |

| Oil (WTI) | 99.73 | 0.2 | 0.18% |

| LIBOR | 0.247 | 0.000 | -0.10% |

| US Dollar Index (DXY) | 79.97 | -0.514 | -0.64% |

| 10 Year Govt Bond Yield | 3.02% | 0.03% | |

| Current Coupon Ginnie Mae TBA | 103.7 | 0.0 | |

| Current Coupon Fannie Mae TBA | 102.7 | -0.1 | |

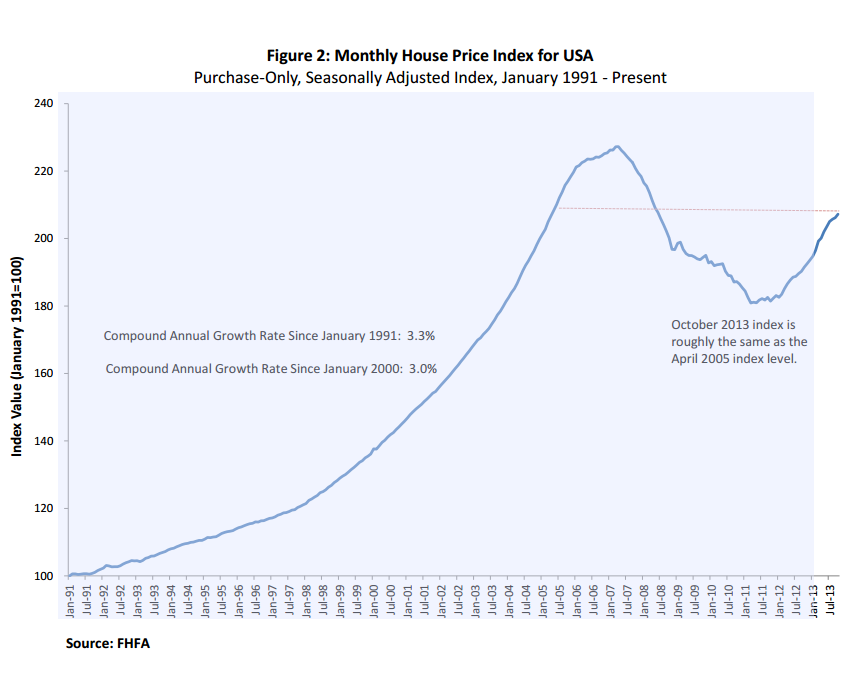

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.56 |

Filed under: Morning Report | 7 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1832.1 | 3.0 | 0.16% |

| Eurostoxx Index | 3072.9 | 2.0 | 0.06% |

| Oil (WTI) | 99.19 | 0.0 | -0.03% |

| LIBOR | 0.247 | 0.001 | 0.41% |

| US Dollar Index (DXY) | 80.48 | -0.076 | -0.09% |

| 10 Year Govt Bond Yield | 2.98% | 0.01% | |

| Current Coupon Ginnie Mae TBA | 103.7 | -0.4 | |

| Current Coupon Fannie Mae TBA | 102.8 | 0.0 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.51 |

Filed under: Morning Report | 8 Comments »

Merry Christmas, McWing. And everyone else, of course.

Filed under: Open Thread | 6 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1823.3 | 0.5 | 0.03% |

| Eurostoxx Index | 3072.9 | 2.0 | 0.06% |

| Oil (WTI) | 99.08 | 0.2 | 0.17% |

| LIBOR | 0.247 | 0.001 | 0.41% |

| US Dollar Index (DXY) | 80.52 | 0.069 | 0.09% |

| 10 Year Govt Bond Yield | 2.95% | 0.03% | |

| Current Coupon Ginnie Mae TBA | 103.9 | -0.3 | |

| Current Coupon Fannie Mae TBA | 103 | -0.3 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.49 |

Delinquencies ticked up 2.63% month-over-month according to LPS’s “First Look” mortgage report. Delinquencies + foreclosures are just under 4.5 million homes. Separately, FHFA announced that it has completed more than 3 million foreclosure prevention actions.

Finally, Merry Christmas everybody..

Filed under: Morning Report | 19 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1805.8 | 3.7 | 0.21% |

| Eurostoxx Index | 3037.7 | 6.7 | 0.22% |

| Oil (WTI) | 98.84 | -0.2 | -0.20% |

| LIBOR | 0.248 | 0.003 | 1.02% |

| US Dollar Index (DXY) | 80.73 | 0.103 | 0.13% |

| 10 Year Govt Bond Yield | 2.95% | 0.02% | |

| Current Coupon Ginnie Mae TBA | 104 | 0.3 | |

| Current Coupon Fannie Mae TBA | 102.8 | -0.1 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.52 |

Filed under: Morning Report | 8 Comments »

Wide open baby!

Filed under: Open Thread | 4 Comments »

It’s how I roll.

I added the “weekend” to the title. Deal with it h8rs!

Filed under: Open Thread | 24 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1805.8 | 3.7 | 0.21% |

| Eurostoxx Index | 3037.7 | 6.7 | 0.22% |

| Oil (WTI) | 98.84 | -0.2 | -0.20% |

| LIBOR | 0.248 | 0.003 | 1.02% |

| US Dollar Index (DXY) | 80.73 | 0.103 | 0.13% |

| 10 Year Govt Bond Yield | 2.95% | 0.02% | |

| Current Coupon Ginnie Mae TBA | 104 | 0.0 | |

| Current Coupon Fannie Mae TBA | 102.8 | -0.2 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.52 |

Filed under: Morning Report | 25 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1796.3 | -8.4 | -0.47% |

| Eurostoxx Index | 3015.9 | 40.8 | 1.37% |

| Oil (WTI) | 97.6 | -0.2 | -0.20% |

| LIBOR | 0.246 | 0.001 | 0.31% |

| US Dollar Index (DXY) | 80.65 | 0.542 | 0.68% |

| 10 Year Govt Bond Yield | 2.94% | 0.05% | |

| Current Coupon Ginnie Mae TBA | 104 | 0.0 | |

| Current Coupon Fannie Mae TBA | 102.7 | -0.4 | |

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.46 |

Stocks and bonds are lower this morning as the market digests the latest from the FOMC. MBS are off as well. Initial Jobless Claims rose to 379k. Later on this morning we will get existing home sales.

The Federal Reserve ended their Federal Open Market Committee meeting, and decided to taper. They will reduce purchases of Treasuries by $5 billion a month and purchases of mortgage-backed securities by $5 billion a month, which will mean the Fed will continue to build its balance sheet by $75 billion a month instead of by $85 billion a month. Tapering will begin in January. This was Ben Bernanke’s final FOMC meeting as Chairman before the torch is passed to the “dream team” of Janet Yellen and Stanley Fischer. Bernanke’s final press conference was no victory lap, but the press was respectful.

Bonds initially sold off on the news, with the 10 year trading above 2.92. Then bonds rallied, and the yield dropped to 2.82%, and then finally bonds sold off with the yield ending the day at 2.89%. Stocks loved the report, with the S&P 500 rallying 33 handles to close the day at a record high. Mortgage Backed Securities were off by almost half a point.

Steve Liesman of CNBC asked if this is now something we can expect every meeting, and it seems to be the case that they will reduce asset purchases by something like $10 billion every meeting from now. Bernanke mentioned all of the caveats about being data dependent, but it looks like this will be a constant until the Fed is no longer purchasing assets. The Fed will continue to reinvest maturing proceeds back into asset purchases. Ben Bernanke stressed that the Fed’s balance sheet is still growing, however it just isn’t growing as fast as it was. Bernanke was asked if that meant the Fed would likely still be conducting asset purchases in mid 2014 (as was previous guidance) and he said QE would probably end in late 2014.

The Fed changed the language regarding how long rates would remain close to zero. Previously, the Fed had guided an unemployment target of 6.5% as the level they would start raising interest rates. That language was changed to “The Committee now anticipates, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate well past the time that the unemployment rate declines below 6-1/2 percent, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal.” That language was what the stock market focused on, and probably accounts for the rally.

Finally, the Fed took down their projections for 2014 inflation and unemployment, and kept GDP the same.

Laugher of the converence – Ben Bernanke claiming that except for 2009, fiscal policy has been “extremely tight.” Reality check: Since obama took over, government spending has averaged around 24% of GDP, the highest since Truman. The biggest post WWII deficits as a percentage of GDP are (in order) 2009, 2010, 2011, 1946, 2012, 1983, 2013. Fiscal policy is about as tight as monetary policy right now. Calling the current fiscal environment “tight” makes about as much sense as calling a Triple Whopper Value Meal with satisfries and a diet coke “healthy.”

After Lennar’s good numbers, KB Home missed their quarter. Earnings and Revenues came in well below expectations. Cancellation rates were 36% and average selling prices increased 11%. The stock is down half a buck pre-open.

Ellie Mae’s Origination Insight Report is out for November. Refi percentage increased for the first time in a year, but that could be a seasonal phenomenon. FHA was 20% of all loans, while conventional was 69%. Days to close dropped to 42. Average FICO dropped to 729, average LTV was 81 and average DTI was 25/38.

I will be on Louis Amaya’s Capital Markets Today show at 10:00 am PST to discuss the FOMC meeting.

Filed under: Morning Report | 21 Comments »