Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1890.4 | 7.4 | 0.39% |

| Eurostoxx Index | 3220.6 | 13.9 | 0.43% |

| Oil (WTI) | 101.3 | 1.0 | 0.98% |

| LIBOR | 0.23 | -0.001 | -0.33% |

| US Dollar Index (DXY) | 80.34 | -0.131 | -0.16% |

| 10 Year Govt Bond Yield | 2.76% | -0.04% | |

| Current Coupon Ginnie Mae TBA | 105.2 | 0.4 | |

| Current Coupon Fannie Mae TBA | 104.1 | 0.4 | |

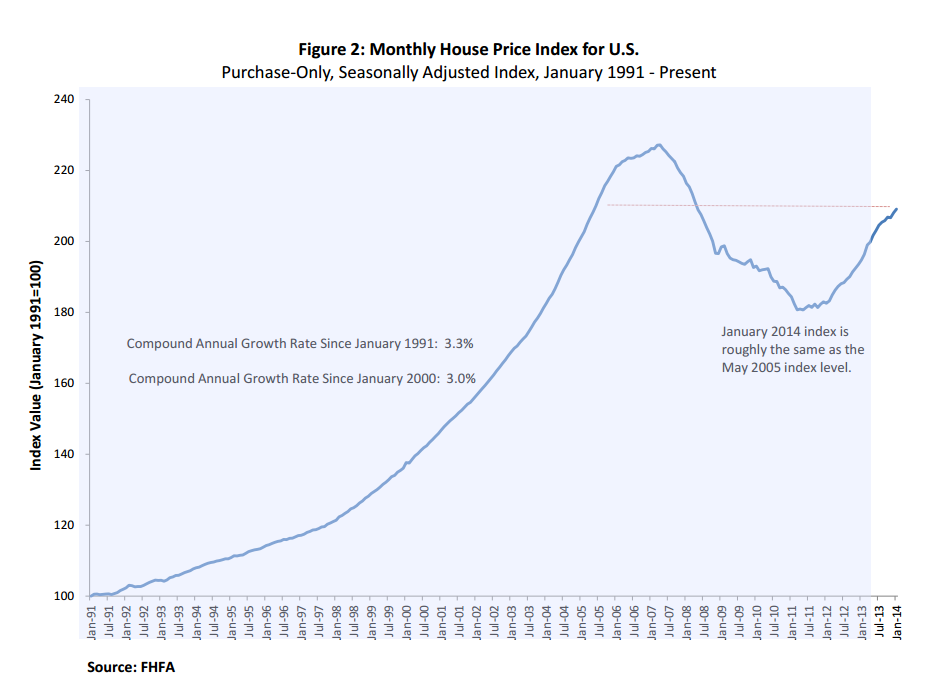

| RPX Composite Real Estate Index | 200.7 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.44 |

Stocks are higher after an okay jobs report. Bonds and MBS are rallying

Nonfarm payrolls rose 192k in March, slightly behind the 200k estimate. February was revised upward to 197k from 175k. The ADP Jobs report was spot on, for once with their estimate of 191k. The unemployment rate was unchd at 6.7% and the labor force participation rate rose to 63.2%. Average hourly earnings were flat, while average weekly hours increased to 34.5. So overall, it is an okay jobs report, nothing great, but nothing terrible either. Par for the course these days.

Separately, outplacement firm Challenger, Gray, and Christmas reported that announced job cuts fell 30% in March, making the first quarter the lowest in announced job cuts in 20 years. Announced job cuts are dropping, and the ISM reports show employment plans are increasing.

Smallish homebuilder Beazer Homes gave an update yesterday. Orders are down 9%, while backlog is down 2%. Orders on the West Coast dropped 16%. It appears prices simply moved to far too fast out there.

James Lockhart, former regulator for Fan and Fred says the stocks are worthless. At this point, they are litigation lottery tickets.

Filed under: Morning Report | 57 Comments »