Filed under: religion | 8 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1917.9 | -3.9 | -0.20% |

| Eurostoxx Index | 3240.1 | -7.7 | -0.24% |

| Oil (WTI) | 102.5 | 0.1 | 0.06% |

| LIBOR | 0.227 | 0.000 | 0.11% |

| US Dollar Index (DXY) | 80.49 | -0.150 | -0.19% |

| 10 Year Govt Bond Yield | 2.55% | 0.02% | |

| Current Coupon Ginnie Mae TBA | 106.5 | 0.1 | |

| Current Coupon Fannie Mae TBA | 105.5 | 0.1 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.18 |

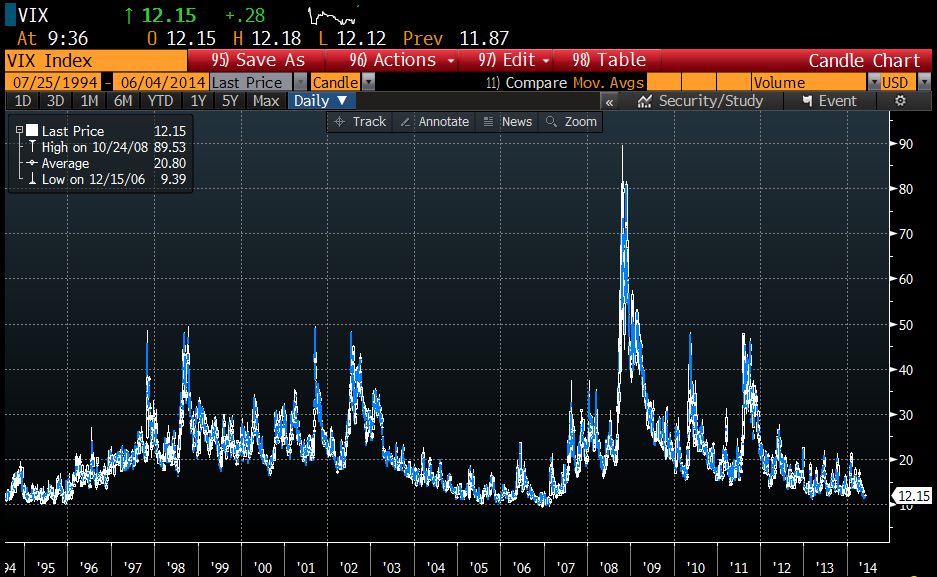

The calm before the storm? The Fed is worried about complacency in the markets. The VIX index has gone 74 straight weeks below its long-run average, which is a similar environment to 2006 – 2007. Junk spreads are widening, and junk issuance is growing as investors reach for yield. William Dudley commented: “Volatility in the markets is unusually low… I am a little bit nervous that people are taking too much comfort in this low-volatility period. As a consequence, they’ll take more risk that really what’s appropriate.” For what its worth, I think the VIX is useful for describing what has already happened in the market, not as a predictor of what is going to happen. Yes, there is the old market saw of “VIX is high, time to buy, VIX is low, time to go,” but a low VIX doesn’t necessarily mean markets are going to fall out of bed – look at the low VIX levels in 94-95, which preceded the mother of all stock market rallies. VIX invariably spikes AFTER the fit hits the shan, not before. It represents market players paying up for option protection, and that is a trailing indicator, not a leading one.

With respect to the junk issuance, investors (in particular defined benefit pension funds and insurance companies) are reaching for yield because the rate of inflation for their liabilities is largely insensitive to interest rates. The actuarial tables couldn’t care less if the Fed is driving down rates via QE – they need to earn X% on their fund to cover expected costs and that’s that. If they can’t get that in Treasuries, they’ll move to assets that can. Invariably that means they have to move out on the risk curve. We have seen this movie before, in the 1950s. FWIW, Dr. Cowbell thinks low rates are here to stay, and that “this time is different.” Most dangerous words in investing, ever. Anyway, it is nice to see the Fed muse about excessive risk taking, although IMO the biggest risk is probably in the so-called “risk free” long bond.

Filed under: Morning Report | 13 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1917.9 | -3.9 | -0.20% |

| Eurostoxx Index | 3240.1 | -7.7 | -0.24% |

| Oil (WTI) | 102.5 | 0.1 | 0.06% |

| LIBOR | 0.227 | 0.000 | 0.11% |

| US Dollar Index (DXY) | 80.49 | -0.150 | -0.19% |

| 10 Year Govt Bond Yield | 2.55% | 0.02% | |

| Current Coupon Ginnie Mae TBA | 106.5 | -0.1 | |

| Current Coupon Fannie Mae TBA | 105.5 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.18 |

Filed under: Morning Report | 74 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1922.6 | 1.1 | 0.06% |

| Eurostoxx Index | 3248.0 | 3.4 | 0.11% |

| Oil (WTI) | 102.4 | -0.3 | -0.27% |

| LIBOR | 0.227 | 0.000 | -0.11% |

| US Dollar Index (DXY) | 80.52 | 0.147 | 0.18% |

| 10 Year Govt Bond Yield | 2.50% | 0.03% | |

| Current Coupon Ginnie Mae TBA | 106.6 | -0.1 | |

| Current Coupon Fannie Mae TBA | 105.8 | -0.1 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.15 |

Filed under: Morning Report | Tagged: morning report | 46 Comments »

From KUT in Austin I heard the following.

The Texas Republican Party has denied the Log Cabin Republicans a space at next week’s state convention. Log Cabin Republicans represent gay conservatives and supporters of marriage equality in the party.

Log Cabin Republican Executive Director Gregory Angelo says the state party denied the group’s application for a booth at the convention because, as homosexuals, they disagree with a plank in the party platform. The plank reads, in part, that “homosexuality tears at the fabric of society.”

“It was our obligation to let the voters of Texas know and to let members of the Republican Party in Texas know that that language is in the party platform and it is being used to intentionally exclude gay Republicans from formal participation in the state GOP convention,” Angelo says.

—

A state party is not purely a private club. We learned that early in the civil rights struggles for black Texans. In Smith v. Allwright (1944), the Supreme Court ruled on a challenge to a 1923 Texas state law that had delegated authority to state conventions of political parties to make rules for their primaries. It ruled that the law violated the protections of the Constitution because the state allowed a discriminatory rule (no “negroes”) to be established by the Democratic Party. However, homosexuals are not being excluded here per se – in fact, the Log Cabin Rs who were elected delegates will be in attendance and will be voting. They will not be allowed a “booth”.

My own view of this bolded language in the Texas Republican platform is that it is wrong as a matter of fact and deeply prejudiced as a matter of practice. It is prejudiced as a matter of practice because no individual homosexual could be judged upon her own gifts and graces if her self-identification as a homosexual tears at the fabric of society.

The plank will not scare off any Rs in TX. Those who disagree with it will think it is a low priority and those who agree with it will strongly approve. There is a difference of enthusiasm here.

QB noted those of us who don’t think consenting private sexual conduct is a moral issue do so by reason of a libertarian slant. He made the case that while he did not believe there should be legal consequences for CPA sex, same sex marriage was not itself private conduct. This plank morally condemns private conduct and, I think, even status. While codifying this moral condemnation into law is not a requisite, I think it would be a natural result, because it happened historically.

Imagine yourself on the platform committee of the Texas Republican Party. Do you vote for or against this plank? Do you argue for or against it, and if you do, do you argue on moral or political grounds? Do you think it is an important plank or a throwaway?

Filed under: homosexuality, Open Thread, Republican Party, TEXAS | 243 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1911.2 | 2.1 | 0.11% |

| Eurostoxx Index | 3240.5 | -5.7 | -0.18% |

| Oil (WTI) | 102.9 | 0.2 | 0.19% |

| LIBOR | 0.227 | 0.000 | -0.11% |

| US Dollar Index (DXY) | 80.45 | -0.121 | -0.15% |

| 10 Year Govt Bond Yield | 2.44% | 0.00% | |

| Current Coupon Ginnie Mae TBA | 106.8 | 0.0 | |

| Current Coupon Fannie Mae TBA | 106 | 0.1 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.13 |

Filed under: Morning Report | 29 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1911.2 | 2.1 | 0.11% |

| Eurostoxx Index | 3240.5 | -5.7 | -0.18% |

| Oil (WTI) | 102.9 | 0.2 | 0.19% |

| LIBOR | 0.227 | 0.000 | -0.11% |

| US Dollar Index (DXY) | 80.45 | -0.121 | -0.15% |

| 10 Year Govt Bond Yield | 2.44% | 0.00% | |

| Current Coupon Ginnie Mae TBA | 106.8 | -0.1 | |

| Current Coupon Fannie Mae TBA | 106 | 0.0 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.13 |

There were 48,000 completed foreclosures in March 2014, up 5.9% month-over-month but down 10% year-over-year, according to CoreLogic. Approximately 720,000 homes in the U.S. are in some state of foreclosure, compared to 1.1 million a year ago. The foreclosure inventory is largely concentrated in the judicial states of Florida, New York and New Jersey. Over the past year, the number of seriously delinquent homes fell from 2.33 million to 1.86 million.

Filed under: Morning Report | 7 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1908.5 | -0.7 | -0.04% |

| Eurostoxx Index | 3241.4 | -2.9 | -0.09% |

| Oil (WTI) | 103.9 | -0.3 | -0.25% |

| LIBOR | 0.228 | -0.002 | -0.98% |

| US Dollar Index (DXY) | 80.49 | 0.139 | 0.17% |

| 10 Year Govt Bond Yield | 2.47% | -0.05% | |

| Current Coupon Ginnie Mae TBA | 106.8 | 0.2 | |

| Current Coupon Fannie Mae TBA | 105.9 | 0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.18 |

Filed under: Morning Report | 7 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1904.4 | 7.5 | 0.40% |

| Eurostoxx Index | 3241.0 | 0.6 | 0.02% |

| Oil (WTI) | 104.3 | 0.0 | -0.04% |

| LIBOR | 0.23 | 0.001 | 0.22% |

| US Dollar Index (DXY) | 80.33 | -0.065 | -0.08% |

| 10 Year Govt Bond Yield | 2.54% | 0.01% | |

| Current Coupon Ginnie Mae TBA | 106.4 | 0.0 | |

| Current Coupon Fannie Mae TBA | 105.5 | 0.0 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.16 |

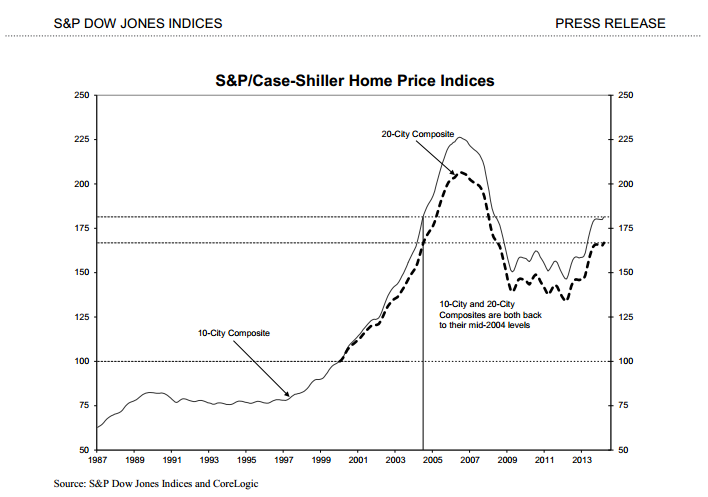

So, according to FHFA, we are within 6% of the peak and prices are at mid 2005 levels and according to Case-Shiller, we are within 20% of the peak and prices are at mid 2004 levels. Who is right? The answer is both. Case-Shiller is a broad-based index, while FHFA is narrower. The FHFA index only looks at homes with a conforming mortgage, which means it excludes jumbos and cash sales, which have been historically distressed properties, although that is changing.

Mohammed El-Arian weighs in on what is going on in the bond market. Speculators are net short Treasuries in a big way, and pension funds are redeploying stock market gains into the bond market. That makes for a tight market. You could almost feel the stops getting triggered a couple of weeks ago when we broke out of our 2.6% – 2.8% trading range:

Always-thoughtful Gary Shilling talks about how a financial crisis in China could be the catalyst for a massive “risk-off” trade, which would mean the rally in bonds could last longer than people think. Note that mortgage REITs (one of the biggest investors in mortgage backed securities) are leaning that way.

Filed under: Morning Report | 42 Comments »

Hi all,

My better half recently celebrated her 13th 29th birthday. As per usual, I make a dinner in her honor and we have a friend or two over. This night, it was just the fabulous Ms. Cox. The request was for something on the lighter side, including a chilled soup. So, I went with the idea of soup, salad, a light entree and dessert. I was supposed to make a fabulous caramel corn from Bluestem (our favorite KC restaurant), but ran out of gas. I abbreviated it by making spiced nuts and serving them with a wedge of blue cheese (Rogue is fantastic for those who haven’t tried their cheeses).

Soup was easy. I planned on asparagus, but didn’t see anything I liked, so shifted to a cucumber, mint and yogurt version (Epicurious has the link). The main was easy too. Scallops have become a favorite of ours. Just get some hot oil (clarified butter is amazing), sear them, and add to a base. I planned on a mango sauce as we had a couple that were sitting around. Too long as it happens as they’d gone rotten under the skins. A roasted tomato sauce subbed nicely.

The salad is my reason for writing this post. Etto is an Italian restaurant in DC with a starter they call Celery, Celery, Celery and Walnut. The Post recently, umm, posted their recipe. This is one that takes you to $100 per person dining at a $5 per plate cost. The ingredient list is deceptively simple: celery, Chinese celery, walnuts, cheese and dressing. The Chinese variant is typically cooked, but has a great flavor. It takes a surprising amount of time to prepare, mainly as peeling celery takes awhile. It kept clogging my Oxo peeler, but was worth the wait.

Ingredients

6 – 8 celery ribs, outer side peeled and thinly sliced (about 1 cup)

1 cup chopped celery leaves from inside of the bunch (use the rest to make stock)

1 cup chopped Chinese celery

1 ½ cups chopped Chinese celery leaves

½ cup toasted and chopped walnuts

1/3 cup olive oil (use the good stuff)

1 tablespoon fresh lemon juice

1 tablespoon fresh orange juice

½ tsp. salt

½ tsp. black pepper

2 oz. pecorino Romano cheese, shaved into curls

Method

Toss it all together and have fun. I tossed the celery and leaves, whisked together the olive oiive oil, juices, salt and pepper and tossed that all together, put onto plates and topped with cheese. It can’t hurt to reserve a few of the leaves as a garnish.

Filed under: Bites and Pieces | 5 Comments »