Markets are higher this morning as oil picks up a bid. Bonds and MBS are flattish.

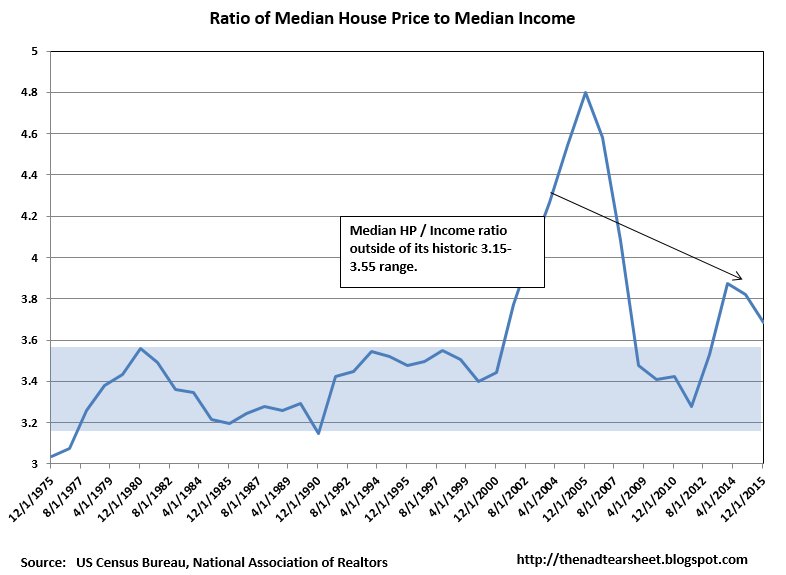

The FHFA House Price Index rose .3% in January, lower than expectations. Prices are up 5.1% year-over-year and are now within 3.5% of their peak levels, which corresponds to December 2005 levels.

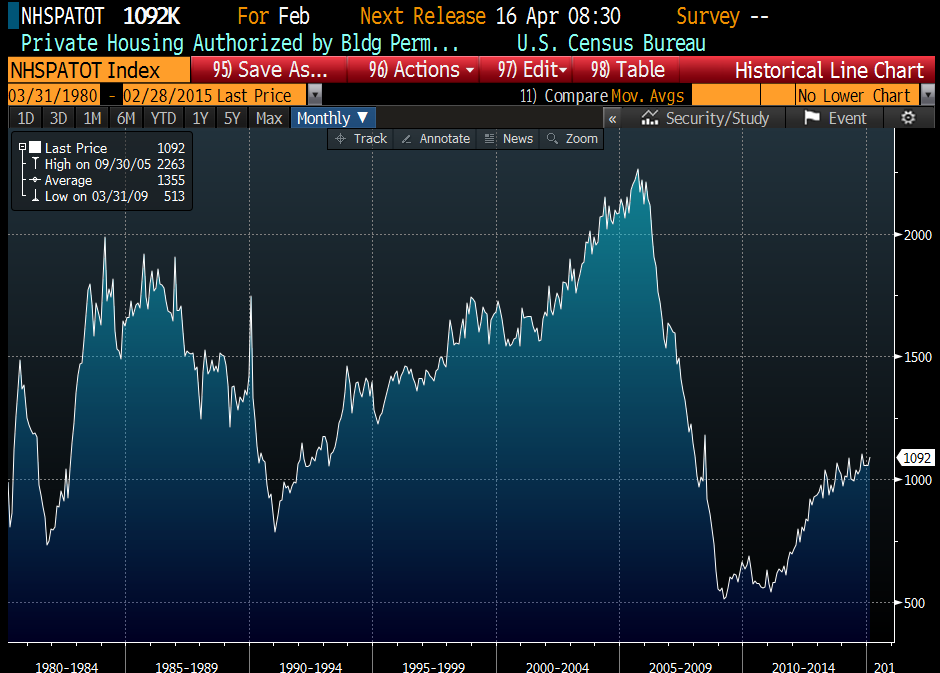

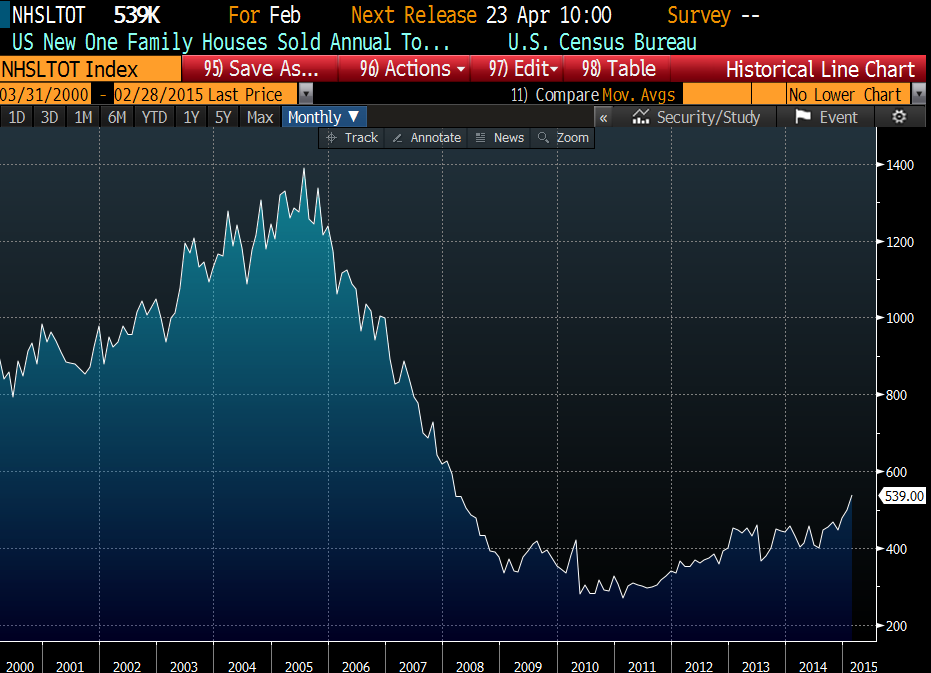

New Home Sales rose in February to a 539k pace from an upward-revised 500k pace in January. New Home Sales are hitting post bubble highs, but are still about 40% of previous peak levels, which were hit about 10 years ago.

On Lennar’s first quarter earnings conference call, CEO Stuart Miller had this to say about new home sales: “Pent-up demand is derived from a now multi-year production deficit that is continuing to grow even at current production levels (emphasis mine) At the same time, volume growth has been constrained by overly conservative lending standards, a regulatory environment that discourages mortgage lending and a negative consumer bias overhang against homeownership….While the relationship between pent-up demand, rental rates and mortgage availability continues to direct the housing market, it’s becoming more apparent that the mortgage market is loosening incrementally with time and enabling more demand to be realized as household formation begins to return to more normalized levels. We have believed and we continue to believe that the downside in the housing market is very limited and the upside is very significant (emphasis mine). We believe that the market is downside supported by the many years of production deficits that have yielded a limited supply of both rental and for-sale housing in the country. Any pullback in the housing market would be short-lived as there’s a need for shelter across the country and there’s very little inventory, and almost no likelihood of mortgage foreclosures (emphasis mine) given the stringent underwriting standards of the past years.

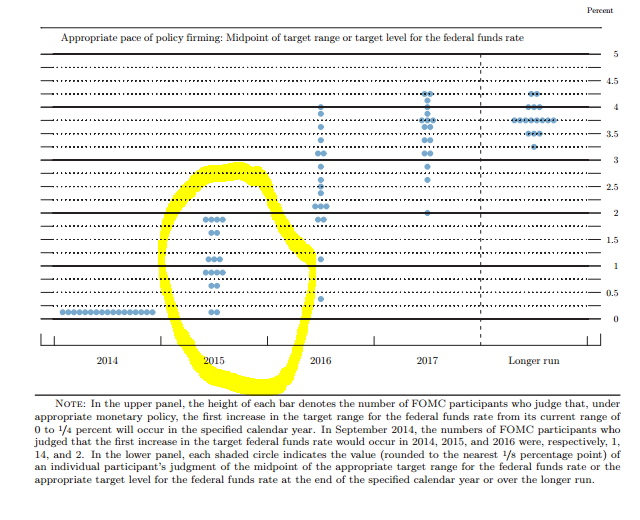

Inflation is still pretty much nowhere to be found, as the consumer price index rose .2% in February. On a year over year basis, it is flat, while ex-food and energy it is up 1.7%. Certainly if the Fed wants an excuse not to hike rates in June, the lack of inflation is giving them one. Note the Fed prefers to use PCE inflation, not CPI.

The Markit US Manufacturing PMI rose in March to 55.3 versus 55.1. Manufacturing continues to rebound, although it doesn’t employ as many people as it used to. Meanwhile one study shows that up to half of all jobs can be automated over the next 10 – 20 years.

The Richmond Fed Manufacturing Index fell to -8 from 0 last month.

Filed under: Morning Report | 6 Comments »