Stocks are lower this morning as the ECB raises aid to Greece. Bonds and MBS are flat.

The FOMC minutes really didn’t have much new information in it and bonds ignored the release for the most part. The decision to remove the word “patient” was not intended to signal that a raise is imminent, just that they will continue to be data-dependent. The strong dollar is beginning to have an effect on the economy, or at least the big multinationals. The stronger dollar is what drove them to revise their near-term GDP forecasts down.

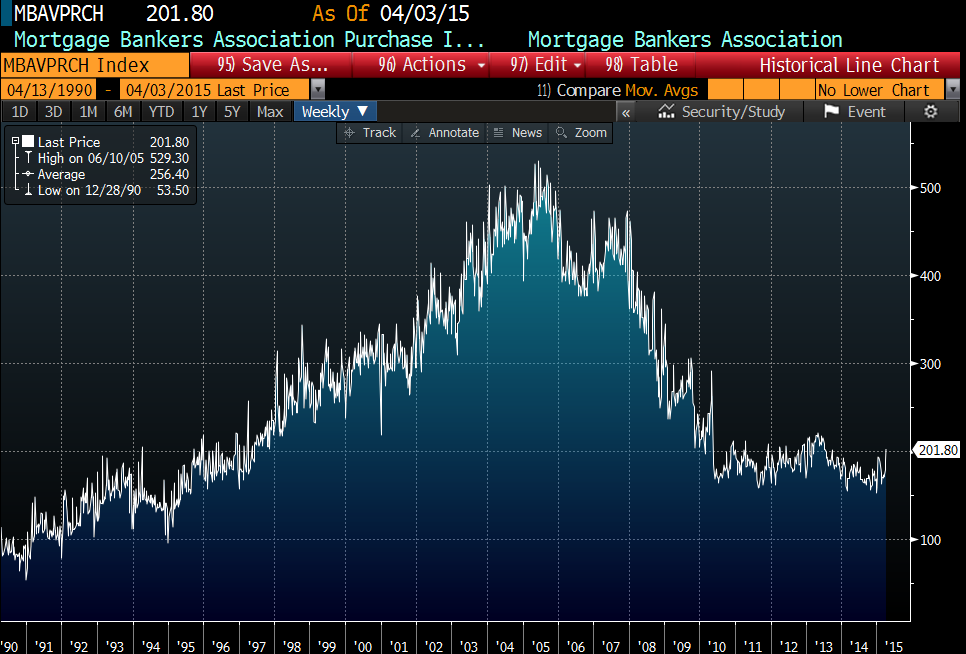

They didn’t discuss housing much except to say that the pace of activity was “slow” and noting the decrease in starts. FWIW, the homebuilders seem to be seeing a bit brighter picture. We’ll get a better idea when D.R. Horton and Pulte report in a couple of weeks. Regarding credit, they said that credit conditions were pretty much easy for everything but mortgages, where credit remains tight. For borrowers who can qualify, rates are low.

Alcoa kicked off earnings season last night with a miss on the top line as demand for aluminum is expected to grow at 6.5% in 2015 compared to 9% last year. They see a glut lasting through 2015. Interestingly, Alcoa continues to shutter production while China increases output. They already have tremendous overcapacity in steel, and are contending with a deflating real estate bubble.

Initial Jobless Claims came in at 281k, more or less in line with expectations. The Bloomberg Consumer Comfort Index rose to 47.9. Wholesale inventories rose while sales fell in February.

Consumers are getting a little more bullish on housing, according to the Fannie Mae National Housing Survey. They expect home prices to rise 2.7% over the next 12 months. Last February had a blip where more people thought the economy was on the right track than the wrong track, but it has reverted back to normalcy.

Filed under: Morning Report | 26 Comments »