Stocks are lower on overseas economic weakness. Bonds and MBS are flattish.

Initial Jobless Claims came in at 295, a little higher than expected. The Bloomberg Consumer Comfort index slipped to 45.4 from 46.6.

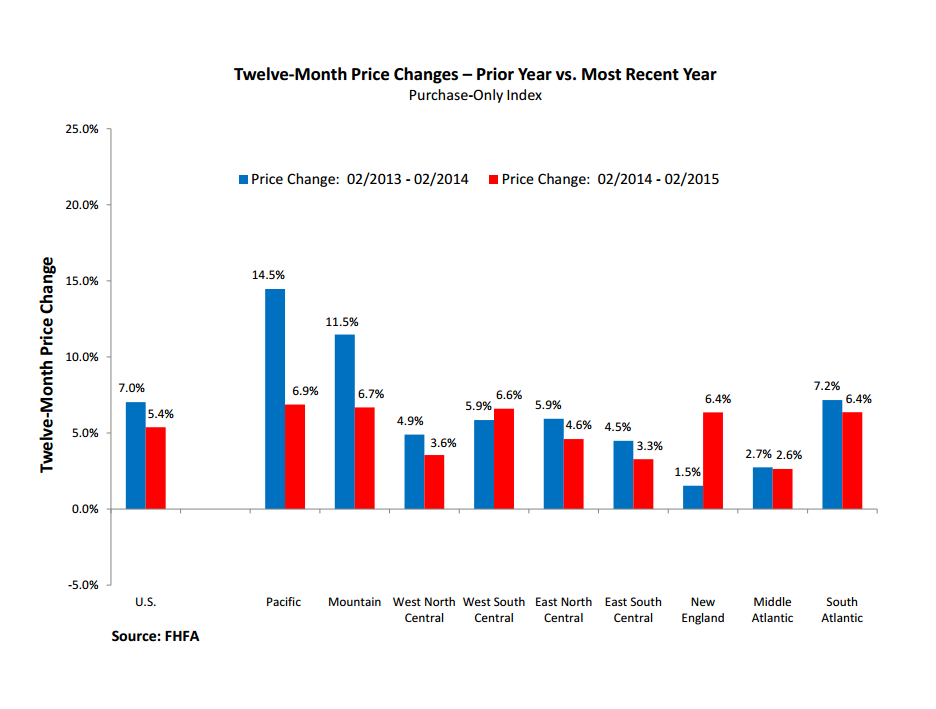

New Home Sales dropped to an annualized pace of 481k in March, from 543k in February. This was a big miss – the Street was at 515k.

We heard from homebuilder D.R. Horton yesterday. They beat expectations, but the margin and revenue guidance was on the light side, so the stock was sold off. D.R. Horton is very exposed to Texas and has yet to see any evidence of an slowdown in that economy. Horton was encouraged by the demand and is seeing strong growth in its Express brand, which is targeted at the first time homebuyer. The downside is that the margins in Express are lower.

Pulte reported this morning, and missed expectations. Revenues were light, however orders were up 6% and ASPs were up 2% to 323k. The company noted at strong start to the spring selling season, and characterized the housing recovery as “sustained but slow.”

Interesting stuff on the state of part-time workers. US part-time employment is reaching historical norms and that indicates the slack in the labor market is going away. Interestingly they polled workers who put in 30 hours a week or less. Of those people, a third were happy with their hours or wanted to work less. Only 23% wanted a traditional 40 hour a week job. Of those working more than 30 hours, about a quarter wanted to work less. Punch line: as the slack is taken up, wages are going to have to go up. Which means the Fed is more likely to mover sooner rather than later.

The Clinton Foundation is under the microscope right now, and the New York Times has a piece about how the State Department approved a Russian nuclear deal after a big donation to the Clinton Foundation. WaPo has a piece on the foundation and Bill Clinton’s speaking fees. There is supposedly a tell-all book coming out on the Clinton Foundation as well. Whatever comes out of it, the Democratic Party is all-in on Hillary and will dismiss any revelations as partisan poo-flinging regardless of the merits.

Filed under: Morning Report | 1 Comment »