Stocks are lower this morning as talks in Greece stall. They have a big payment due to the IMF tomorrow.

Some labor market numbers this morning. Initial Jobless Claims fell to 276,000, a great number. That said, the final revision to productivity for the first quarter is in, and it fell to -3.1%. Unit Labor Costs rose 6.7%.

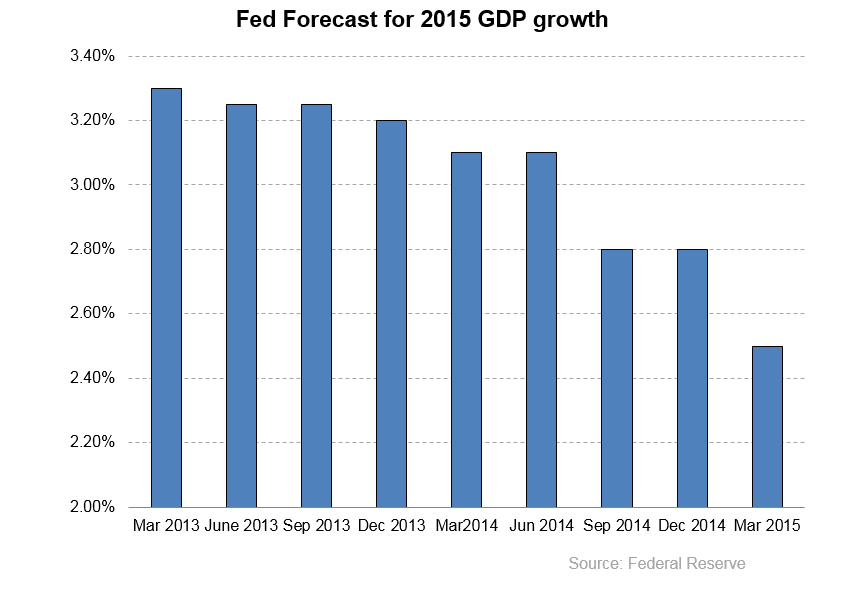

The IMF is urging the Fed to hold off raising rates until the first half of 2016. They also cut their forecast for US GDP growth from 3.1% to 2.5%, more or less matching what the Fed was forecasting at its March meeting. Given the weak Q1, that forecast is probably coming down in the June FOMC meeting.

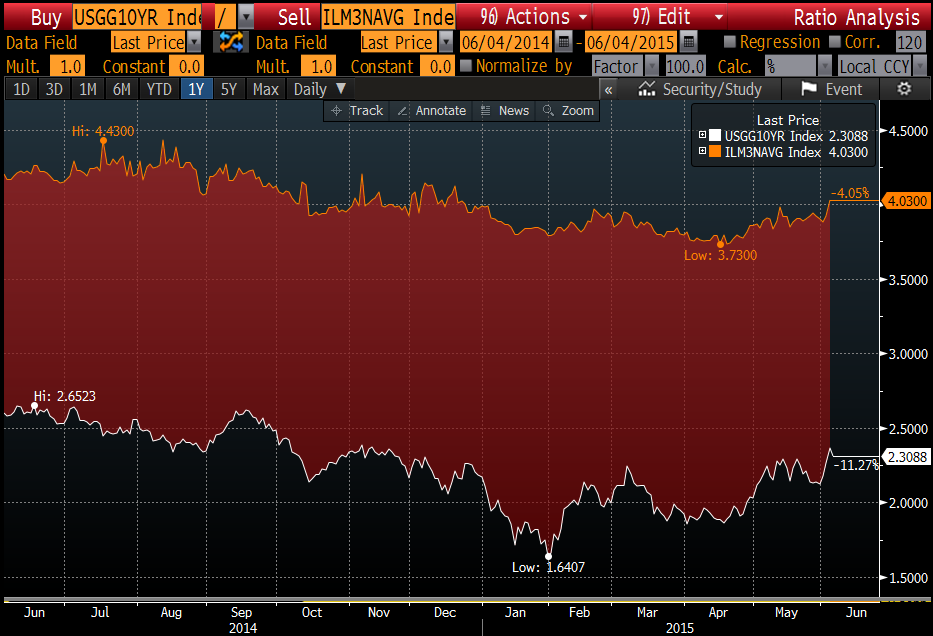

If you have been caught by surprise with the big moves in the bond market, you aren’t alone. The volatility in the bond market has been stunning over the past several months. The mood of the markets seems to go from fear of deflation in Europe to fears of inflation in the US. Jim Bianco characterized the bond market like this: “You want to shove rates down to zero, people are going to make big bets because they don’t think it can last,” Bianco said. “Every move becomes a massive short squeeze or an epic collapse — which is what we seem to be in the middle of right now.” IMO, the action in the markets is also a function of the fact that the major players in the markets right now are central banks, and they are taking positions based on social policy considerations, not economic ones. In other words, the ECB isn’t buying bonds because it thinks they are cheap – it is buying them in an attempt to create inflation. When you have non-economic players (players that are not concerned about their p/l) dominating the market, the ones that do care about their p/l (everyone else) are bound to get whipsawed.

Another issue is the fact that new regulations against proprietary trading has diminished the historical market stabilization role of trading desks. In the old days, when a big buyer or seller (say someone like a PIMCO) had an big order, they would find an investment bank to take the other side of the trade. The bank would bid (or offer) a little bit above or below the market and gradually work out of the trade over the course of the day or days. This had the effect of dampening volatility as it kept the market from getting whipsawed by big orders. Ironically, the regulatory push to “make banking boring again” has had the effect of making the government bond market anything but boring.

For mortgage bankers, the thing to keep in mind is that mortgage rates have been “fading” this volatility. In other words, they have been reluctant to follow big outsized moves. You can see it in the graph below, where the upper line is the Bankrate 30 year mortgage rate and the lower line is the US 10 year bond yield. Note how mortgage rates ignored the big dip in yields at the end of Janurary and have lagged the moves upward lately. Think about this when you are locking. If rates stop going up, mortgage rates will still probably keep rising to “catch up” with Treasuries. Even if rates fall, mortgage rates will probably stay up here for a while. In a volatile market like this it doesn’t make a lot of sense to be floating. Rates are still at historical lows, and can move up in a hurry. It would be shame to end up paying an extra 30 basis points on your mortgage because you were waiting to catch a rally that never came.

Filed under: Morning Report | 25 Comments »