Vital Statistics:

| Last | Change | |

| S&P Futures | 2256.8 | 1.5 |

| Eurostoxx Index | 359.6 | -0.4 |

| Oil (WTI) | 51.7 | -0.2 |

| US dollar index | 93.2 | 0.1 |

| 10 Year Govt Bond Yield | 2.55% | |

| Current Coupon Fannie Mae TBA | 103 | |

| Current Coupon Ginnie Mae TBA | 104 | |

| 30 Year Fixed Rate Mortgage | 4.29 |

Stocks are up this morning on no real news. Bonds and MBS are up as well.

Not much in the way of economic data this morning, however Janet Yellen speaks at 1:30pm EST.

The flash services PMI fell slightly to 43.5.

Today the Electoral College votes for President. The vote will then go to Congress to be certified in early January.

Homebuilder Lennar reported earnings this morning, with revenues up 15%, new orders up 12%, and backlog up 17%. Average selling prices rose only 2.9% to $357k, which indicates that home price appreciation is slowing. The press release didn’t address the cancellation rate, which will probably begin to grow for the builders as higher rates kick in. Lennar has a November 30 fiscal year, so it is probably a little early to see how higher rates are affecting them.

Lenders foresee a drop in margins and demand going forward as rates rise, according to the Fannie Mae Quarterly Lender Survey. Fully 2/3 of lenders view rates as “not favorable” at the moment. Lenders expect margin compression as well as refi shops cut prices to stay competitive. Lenders do expect to continue to ease lending standards. Lenders also intend to execute more through the GSEs and the government and plan to reduce the number of loans they hold on their balance sheet.

CoreLogic put out its forecasts for 2017. Home price appreciation will slow into 2017 as higher mortgage rates and home prices take a bite out of demand. Credit quality will remain good, however and we will start to see more HELOC activity, while refis will decrease. Vacancy rates will remain low, and rental inflation will be around 3%.

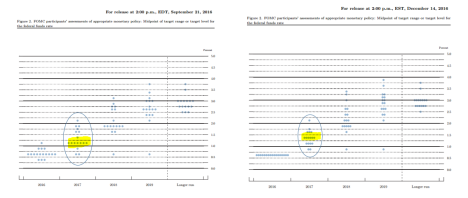

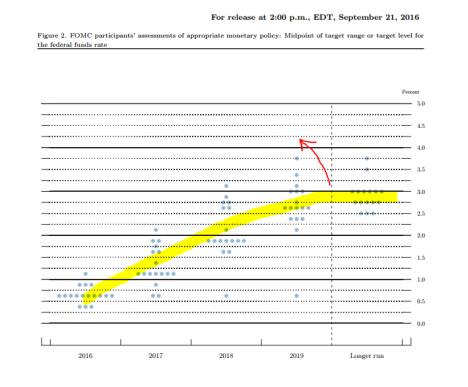

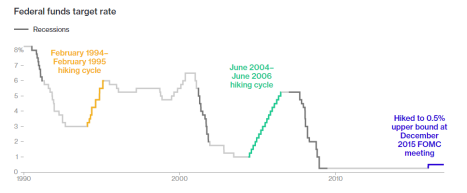

Here is a look at the effects of rising rates for the mortgage lending sector.

Filed under: Economy, Morning Report | 33 Comments »