Vital Statistics:

| Last | Change | |

| S&P futures | 2708 | 9.25 |

| Eurostoxx index | 360.56 | -1.71 |

| Oil (WTI) | 56.32 | 0.07 |

| 10 year government bond yield | 3.11% | |

| 30 year fixed rate mortgage | 4.94% |

Stocks are higher as oil stabilizes. Bonds and MBS are up. The 10 year is trading at 3.11%, quite the drop from the 3.27% levels of last week.

Inflation remains largely under control according to the Consumer Price index. The CPI in October rose 0.3% MOM and 2.5% YOY, right in line with street forecasts. Ex food and energy, it was up 0.2% MOM and 2.1% YOY.

A couple of trade groups wrote letters of support for Kathy Kraninger as head of the CFPB. The agency has been led by Mick Mulvaney, who also head OMB, as Acting Director. Kraninger is the supposed replacement. If she isn’t confirmed by the Senate in the lame duck session, the nomination returns to the President and Mick Mulvaney stays in charge for another 210 days. Kraninger promises to reform the CFPB in the same way Mick Mulvaney is, by ending “regulation by enforcement” and being more transparent about what the rules actually are.

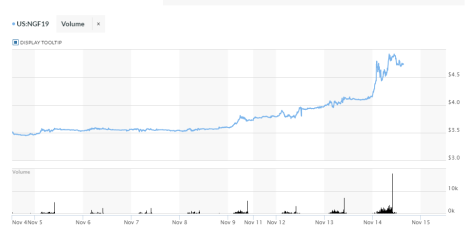

It usually pays to keep tabs on markets unrelated to your own. While people have been focusing on the oil market, and the bear market in oil, we are seeing the opposite effect in natural gas. Oil has lost about 24% over the past month. Natural gas gained more than that this week. Seriously. Natural gas closed last Friday at around $3.70 a contract and closed yesterday at around $4.70 a contract. Many commodities, especially natgas, is extremely sensitive to weather forecasts – if you go to the New York Stock Exchange, you’ll see CNBC on the trading floor. If you go to the a commodity exchange like the Chicago Mercantile Exchange, they have on the Weather Channel. So, if you get a forecast for an extra-cold winter, the price can skyrocket. As the link above explains, while we are the Saudi Arabia of natural gas, supply is not the driver here, storage is. And if we have an unusually cold winter, the amount of gas in storage can fall to dangerously low levels, which means higher prices. There are rumors going around of a hedge fund that is short Natgas and in trouble, but who knows? Regardless, it is something to watch.

Speaking of keeping tabs on other markets, watch the corporate bond markets. General Electric has issues. While everyone is aware of what is going on the stock price, the bonds are down about 15 points since early October. In bond market terms, for a household name like GE, that is a lot. Bonds trading in the low 80s aren’t necessarily distressed, but this is GE we’re talking about. If this snowballs, we should see a tightening of credit overall. It probably won’t affect the MBS market and mortgage pricing, but it will almost inevitably act as a drag on interest rates overall, and it could keep the Fed at bay.

Chart: Financial Stress Index:

Filed under: Economy, Morning Report | 45 Comments »