Stocks are lower this morning as the banks are getting hammered over a money laundering report. Bonds and MBS are up.

Bank stocks are getting slammed this morning after a report alleges that over $2 trillion in transactions were flagged as possible money laundering.

We don’t have much in the way of market-moving data this week, although we will get some housing numbers with existing home sales, new home sales, and the FHFA Home Price Index. Jerome Powell will be speaking Tuesday, Wednesday and Thursday this week.

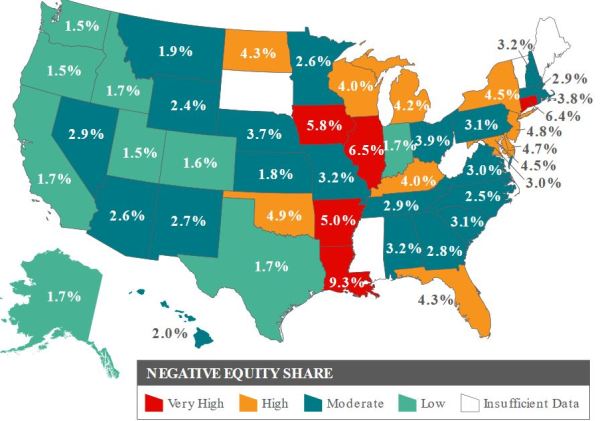

The average homeowner gained $9,800 in home equity in the second quarter according to CoreLogic. There are still about 1.7 million homes with negative equity. Negative Equity still remains a problem in a few states, but the home price appreciation of the past decade has largely solved the issue.

The housing market remains red hot according to Redfin. The median home price rose 13% YOY to $319k. Active listings fell 28% to an all-time low, while sales prices were 99.3% of listing prices, which is an 11 year high.

“Seasonality is going to become more noticeable now that schools have started and Labor Day is over,” said Redfin lead economist Taylor Marr. “There is still a lot of room for more homes for sale to hit the market to make up for lost ground during the pandemic. This increase in supply is likely to drive more strong year-over-year growth in home sales. Leading indicators of home sales like mortgage applications and pending sales are still showing tremendous strength as we head into fall.”

Stocks are higher this morning as we await the Fed announcement at 2:00 pm. Bonds and MBS are up

The Fed is expected to maintain rates at 0%, however the action will be in the projection materials. Most market-watchers expect the Fed to keep rates at this level until 2023. In June, the Fed was predicting unemployment would end 2020 at 9.3%, and we are already well below that. They were also predicting GDP would fall 6.5% this year. What would make stocks happy? Big upward revisions in the economic predictions, along with a commitment to hold rates at 0% through 2022.

Retail Sales came in a little below expectations, rising 0.6%. Ex-vehicles and gasoline, they rose 0.7%. The control group, which also excludes building materials fell 0.2%. Note that lumber is on a tear these days.

The retail sales numbers don’t bode well for the holiday shopping season, as back-to-school is often a good predictor. One other interesting data point: the banks have been reporting credit card delinquency rates are actually falling, which means people are paying down debt and not spending. I am guessing less entertainment spending is driving this, however it is something to keep an eye on.

Mortgage Applications fell 2.5% last week as purchases fell 1% and refis fell 4%. The week did contain an adjustment for the Labor Day holiday, so that could be introducing some noise into the numbers. “Mortgage rates held steady last week, and the 30-year fixed rate – at 3.07 percent – has now stayed near the 3 percent mark for the past two months,” said Joel Kan, MBA Associate Vice President of Economic and Industry Forecasting. “A 5 percent decline in conventional refinances pulled the overall index lower, but activity was still 30 percent higher than last year. With the flurry of refinance activity reported over the past several months, demand may be slowing as remaining borrowers in the market potentially wait for another sizeable drop in rates.”

Stocks are higher this morning on good overseas economic news. Bonds and MBS are flat

The FOMC meeting begins today. We will get the official policy announcement tomorrow afternoon. There is talk that the Fed will change its inflation targeting policy from managing a single point in time to an average over time. The practical effect will be for the Fed to let inflation build before raising rates.

August new home purchase applications rose 33% YOY, according to the MBA. “The housing market continued to exceed expectations in August, as housing demand for new homes stayed strong and the job market continued to recover,” said Joel Kan, MBA Associate Vice President of Economic and Industry Forecasting. “Despite economic uncertainty and the pandemic’s distortions to typical seasonal patterns, the comparisons to August 2019 show strength.”

The number of loans in forbearance fell by 15 basis points to 7.01% of mortgage servicers’ portfolio. Fannie and Freddie loans fell to 4.65%. Ginnie Mae loans fell to 9.12% and non-QM / portfolio rose to 10.71%. Part of the reason for the big drop in Ginnies / increase in portfolio loans was due to early buyout activity, where investors buy delinquent Ginnie loans out of the pool and portfolio them.

“The beginning of September brought another drop in the share of loans in forbearance, with declines in both GSE and Ginnie Mae forbearance shares,” said MBA Chief Economist Mike Fratantoni. “However, at least a portion of the decline in the Ginnie Mae share was due to servicers buying delinquent loans out of pools and placing them on their portfolios. As a result of this transfer, the share of portfolio loans in forbearance increased. Forbearance requests increased over the week, particularly for Ginnie Mae loans. With just under 1 million unemployment insurance claims still being filed every week, the lack of additional fiscal support for the unemployed could lead to even higher increases of those needing forbearance.”

In other economic data, the New York Empire State Survey improved last month, while industrial production rose 0.4% while manufacturing production rose 1%. Capacity Utilization rose to 71.4%.

Stocks are higher this morning as a bunch of mergers are announced. Bonds and MBS are flat.

The September FOMC meeting begins this week. No changes are expected in the Fed Funds rate. We will get a new set of economic projections and dot plot. That could potentially be market-moving.

There are 19 million high quality refinance candidates, representing 43% of all 30 year mortgages. Black Knight defines “high quality” as a FICO > 720, 20%+ equity, current on the mortgage, and could save 75 basis points on their mortgage. “With rates near historic lows, millions of consumers have an opportunity to find savings by refinancing and, in many cases, significantly lowering their interest rate and monthly payments,” said Will Pendleton, senior managing director of third party originations at Home Point Financial. “We feel that the low-rate environment is likely to persist well into 2021, and a great amount of focus in the lending community is on building capacity to meet the explosion of consumer demand.”

Note that 19 million mortgages at $250k a pop works out to be about $5 trillion in originations… So this has a few years to run.

Home prices are up 13%, according to Redfin. “Home price growth this high is making the housing market especially difficult for first-time homebuyers right now,” said Redfin chief economist Daryl Fairweather. “Rising prices are just one more reason for people to leave expensive urban neighborhoods behind. The sudden rise of remote work has allowed homebuyers who are priced out of one neighborhood to expand their search to more affordable areas. In turn, they are pushing up home prices in those relatively affordable areas, causing more people to look to even more affordable areas, and so on. Price growth may slow in 2021, but even if it does, high prices are going to continue to make affordability a concern for buyers.”

Stocks are flattish this morning on no real news. Bonds and MBS are down.

Initial Jobless Claims were flat last week at 884k. Separately, there were 6.2 million job openings in the US, according to the JOLTs report. This was a big improvement which is at least one bright spot in the labor economy.

Inflation remains well below the Fed’s target according to the producer price index. The headline PPI rose 0.3% MOM and fell 0.2% YOY. The core numbers were up 0.3% MOM and 0.3% YOY. The Fed is sweating bullets about the low inflation numbers as they fear the US slipping into a Japanese-style deflationary stagnation.

New listings are up 7%, according to Redfin. Pending home sales are up 21% YOY and the median price is up 12% to $318,473. 47% of homes had an offer within two weeks – the fastest pace since 2012. What is going on? People are ringing the register as home prices rise. The demand was always there – the persistent issue in the housing market has been limited supply. The sale=to-listing ratio is 99%, and bidding wars are becoming the norm.

Problems for landlords: The National Multifamily Housing Council reported that only 75% of renters had made their September rent payment so far. In August, that number was 79%.

“The initial rent payment figures from September have begun to demonstrate the increasing challenges apartment residents are facing. Falling rent payments mean that apartment owners and operators will increasingly have difficulty meeting their mortgages, paying their taxes and utilities and meeting payroll,” said Doug Bibby, NMHC President. “The enactment of a nationwide eviction moratorium last week did nothing to help renters or alleviate the financial distress they are facing. Instead, it only is a stopgap measure that puts the entire housing finance system at jeopardy and saddles apartment residents with untenable levels of debt. Federal policymakers would have been better advised to continue to provide support as they successfully did through the CARES Act.”

It is possible that the Labor Day weekend is introducing some noise into these numbers, but the trend is a worrisome sign.

Mortgage Credit Availability continues to move south as originators find little appetite for jumbo loans. I wonder if the surprise 50 basis point LLPA affected things as well.

“Mortgage credit supply fell to its lowest level since March 2014, driven by a reduction in supply from both conventional and government segments of the market,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “Additionally, both conforming and jumbo sub-indexes fell by almost 9 percent each, with the conforming index declining to the lowest reading since MBA’s series began in 2011. Credit continues to tighten because of uncertainty still looming around the health of the job market, even as other data on loan applications and home sales show a sharp rebound. A further reduction in loan programs with low credit scores, high LTVs, and reduced documentation requirements also continued to drive the overall decline in credit availability.”

Stocks are rebounding today after a tech sell-off. Bonds and MBS are flat.

Mortgage applications increased 3% last week as purchases and refis rose by the same amount. Purchase applications were up 40% year-over-year, however there was some noise due to the Labor Day holiday last year.

Black Knight Financial reported that $1.1 trillion worth of mortgages were originated in the second quarter

“Despite the nation being under pandemic-related lockdowns for much of the quarter, a record-breaking surge in mortgage originations occurred in Q2 2020, driven by the record-low interest rate environment,” said Graboske. “Nearly $1.1 trillion in first lien mortgages were originated in Q2 2020, which is the largest quarterly origination volume we’ve seen since first reporting on the metric in January 2000. Refinance lending grew more than 60% from the previous quarter and more than 200% from the same time last year, accounting for nearly 70% of all Q2 originations by dollar value. At the same time, purchase lending declined 8% year-over-year as the traditional spring homebuying season was impacted by COVID-19-related restrictions. However, mortgage loan rate lock data – a leading indicator of lending activity – suggests that the homebuying season was simply pushed forward into the third quarter.

More than half of Redfin offers faced bidding wars in August, according to the company. Competition was most pronounced in San Diego and San Francisco, as well as Phoenix, Austin and Salt Lake City.

“The market is on fire. There just isn’t enough on the market to supply the huge demand for homes,” said San Diego Redfin agent Lisa Padilla. “A lot of military buyers are trying to take advantage of the low interest rates for VA loans. Anything on sale for less than $600,000 has multiple offers, and sometimes they’re getting more than 20 offers. Only condos are a little slow, as most buyers want a home with a yard.”

Forbearance numbers fell to 7.16% from 7.2% last week, which was the lowest level in nearly 5 months. 4.8% of Fan and Fred loans were in forbearance while FHA loans in forbearance rose slightly to 9.62%.

Stocks are lower this morning as last week’s market sell-off continues. Bonds and MBS are up

Small business sentiment improved in August, according to the NFIB. The index rebounded back to its historic level. Hiring plans were definitely the bright spot in the report, as a net 21% of firms plan to hire in the next 6 months. Demand for skilled construction workers is high, but finding them is tough.

Intercontinental Exchange, the parent company of the New York Stock Exchange has completed its $11 billion purchase of Ellie Mae. ICE already owns MERS and Simplifile. “We are excited to begin the next important chapter in our journey to digitize the residential mortgage industry,” said Jeff Sprecher, founder, chairman and CEO of Intercontinental Exchange. “Ellie Mae’s industry leadership and best-of-breed technology will better enable us to further accelerate the automation of the mortgage origination workflow, which will benefit stakeholders across the production chain, including consumers.”

Productivity improved for the mortgage industry last quarter. The median productivity for sales employees (mainly LOs) was 7.4 loans per month, compared to 4.5 loans in the first quarter. Fulfillment employees were closing 8.4 loans a month versus 5.5 in the first quarter.

Urban apartment REITs are seeing big cuts in rent, as they try and “buy occupancy.” NYC rents are down 15%, while Bay Area rents are down 9%. The eviction moratorium (put out by the CDC) isn’t helping things. When the Center for Disease Control is making apartment regulations, you have to wonder if HUD is about to weigh in on vaccine efficacy. Note that campus housing REITs are struggling as well, as colleges move towards remote learning.

Overall, this is a strong report that pours cold water on the idea that we could be experiencing a W-shaped recovery (aka a double-dip recession). The labor force participation rate last year was 63.2%. It bottomed out just above 60% in April, which means we have retraced about half the COVID-related decrease.

I took a look at Quicken’s numbers and found some truly astounding things. First, their gain on sale margins are 519 basis points. I think the average according to the MBA is something like 429 bps. The more impressive number is the net profitability. Quicken made $3.5 billion on $72.3 billion in origination, or a whopping 484 basis points in net income. The MBA average for bankers was 167. Of course comparing Quicken to Pennymac or Mr. Cooper isn’t really the right model – those guys are largely aggregators while Quicken doesn’t really have much of a correspondent footprint (non-del only).

Another thing I found interesting from the conference call is that Quicken looks at its MSR book as a source of future business. In other words, they aren’t looking at the book solely as a return on assets game or even a hedge for the origination business – they are actively soliciting their borrowers for a refi. I wonder if people who are buying their spec pools are aware of this – prepay speeds are probably going to be quite higher than the rest of the industry.

Quicken is trying to build the infrastructure to get to $40 billion a month in origination and has a goal of achieving 25% market share by 2030. Finally, Quicken guided for $82 – $85 billion in origination in Q3, however margins are going to drop from 4.05% – 4.3%.

Finally, IMO the new WordPress editor is awful and klugey

Stocks are lower this morning on no real news. Bonds and MBS are up.

Rocket Mortgage (aka Quicken) reported second quarter numbers after the close yesterday. Origination volume rose 126% YOY to $72 billion. Margins were 519 basis points. For the third quarter, Quicken is projecting volume of $82 – $85 billion with a drop in gain on sale margins to 405 – 430 basis points. About 4.7% of the company’s servicing portfolio was in forbearance. Despite the strong numbers, the stock is down 10% pre-open.

Initial Jobless Claims fell to 881,000, which was below the 958k the street was looking for. Separately, companies announced 116k job cuts in August, according to outplacement firm Challenger, Gray and Christmas. “The leading sector for job cuts last month was Transportation, as airlines begin to make staffing decisions in the wake of decreased travel and uncertain federal intervention. An increasing number of companies that initially had temporary job cuts or furloughs are now making them permanent,” said Andrew Challenger, Senior Vice President of Challenger, Gray & Christmas, Inc.

Nonfarm productivity increased 10% in the second quarter, according to BLS. Unit labor costs increased 9%. Given the chaos in the labor market during Q2, I suspect there is a lot of noise in these numbers.

The Center for Disease Control has declared evictions a national health hazard. You would be forgiven for wondering what a bunch of MDs have to do with real estate, but here we are. Needless to say, the industry is dead set against it:

“If tenants are unable to pay their rent, then millions of our nation’s housing providers – many of whom are individual landlords and small business owners – will be unable to meet their mortgage obligations, make payroll to their own employees, maintain a safe and healthy living environment for their tenants and pay their state and local government property taxes,” said Bob Broeksmit, CEO of the Mortgage Bankers Association. “The result would be a cascading reaction that would only exacerbate the current economic crisis, leading to more job loss, financial pain, and long-lasting economic effects.”

and the left doesn’t think it is enough:

“The CDC order is really quite extraordinary, but if it’s not coupled with rental assistance, it’s just pushing the issue down the line and it will snowball into a crisis that landlords and tenants will be recovering from for decades,” said Emily Benfer, a law professor at Wake Forest University and co-creator of the COVID-19 Housing Policy Scorecard with the Eviction Lab at Princeton University.

“We need $100 billion to cover this deficit and that investment is far less expensive than the cost of eviction, the cost of homelessness — all of the downward effects that this causes,” Benfer said.

PIMCO is warning that releasing the GSEs without an explicit government guarantee will raise mortgage rates. The company is one of the biggest buyers of Fannie and Freddie mortgage backed securities, and the amount it is willing to pay to invest in MBS directly influences what borrowers pay. PIMCO is not interested in returning to the vague “government sponsored entity” status of Fan and Fred that existed pre-2008. It would view them as “wholly-owned private companies with no accompanying government guarantee.”

Stocks are higher this morning on no real news. Bonds and MBS are flat.

Mortgage Applications fell by 2% last week as purchases were flat and refis fell by 3%. “Both conventional and government refinancing activity decreased last week, despite 30-year fixed and 15-year fixed mortgage rates declining to near historical lows,” said Joel Kan, MBA Associate Vice President of Economic and Industry Forecasting. “Mortgage rates have remained below 3.5 percent for five months now, and it’s possible that refinance demand may be slowing and will not significantly increase again without another notable drop in rates.” Are we seeing prepayment burnout? Or was the 50 basis point adverse market fee adding some noise? I suspect it was the latter.

Independent mortgage banks made a profit of $4,548 on each loan in the second quarter, up from $1,600 in the first quarter. Average volume for the quarter was $1 billion. 96% of firms were profitable. Total production revenue increased to 429 basis points from 362 bp in the first quarter.

ADP reported 428,000 new jobs in August. The Street was looking for 900k. The consensus for Friday’s jobs report is 1.4 million.

Rental prices are collapsing in New York City and San Francisco. “Since [COVID-19] really started to affect the U.S. market in March, it has dramatically decreased the amount of people commuting to work every day—either because of social distancing measures or layoffs resulting from COVID-19’s effect on the economy. Given this, there is less of a reason for Americans to cluster in urban centers,” says Zumper analyst Neil Gerstein. “We believe this has caused a migration shift, and a subsequent demand shift, to historically cheaper cities.”