Vital Statistics:

| Last | Change | |

| S&P futures | 2992 | -2.25 |

| Oil (WTI) | 53.87 | -0.64 |

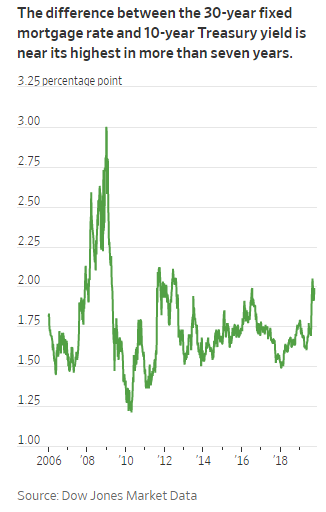

| 10 year government bond yield | 1.74% | |

| 30 year fixed rate mortgage | 4.03% |

Stocks are flattish as earnings come in. We should be hearing from heavyweights such as Tesla, Boeing, Caterpillar, Ford and Microsoft. Bonds and MBS are flat.

Mortgage Applications fell 12% last week as purchases fell 4% and refis fell 17%. Mortgage rates increased 10 basis points and increased to 4.02%. “Interest rates continue to be volatile, with Brexit votes and ongoing trade negotiations swinging rates higher or lower on any given day,” said MBA Chief Economist Mike Fratantoni. “Last week, mortgage rates jumped 10 basis points and were above 4 percent for the first time since September. The increase in mortgage rates caused refinance applications to drop 17 percent, and by more than 20 percent for conventional loans. Borrowers with larger loans are the most sensitive to rate changes, and with rates climbing higher last week, the average size of a refinance loan application fell to its lowest level this year.”

Existing home sales fell 2.2% in September, according to NAR. Lawrence Yun, NAR’s chief economist, said that despite historically low mortgage rates, sales have not commensurately increased, in part due to a low level of new housing options. “We must continue to beat the drum for more inventory,” said Yun, who has called for additional home construction for over a year. “Home prices are rising too rapidly because of the housing shortage, and this lack of inventory is preventing home sales growth potential.” The median home price increased 5.9% to 272,100 and the supply of available homes came in at 1.83 million units, or about 4 month’s worth of inventory.

Home prices rose 0.2% MOM and 4.6% YOY in August, according to the FHFA House Price Index. Home price appreciation is definitely decelerating this year, compared to 2018, although lower rates will probably re-accelerate growth in the markets with tighter inventory.

FHFA Director Mark Calabria said that he is willing to wipe out the shareholders of Fannie and Freddie if needed to protect taxpayers. “If the circumstances present themselves where we have to wipe out the shareholders, we will.,” he said at testimony in front of the House Financial Services Committee. He added that he believes that shareholders should have lost their stakes in the GSEs when the government rescued them in 2008. Fannie and Fred were put into conservatorship, with the government owning 79.9% of the companies. This was done largely to prevent disruption to the mortgage market if the companies were to enter formal bankruptcy, and also to prevent the government from having to consolidate all of Fannie’s debt on its own balance sheet. His comments at least leaves the door open for some recovery value for common stockholders if the GSEs are reformed. FWIW, the Obama administration was absolutely steadfast in their belief that the stock was worthless, and a change in administrations will probably return to that stance.

Filed under: Economy, Morning Report | 8 Comments »