I started writing for this site as well – http://marketrealist.com/

Free professional investment research for individual investors. Check it out.

Filed under: Economy, stock market | 15 Comments »

I started writing for this site as well – http://marketrealist.com/

Free professional investment research for individual investors. Check it out.

Filed under: Economy, stock market | 15 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1583.0 | 0.3 | 0.02% |

| Eurostoxx Index | 2664.1 | 2.5 | 0.09% |

| Oil (WTI) | 94.28 | -0.4 | -0.38% |

| LIBOR | 0.277 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 82.15 | -0.387 | -0.47% |

| 10 Year Govt Bond Yield | 1.79% | -0.02% | |

| Current Coupon Ginnie Mae TBA | 105.4 | 0.0 | |

| Current Coupon Fannie Mae TBA | 103.7 | 0.2 | |

| RPX Composite Real Estate Index | 190.8 | 0.5 | |

| BankRate 30 Year Fixed Rate Mortgage | 3.56 |

Markets are flattish this morning after initial jobless claims came in lower than expected at 346k. They dropped 42k from last week, which spiked due to a seasonal adjustment related to the Easter holiday. Import prices fell half a percent on lower energy costs.Bonds and MBS are up.

Ever since the Bank of Japan announced its quantitative easing program, the market has been speculating that Japanese investors would enter the US market en masse and purchase Treasuries. There has been plenty of anecdotal evidence, but no real numbers to work with. Yesterday’s 10 year auction didn’t provide any either – the bid to cover ratio was 1.8 which was a little light.

FHA might need a little more money from the government. They have $30 billion of cash on hand and insure $1.1 trillion in loans. The Administration is projecting they might need another billion. It looks like it was the reverse-mortgage business that hammered them.

One of the interesting things about the latest FOMC minutes is that the dispersion of opinion regarding the future of QE appears to be widening. Some wanted to end QE now, while others not only want to continue it, they want to increase it. Nonvoting hawk Charles Plosser said the Fed would be wise to begin unwinding its balance sheet now.

SIFMA lays into Obama’s proposed 2014 budget. It sounds like ETF investors could be in for a nasty surprise. They support the Administration’s proposal to create bonds for financing infrastructure spending, but pretty much pan everything else. The proposal is loaded with new taxes on capital Suffice it to say, if you are an investor, the administration is gunning for you.

Filed under: Morning Report | 59 Comments »

Vital Statistics:

|

Last |

Change |

Percent |

|

|

S&P Futures |

1567.7 |

4.5 |

0.29% |

|

Eurostoxx Index |

2630.1 |

35.0 |

1.35% |

|

Oil (WTI) |

93.64 |

-0.6 |

-0.59% |

|

LIBOR |

0.277 |

-0.001 |

-0.36% |

|

US Dollar Index (DXY) |

82.38 |

0.070 |

0.09% |

|

10 Year Govt Bond Yield |

1.77% |

0.02% |

|

|

Current Coupon Ginnie Mae TBA |

107.1 |

1.2 |

|

|

Current Coupon Fannie Mae TBA |

103.6 |

-0.1 |

|

|

RPX Composite Real Estate Index |

190.1 |

0.0 |

|

|

BankRate 30 Year Fixed Rate Mortgage |

3.57 |

Stock markets are higher this morning in anticipation of the Fed minutes which will be released this morning at 9:00 am (a change from their usual 2:00 pm time). Market participants will focus on hints regarding the end of quantitative easing. Mortgage Applications rose 4.5% last week on the back of the BOJ-led rally in the bond market and MBS. Treasury will also be conducting a 10-year auction around 1:00 pm. It will be interesting to see if the bid / cover ratio is affected by events in Japan. Bonds and MBS are down small.

Earnings season kicked of on Tuesday with Alcoa reporting better than expected earnings, but weaker sales. Retailers Fastenal and Family Dollar are down this morning after missing. We will get JP Morgan and Wells Friday morning before the open.

The President plans to release a $3.77 trillion budget today. He is proposing $1.8 trillion in new spending (although to be fair, that is to replace the sequester). He is also instituting a AMT II on incomes over $1 million of 30%. He also proposes to cap IRAs at $3 million, end carried interest, and to raise taxes on tobacco. He will also propose changes to the way cost-of-living adjustments are calculated – aka Chained CPI – to Social Security. Given that taxes and spending both increase pretty dramatically, the plan is DOA in the house.

It turned out the Fed mistakenly released the minutes early. Still don’t have the actual link, but here are some of the particulars: Economy re-accelerating after Q4 slowdown. Private nonfarm payroll increased at a modest rate in January, but expanded more briskly in Feb. (We now know that March was a disaster). The Fed asked primary dealers about their expectations for when the Fed will start tightening (are they running the Fed according to polls now?) and the view seems to be Q114 for the end of QE and Q315 for the first increase in the Fed Funds Rate. They noted that there did not seem to be much of a pullback in the economy in response to the tax hikes that kicked in Jan 1. Opinions about QE were all over the place, with some wanting to end it now and others wanting to increase the pace of purchases.

Filed under: Morning Report | 33 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1550.9 | 4.9 | 0.32% |

| Eurostoxx Index | 2600.8 | 15.6 | 0.60% |

| Oil (WTI) | 93.27 | 0.6 | 0.61% |

| LIBOR | 0.279 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 82.61 | 0.111 | 0.13% |

| 10 Year Govt Bond Yield | 1.72% | 0.01% | |

| Current Coupon Ginnie Mae TBA | 106 | 0.1 | |

| Current Coupon Fannie Mae TBA | 104.3 | 0.0 | |

| RPX Composite Real Estate Index | 190.1 | 0.4 | |

| BankRate 30 Year Fixed Rate Mortgage | 3.54 |

Markets are higher this morning on no real news. The Japanese Yen continues to fall, and is now approaching 100 yen to the dollar. The new program of quantitative easing in Japan is re-igniting the yen carry trade, except now the Japanese are borrowing yen to invest in US dollar assets. In case you missed it, Japan’s Nikkei 225 stock market index is up 52% since November. Incredible move. Japan’s QE program will mean incrementally lower rates on US long-dated Treasuries and MBS. Bonds and MBS are flat this morning.

Alcoa kicks off Q1 earnings season after the close today. We will get JP Morgan and Wells Fargo earnings on Thursday before the open.

Friday’s lousy jobs report probably means that any talk of ending QE this summer is probably over. After 3 consecutive economic slumps over the summer months, the Fed is going to stay aggressive. Chicago Fed President Charles Evans said “I’m going to have a lot more confidence if I begin to see indications that growth is well above trend and its going to be sustainable.” The Fed is going to be wary of reducing stimulus given that the fiscal policy has tightened a little bit.

Fannie Mae’s surprise profit has investors re-thinking the theory that they will be euthanized. Hedge funds are jumping into the preferred stock, which was issued in spring of 2008 as Fannie Mae was circling the drain before becoming nationalized. The 8.25% prefs have a $25 face value and were trading at $4.81 on Friday. All of this is predicated on the idea that Fannie Mae will be able to pay back the government. Once that happens, Fannie will restructure, and the bet is that there will be a place in the capital structure for the prefs. Risky bet, obviously, but big upside too.

Filed under: Morning Report | 121 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1537.5 | -17.0 | -1.09% |

| Eurostoxx Index | 2590.5 | -30.9 | -1.18% |

| Oil (WTI) | 92.26 | -1.0 | -1.07% |

| LIBOR | 0.279 | -0.001 | -0.36% |

| US Dollar Index (DXY) | 82.43 | -0.245 | -0.30% |

| 10 Year Govt Bond Yield | 1.70% | -0.06% | |

| Current Coupon Ginnie Mae TBA | 105.8 | 0.5 | |

| Current Coupon Fannie Mae TBA | 104.4 | 0.4 | |

| RPX Composite Real Estate Index | 189.7 | 0.3 | |

| BankRate 30 Year Fixed Rate Mortgage | 3.59 |

They’re beating the tape with the ugly stick after a dismal jobs report. The S&P 500 futures dropped from -4 to -16 on the report. The 10-year jumped on the news and is now yielding 1.7%. It is hard to believe the 10 year was above 2% three weeks ago. MBS are rallying as well, but not as much as the 10-year.

The March Employment Situation showed the economy added 88,000 jobs in March, well below the 190,000 estimate. February was revised upward to 268,000 from 236,000. The unemployment rate ticked down to 7.6% from 7.7%, but that was due to a drop in the labor force participation rate, which dropped .2% from 63.5% to 63.3%. This means that the size of the labor pool dropped as more workers simply stopped looking for a job. Long-term unemployed workers who are not actively looking for a job are not counted as part of the labor force. Wages were flat month-over-month and increased 2% year-over-year.

The recent rally in bonds pours cold water on the “great rotation” theory – the idea that 2013 would be the year when investors, particularly big institutional investors, change their target asset allocation and sell bonds to buy equities. So far, it seems like that investors are allocating money equally to both sectors – stock funds have taken in $79 billion while taxable bond funds have taken in $76 billion. Between the Bank of Japan’s QE program, which is driving funds to the US, the Fed’s QE program, and continued investor purchases of bonds, the expected 2013 bloodbath in the bond market may be held off for a while. Meanwhile, mortgage bankers are licking their chops thinking about another refi wave.

Chart: US Unemployment rate 1949-Present

Filed under: Morning Report | 53 Comments »

Vital Statistics:

|

Last |

Change |

Percent |

|

|

S&P Futures |

1550.7 |

2.2 |

0.14% |

|

Eurostoxx Index |

2661.8 |

22.8 |

0.86% |

|

Oil (WTI) |

93.96 |

-0.5 |

-0.52% |

|

LIBOR |

0.28 |

-0.001 |

-0.25% |

|

US Dollar Index (DXY) |

83.19 |

0.469 |

0.57% |

|

10 Year Govt Bond Yield |

1.77% |

-0.04% |

|

|

Current Coupon Ginnie Mae TBA |

104.9 |

0.1 |

|

|

Current Coupon Fannie Mae TBA |

103.7 |

0.2 |

|

|

RPX Composite Real Estate Index |

189.4 |

0.1 |

|

|

BankRate 30 Year Fixed Rate Mortgage |

3.68 |

Markets are giving back some Japan-led gains after Initial Jobless Claims spiked to 385k from 357k. This was the holiday-shortened Easter week, so there is a seasonality adjustment there. On a non-seasonally adjusted basis, they fell. Bonds and MBS are rallying, with the 10 year yield down to 1.77%.

The Bank of Japan outlined more aggressive monetary actions last night with their own version of quantitative easing. This pushed the Nikkei 225 stock market index up 2%, and caused a sizeable drop in the yen. This explains the rally in US bonds as Japanese investors flee for the “high yielding” US treasury market. Don’t laugh – the Japanese 40 year bond (the 2’s of 52) yields 1.34%. The US 10-year at 1.77%, in the context of a depreciating yen, is reviving the yen carry trade. The Yen Carry Trade is when Japanese investors borrow funds at yen rates and invest in high-yielding sovereign debt. They benefit from the pickup in yield and any favorable currency movements. With the high quality Euro sovereigns yielding even lower than the US, we are the only game in town. Punch line – this will put downward pressure on mortgage rates in the US, at least at the margin.

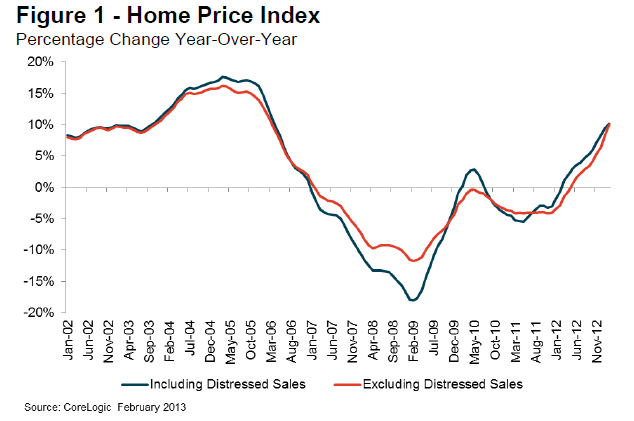

The CoreLogic Home Price Index increased 10.2% on a year-over-year basis in February, the highest increase since March of 2006. It is the 12th consecutive monthly increase. The gains were broad based, with 96% of their MSAs reporting gains. California, Arizona, and Nevada all showed gains in the high teens. They are forecasting a 2% month over month increase in March, or 12% year over year.

Chart: CoreLogic Home Price Index

Hank Paulson, George Bush’s Secretary of Treasury, says that Fannie Mae’s new profitability shouldn’t deter the government from establishing a new platform for mortgage finance. He mentioned the Washington Post article that says the Administration is pushing banks to make home loans to people with weaker credit. Nominated to take over as Treasury Secretary just as the housing bubble was peaking, he can be forgiven for being a little gun-shy on re-inflating the bubble.

San Francisco Fed President John Williams said he is hopeful that “the economy has shifted into high gear” and that the Fed could begin slowing the purchases of Treasuries and MBS this summer, with a full exit by the end of the year.

Finally, you can hear my latest interview on Capital Markets Today, where I discuss real estate pricing, politics, and the economy.

Filed under: Morning Report | 70 Comments »

Vital Statistics:

| S&P Futures | 1564.7 | 0.3 | 0.02% |

| Eurostoxx Index | 2665.2 | -14.6 | -0.54% |

| Oil (WTI) | 96.64 | -0.5 | -0.57% |

| LIBOR | 0.281 | -0.001 | -0.35% |

| US Dollar Index (DXY) | 82.81 | -0.117 | -0.14% |

| 10 Year Govt Bond Yield | 1.85% | -0.01% | |

| Current Coupon Ginnie Mae TBA | 104.6 | 0.0 | |

| Current Coupon Fannie Mae TBA | 103.3 | 0.0 | |

| RPX Composite Real Estate Index | 189.3 | -0.2 | |

| BankRate 30 Year Fixed Rate Mortgage | 3.69 |

Markets are flat after a mixed ADP Employment report. They forecast that the private sector added 158k jobs in March, below the 200k estimate. February was revised upward, however to 237k. Mortgage Applications fell 4%. Bonds and MBS are flat

The Obama administration is pushing banks to lend to borrowers with weaker credit, encouraging them to use FHA loans and to use more subjective judgment in determining whether to offer a loan. Of course the CFPB has already drawn a line in the sand with DTI. Housing officials are urging the Justice Department to provide assurances to banks that they will not face legal consequences if they comply and the borrowers subsequently default. Working against this initiative is that (a) the CFPB has drawn a bright line around the qualifying mortgage and (b) Ginnie Mae will flush an originator when they get 5% to 10% portfolio delinquencies.

On the other hand, credit IS easing, especially for those who had short sales or foreclosures during the housing bust. Of the 7 million borrowers who had a foreclosure or a short sale, about 1 million are eligible for an FHA mortgage. Second, the return of the private label market (however small) will allow borrowers who don’t fit in the government bucket or the super high quality jumbo bucket to get financing.

Fannie Mae’s record profit has some questioning the future of the housing finance. According to the Administration’s White Paper, the intention seemed to be that the government would euthanize Fan and Fred and replace them with an entity that would act as a re-insurer. However, with more pressing issues facing the Administration, dealing with the GSEs has taken a back seat. In the interim, they are improving their balance sheets and have paid back nearly half of what they owe to the government. And with the stock approaching $1.00, the 4.6 billion shares owned by the government start to become significant. It will become harder to kill the company when the stock is worth some money. That is obviously what the market has figured out, as the stock has tripled since Fannie announced they will be profitable nearly 3 weeks ago.

Chart: Fannie Mae Stock Price:

Filed under: Morning Report | 19 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1562.2 | 6.3 | 0.40% |

| Eurostoxx Index | 2651.8 | 27.7 | 1.06% |

| Oil (WTI) | 97.01 | -0.1 | -0.06% |

| LIBOR | 0.282 | -0.001 | -0.18% |

| US Dollar Index (DXY) | 82.75 | 0.016 | 0.02% |

| 10 Year Govt Bond Yield | 1.85% | 0.01% | |

| Current Coupon Ginnie Mae TBA | 104.6 | 0.0 | |

| Current Coupon Fannie Mae TBA | 103.3 | -0.1 | |

| RPX Composite Real Estate Index | 189.5 | -1.1 | |

| BankRate 30 Year Fixed Rate Mortgage | 3.68 |

Markets are higher after Europe returned from a 4 day weekend. Italian sovereign yields are dropping, which is easing concerns about the Cyprus situation. Later this morning, we will get the ISM New York, factory orders and vehicle sales. Bonds and MBS are down small.

Fannie Mae just reported the largest net income in company history. Good thing they didn’t release this yesterday or nobody would have believed it. They reported net income of $17.2 billion for 2012 and $7.6 billion in the 4th quarter. The refi boom of 2012 has certainly helped them, along with a drop in delinquencies, increasing home prices, and higher sales of Fannie Mae-owned properties. They still owe Treasury $85 billion. Fannie Mae stock has rallied from 30 cents a share two weeks ago to 80 cents a share as of yesterday on reports they will be profitable. The stock is trading up a nickel on low volume pre-market. Every dime the stock increases is roughly half a billion dollars in the US government’s coffers.

The Consumer Financial Protection Bureau has a new one-stop shopping site for financial gripes. They do not verify the facts of the complaints, but they give the company a chance to respond before they put it on their site. If you had ever been mad at your bank and wanted to create a http://www.thiscompanysucks.com website, well, there ya go.

Mohammed El-Arian says that the Cyprus situation is not fixed, just temporarily stabilized. Even if it doesn’t become a systemic problem (read: spread to Italy and Spain) it still could create a systemic threat if enough peripheral countries have issues. The EU seems to be against an Iceland-style fix, where Cyprus leaves the EU and devalues its currency.

Filed under: Morning Report | 183 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1562.4 | -0.3 | -0.02% |

| Eurostoxx Index | 2624.0 | 11.6 | 0.44% |

| Oil (WTI) | 96.53 | -0.7 | -0.72% |

| LIBOR | 0.283 | -0.001 | -0.35% |

| US Dollar Index (DXY) | 82.94 | -0.032 | -0.04% |

| 10 Year Govt Bond Yield | 1.88% | 0.03% | |

| Current Coupon Ginnie Mae TBA | 104.4 | -0.2 | |

| Current Coupon Fannie Mae TBA | 103 | -0.2 | |

| RPX Composite Real Estate Index | 190.5 | -0.3 | |

| BankRate 30 Year Fixed Rate Mortgage | 3.67 |

Markets are flat this morning as most European markets are closed for the Easter Holiday. We are kind on a lull period until next Monday when Alcoa kicks off earnings season. Bonds and MBS are down small.

The Markit U.S. Preliminary March Purchasing Managers Index rose to 54.9 from 54.3 in February, indicating that the economy is expanding at a faster rate. Most indicators (new orders, employment, backlog) indicated the economy was expanding and accelerating. The Markit PMI is different than the more widely followed Institute of Supply Management Survey, which uses different weightings.

NPR has a good backgrounder on how strength in housing feeds other sectors of the economy. Punch line: the wealth effect, which was given up for dead in 2008 has returned. As home equity grows, people start spending again.

The Feds are getting closer to Stevie Cohen. They have arrested Micheal Steinberg, one of Cohen’s senior lieutenants, who was implicated in insider trading in Nvidia and Dell.

Filed under: Morning Report | 57 Comments »

Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1558.1 | 1.3 | 0.08% |

| Eurostoxx Index | 2633.5 | 21.0 | 0.80% |

| Oil (WTI) | 96.39 | -0.2 | -0.20% |

| LIBOR | 0.283 | -0.001 | -0.35% |

| US Dollar Index (DXY) | 83.07 | -0.148 | -0.18% |

| 10 Year Govt Bond Yield | 1.85% | 0.01% | |

| RPX Composite Real Estate Index | 190.5 | -0.3 |

Markets are flattish on the last trading day of the quarter. 4Q GDP was revised upward from + .1% to + .4%. Personal consumption was revised downward as well. Initial Jobless Claims rose last week to 357k. Bonds and MBS are flat.

The bond markets close at 1:00 pm EST today. Expect very little action today as traders will probably flatten positions ahead of quarter end.

The Office of Comptroller of the Currency has released the 4Q mortgage performance metrics. 89.4% of all mortgages are current, up from 88.6% last year. Delinquencies and foreclosures are down as the pipeline gets cleared and real estate prices start rebounding. More and more servicers are turning to mods as opposed to foreclosure initiations. The recidivism rate on these mods is around 17%.

The Private Label Securitization market is returning faster than people thought. Prior to this year, the only deals were the occasional Redwood Trust jumbo deal. JP Morgan recently announced a deal, and now Springleaf plans a $1 billion subprime deal. The palette of products originators can offer is expanding in a big way.

FHFA has made mods easier to do on delinquent mortgages – anyone who is more than 90 days delinquent is automatically eligible for a loan mod. Borrowers do not have to show a financial hardship any more. This will only apply to Fan and Fred loans, and mods will be rate / term, not principal reductions. So this begs the question: Why won’t everyone stop paying their mortgage in order to get a mod? FHFA said they would use existing “screening measures to prevent strategic defaulters.” Whatever that means.

Is your house an undiversified bond investment? Was house price appreciation driven by falling interest rates? And does that mean that when rates start rising house prices will fall again? I would point out that interest rates aren’t the only factors affecting home prices – population growth, incomes, the availability of credit, and even global capital flows play a role. He does have a point, which is that a rapid rise in home prices like we saw from the early 90’s to 2007 is unlikely to be repeated given that we won’t have the tailwind of falling interest rates to increase affordability. That said, low interest rates can last a long time – from the end of WWI to the mid 60’s, short-term rates were 5% or lower. From 1932 to the mid 50’s, short term rates were under 2.5%. I would also point out that real estate prices increased during the 1970s, even as short term rates moved up to 15%.

Filed under: Morning Report | 24 Comments »