Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1867.6 | -5.5 | -0.29% |

| Eurostoxx Index | 3164.6 | -25.2 | -0.79% |

| Oil (WTI) | 101.1 | -0.8 | -0.83% |

| LIBOR | 0.227 | -0.001 | -0.55% |

| US Dollar Index (DXY) | 79.68 | -0.120 | -0.15% |

| 10 Year Govt Bond Yield | 2.68% | -0.01% | |

| Current Coupon Ginnie Mae TBA | 105.6 | 0.1 | |

| Current Coupon Fannie Mae TBA | 104.5 | 0.0 | |

| BankRate 30 Year Fixed Rate Mortgage | 4.24 |

Stocks are lower this morning on no real news. Emerging markets continue to sell off. Bonds and MBS are up small.

University of Michigan Consumer Confidence picked up in April, from 82.6 to 84.1.

The Markit Purchasing Managers Index fell slightly to 54.9 from 55.7. The Markit Services PMI fell as well. These readings are still well above neutrality, but it looks like things cooled a bit in April. The employment numbers were not great – the expansion in service sector payroll was the weakest in almost 2 years. Input prices (primarily food and energy) increased.

Rep. Elijah Cummings (D-MD) wants to exhume the robo-signing scandal and hold hearings on it. There was an ongoing investigation of servicing misdeeds during the foreclosure process that was eventually shut down when the government realized the only people making any money on it were the consultants, not aggrieved homeowners. Apparently the consultants walked away with $1.9 billion and homeowners got nothing. Seems to me to be a lot of money to pay consultants to review foreclosure files. But that probably explains why 6 of the 10 richest counties in the US surround DC.

Speaking of regulators going after the banks, the government is looking for more that $13 billion from Bank of America over RMBS deals. If B of A wasn’t asked to buy Countrywide from the government, that deal will go down in history as one of the worst mergers ever. If the government asked B of A to buy Countrywide, then the government is exhibiting absolutely reprehensible behavior.

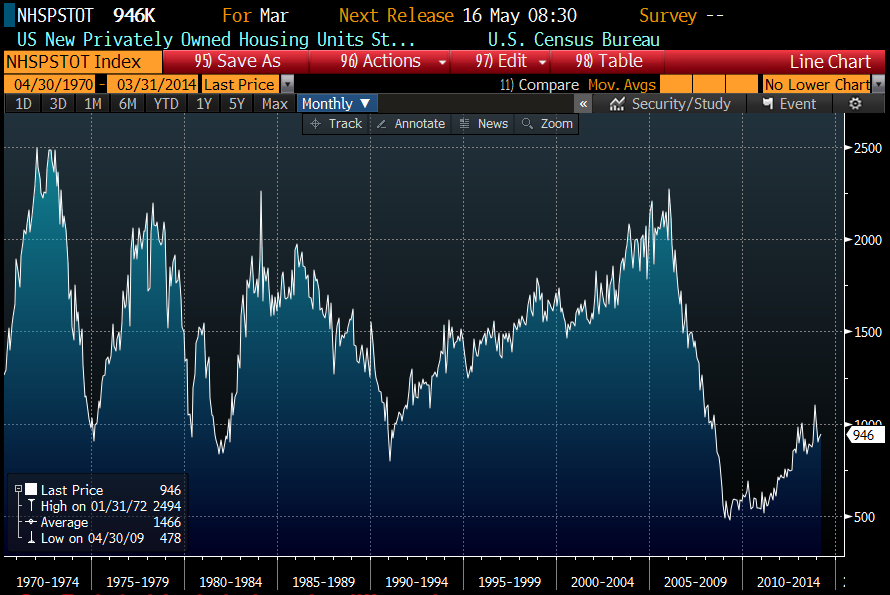

The Wall Street Journal has a good article on how demand for home loans has fallen off as buyers experience sticker shock. Last year at this time, mortgage rates were 75 basis points lower, and home prices were 13% lower. This has caused affordability to take a hit, although real estate is still highly affordable compared to historical numbers. As a result, housing continues to punch below its weight in terms of contributing to economic growth. That said, the thing that jumped out in reviewing the homebuilder earnings is that the growth is pretty much coming from increases in average selling prices. For example, Pulte had flat year-over-year revenues which consisted of a 10% increase in ASPs and a 10% drop in deliveries. The builders have probably increased prices as far as they can, and will now have to push out volume to keep increasing the top line. In my opinion, that is what is going to break the logjam in the economy. The builders are coming up against some tough comparisons, and are not going to want to report revenue declines. Which means more building, which puts more people to work, which gets the virtuous cycle going again. At some point, the job market will improve enough to bring the first time homebuyer back, which is the key to a meaningful recovery in housing and is the difference between housing starts of 900k and 1.5 million.

Filed under: Morning Report | 48 Comments »