Posted on February 23, 2016 by Brent Nyitray

Stocks are lower this morning on fears of another yuan devaluation. Bonds and MBS are down.

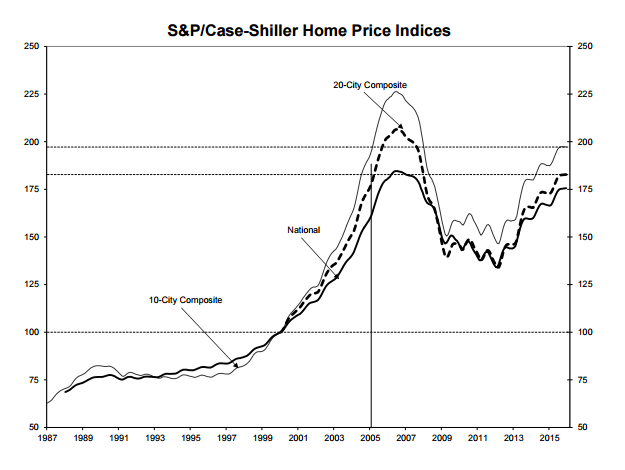

Home Prices continued to rally in December, according to the Case-Shiller Home Price Index. They were up 0.8% on a month-over-month basis and up 5.7% on a year-over-year basis. Prices remain about 11.5% below their July 2006 peak. Note the FHFA House Price index which we will get on Thursday is already at new highs.

Existing Home Sales were up 0.4% at 5.47 million units in January, according to the National Association of Realtors. On a year-over-year basis, they are up 11%, the biggest gain in 3 years. The median home price rose 8.2% year-over-year to $213,800 as supply constraints continue to drive up prices. Housing inventory is 1.82 million units, which represents a 4 month supply. A balanced market is more like 6 – 6.5 month’s worth. Ultimately, the big price increases are unhealthy because incomes have yet to really exhibit growth (although that may be changing). The median house price to median income ratio is roughly 3.8x, using the median income data from Sentier. 3.3 – 3.7x which is about normal.

Speaking of home supply, McMansion builder Toll Brothers reported earnings this morning. Revenues were driven again by an 11.7% increase in average selling prices and not by unit growth. Gross margins fell, which speaks to increasing costs. So far this February, deposits and contracts are flat with last year. The decline in stocks probably has a lot to do with it as the luxury buyer is going to be more sensitive to asset prices than the first time homebuyer.

Interesting to see this dynamic with the builders – a reluctance to build more units despite higher prices. Interestingly, CalAtlantic (the new name for Standard Pacific and Ryland after their merger) is bringing back the buydown loan.

In other economic news, consumer confidence slipped in in February, and the Richmond Fed Manufacturing Index both fell.

Blackrock is warning clients that the Fed is not likely to sit out the rest of 2016, the way the Fed Funds futures markets are predicting. Efficient market theorists might scoff at that notion, however the interest rate markets are so manipulated by central banks at the moment it makes sense to look at market signals with a jaundiced eye. What does that mean to mortgage types? Make hay now, because no one knows how long these low rates are going to stick around.

Speaking of credit markets, the new subprime – auto loans – are beginning to exhibit signs of trouble. Auto loans are being priced like mortgages, however a mortgage is secured by a generally appreciating asset, while an auto loan is secured by a depreciating asset. This is the result of financial repression, which is the act of pushing interest rates to the floor. Investors who have to earn a return (like pension funds and insurance companies) are forced to move further and further out on the risk curve to earn their required return. The actuarial tables really couldn’t care less that interest rates are zero.

Filed under: Economy, Morning Report | 67 Comments »

Posted on February 19, 2016 by Brent Nyitray

Markets are lower this morning on no real news. Bonds and MBS are down.

Real Average weekly earnings increased 1.2% in January.

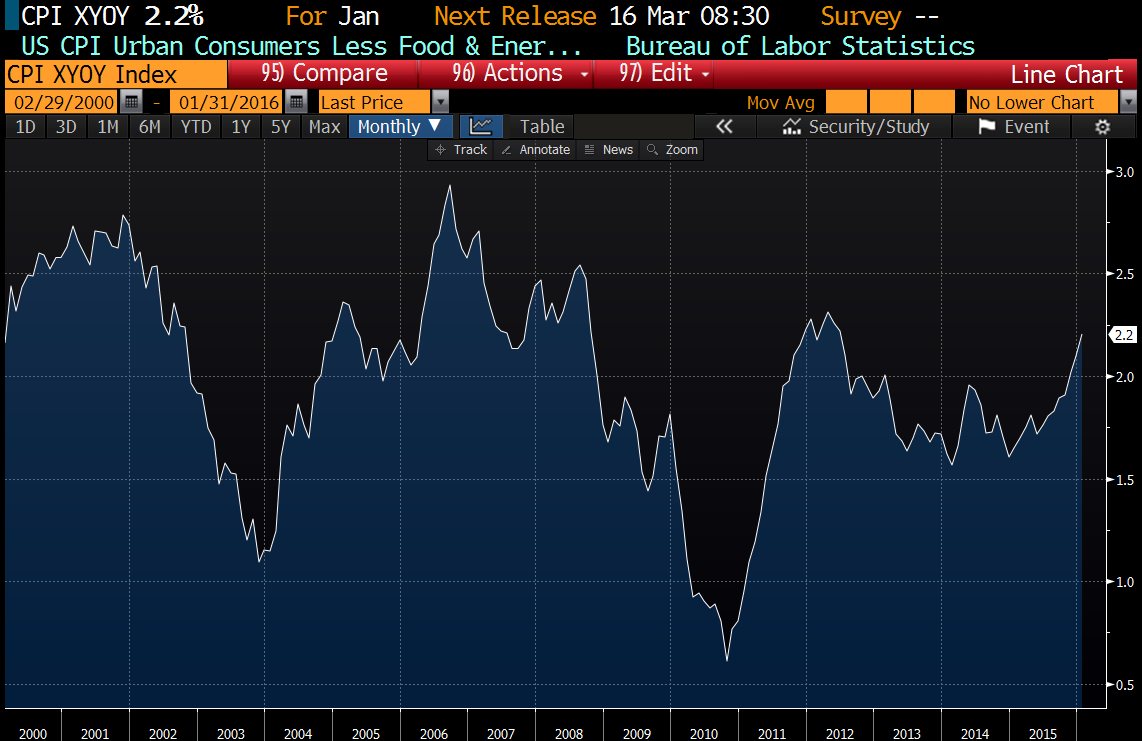

Inflation at the consumer level was flat month-over-month and up 0.3% YOY. Ex food and energy, it was up 2.2%, which is the highest level since June of 2012. This would indicate the Fed is actually getting there as far as its inflation target. That said, the Fed prefers to use the Personal Consumption Expenditure index, which is still below their target.

Chart: YOY inflation, ex-food and energy:

The thinking behind negative interest rates, explained. European economists give their take on it. Basically they work well in smaller. open economies as a lever to manipulate foreign exchange rates, but they aren’t all that effective for larger economies which are trying to boost inflation and growth. In other words, they might work for Denmark, but probably won’t do much good here. Japan recently went negative, so that will be a good test of that theory.

There is legislation afoot to eliminate the caps on VA loans, which will make them much more popular in high cost areas. Basically it will become a no money down jumbo. It has passed the House, and the prospects are good in the Senate and the WH.

Filed under: Economy, Morning Report | 65 Comments »

Posted on February 18, 2016 by Brent Nyitray

Stocks are higher this morning after oil continues its rally. Bonds and MBS are flat

Initial Jobless Claims fell from 269k to 262k., while the Philly Fed improved to -2.8.

The Bloomberg Consumer Comfort Index fell slightly to 44.3 from 44.5 the prior week. The Economic Expectations index fell markedly from 47 to 42.5.

The Index of Leading Economic Indicators improved slightly in January from -0.3% to -0.2%.

Mortgage Delinquencies fell from 4.99% to 4.77% and foreclosures fell from 1.88% to 1.77% in the fourth quarter, according to the MBA.

The FOMC minutes were released yesterday, and for the most part they were a non-event as far as the markets were concerned. The Fed did spend some time talking about the slowdown in China, and the reverberations in the markets. A number of officials are beginning to think the inflation forecasts are too high. In addition, the stresses in the financial system act as a tightening even if rates go nowhere. The Fed seems to be setting the stage for a cut in the GDP and inflation forecasts at the March meeting, as well as a pause in tightening. Separately, the OECD took down its forecast for global growth to 3.0% from 3.3%.

Mortgage REIT MFA Financial reported earnings this morning. They continue to position their portfolio of MBS more towards credit risk and less towards interest rate risk. When the private label securitization market comes back, REITs like MFA will be the big buyers of non-QM paper. Their appetite for non-agency MBS will be the key driver bringing back the widespread use of products that don’t fit in the agency box.

FHFA Chairman Mel Watt says that the GSE’s lack of capital is the most serious risk to the mortgage market right now. He says that guarantee fees have increased 25 basis points since 2009 and they are now “appropriate.” He also said that the current state of conservatorship is “not a desirable end state” and said that the GSE’s protection from market forces “presents itself in multiple decisions, including pricing.”

Filed under: Economy, Morning Report | 50 Comments »

Posted on February 17, 2016 by Brent Nyitray

Stocks are higher this morning as yesterday’s rally has follow-through on overseas markets. Bonds and MBS are down.

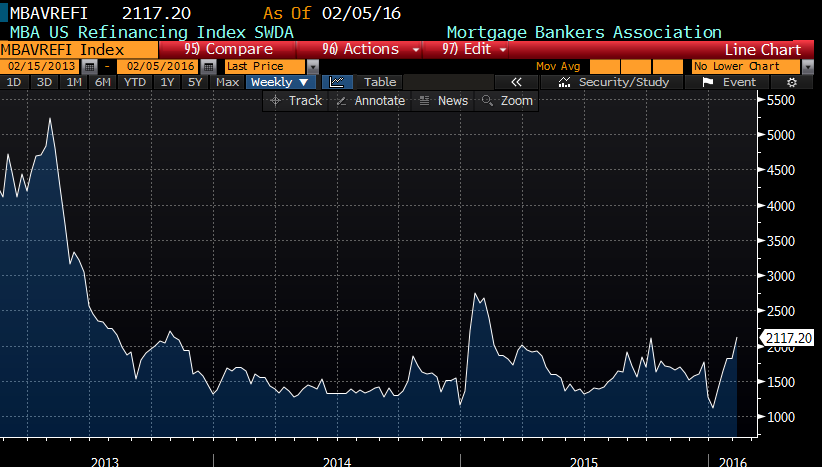

Mortgage Applications rose 8.2% last week as purchases fell 3.7% and refis rose 16%.

Housing starts came in 1.1 million, missing the 1.17 million estimate. Building Permits were flat at 1.2 million.

The Producer Price Index rose 0.1% in January. The core index (ex food and energy) rose 0.4%. The headline number was up 0.6% YOY and the core number was up 0.8%.

Industrial Production jumped in January by 0.9%, however the preior month was revised lower from -0.4% to -0.7%. Manufacturing Production rose 0.5%. Capacity Utilization improved markedly from 76.4% to 77.1%.

At 2:00 pm, we will get the FOMC minutes. Given the uncertainty around the Fed’s future plans, we could see the market more sensitive to these than usual.

Neel Kashkari of the Minneapolis Fed gave a speech to Brookings yesterday, calling for even more regulation for the banks and to turn them into public utilities. Of course any examination over whether the Fed had a hand in creating the real estate bubble in the first place is nowhere to be found.

Filed under: Economy, Morning Report | 61 Comments »

Posted on February 16, 2016 by Brent Nyitray

Green on the screen as investors return after a long weekend. Bonds and MBS are down small.

The Empire Manufacturing Index improved slightly to -16.64 versus -19.37 in the prior month.

The NAHB Homebuilder Sentiment Index fell to 58 from 61 in February.

Saudi Arabia, Russia, Venezuela and Qatar agreed to freeze production at January levels provided the other members of OPEC agree to go along. Apparently this has been in the works for a while, so oil isn’t having much of a reaction.

Household debt increased 0.4% in the fourth quarter, according to the NY Fed. Student Loan and Auto loan financing are growing the most, while mortgage and HELOC is steady or falling. Credit quality for mortgage debt remains strong, however you can see the increase in low-FICO auto loans (the new subprime). Debt levels below:

As the Spring Selling Season begins, inventory remains tight, especially close to urban areas. The supply of homes is the lowest since 2005.

Filed under: Economy, Morning Report | 75 Comments »

Posted on February 11, 2016 by Brent Nyitray

Global stock markets are down again on no real news. Whatever comfort markets took in Janet Yellen’s remarks yesterday are over. Bonds and MBS are up, with the 10 year bond yield pushing a 1.5% handle.

Loan officers, you have been given an unexpected gift with the 10 year. Rates are now at the pre “taper tantrum” level when the Fed started bracing the markets for the end of QE. So I guess the Fed didn’t need to purchase $4 trillion worth of assets to get rates down?

Initial Jobless Claims fell to 269k from 285k last week. It bears repeating that these numbers are exceptionally good and are associated with boom times. The tape doesn’t care, but still…

The Bloomberg Consumer Comfort Index rose slightly to 44.5 from 44.2 last week. Lower gasoline prices are helping improve the mood.

Most commodities have been getting crushed lately, however one has been on a tear: Gold. Gold is a strange animal, in that it is one of the few financial assets that isn’t some else’s liability. The price of gold can be considered to be the (inverse) confidence indicator in the world’s central banks. Gold up, confidence down.

Continuing on the central bank thread, one of the bright spots in the US markets has been auto sales. This has been driven by a couple things: The biggest was that people deferred replacing cars until they absolutely had to due to the lousy economy. However another reason is cheap credit, and some hedge funds think they have found the new “big short” in subprime auto. When you can get an 8 year loan for a new car at a rate below the 30 year fixed rate mortgage, something is awry.

So, yet another pillar holding up the economy was based on cheap credit. Janet Yellen must feel like Michael Corleone: “Just when I thought I was out, they pull me back in.”

The House Financial Services Committee is having a hearing today on FHA MIP. Expect Democrats to push for another cut and Republicans to be against it. The Democrats are in a strange position with the base continuing to push for even tougher regulations for the industry and the affordable housing types getting sick and tired of the tight credit that results.

Filed under: Economy, Morning Report | 76 Comments »

Posted on February 10, 2016 by Brent Nyitray

Stocks are higher this morning based on prepared testimony for Janet Yellen’s appearance before Congress. Bonds and MBS are down small.

Keep in mind that the Chinese stock market is closed all week in observance of the Chinese New Year, so the biggest catalyst for downside movement in the markets will be absent this week.

Janet Yellen is traveling to the Hill for her Humphrey Hawkins testimony. In her prepared remarks she did spend some time talking about the turmoil in the financial markets and that acknowledgement was soothing enough to stocks to give them a boost. Overall, however the message is that the US economy is improving, and rate are going up gradually. The rest of the testimony will probably be a bunch of ideological questions from various congresscritters trying to get the Chairman of the Fed to agree with their ideological worldview.

Goldman is forecasting 3 rate hikes in 2016. Given the overall weakness in the global economy and the rush to negative interest rates globally, it may not affect long-term interest rates in the US (or mortgage rates for that matter).

Blackrock is forecasting that US growth has probably peaked for the near term as more and more central banks enter the negative interest rate vortex. I wonder what our grandkids will think about today’s PhD standard. If it ends up not working, do we go back to the gold standard?

In New Hampshire, Bernie Sanders won the Democratic primary vote, and Donald Trump won the Republican primary vote. John Kasich had a surprisingly strong showing.

Mortgage Applications rose 9.3% last week as purchases were up 0.2% and refis were up 15.8%. The refi index has had a nice run since rates started collapsing, but we are nowhere where we used to be compared to 2013.

Competition in the jumbo market is fierce, and the typical rate for a jumbo is now 15 basis points below a conforming mortgage. Historically, jumbos have cost an extra 25 basis points to the borrower.

Do you think your underwriters are approving too many shaky loans? Move them to Seattle. Are they too conservative? Move them to San Diego.

Filed under: Morning Report | 52 Comments »

Posted on February 9, 2016 by Brent Nyitray

Markets are down after yesterday’s blood bath. Bonds and MBS are up small.

Since the Fed tightened rates at the December meeting, the 10 year bond yield has fallen by 58 basis points. Fun fact: The Japanese 10 year bond yield is now negative.

In economic data, the NFIB Small Business Optimism Index fell from 95.2 to 93.9 last week. This is surprisingly tame given the activity in the markets over the past couple months. That said, small business optimism didn’t ride the post-2009 rally in the markets up, so it probably will be a little insulated on the way down. Hiring plans remain intact, which is a good sign, however finding qualified applicants continues to be an issue.

Job openings are pushing close to new highs, according to the JOLTS job report. Quits are increasing, which is a bullish sign for the labor markets.

Bottom line: the markets are signalling pain in the global economy, but it is hard to draw the conclusion that conditions in the US are driving it. If anything, the US appears to be taking its historical role of the engine of growth in a soft global economy.

The canary in the coal mine (besides oil) has been the absolute carnage in the banking sector, especially overseas. Deutsche Bank has been cut in half since September. Same as Credit Suisse. Citigroup is down 27% since Jan 1. So is BNP Paribas. Not sure what this is signalling (exposure to energy? exposure to China?) but it is a big warning button for the global economy and it is flashing red.

Even though the economy has recovered, the hatred of the financial sector hasn’t changed, and it is being channeled through Bernie Sanders. The ironic thing is that the “Wall Street” they are railing against hasn’t existed for 10 years. Regardless it isn’t an environment conducive to risk-taking.

Speaking of politics, the New Hampshire Primaries are today. Clinton and Sanders look neck and neck, and Trump looks to be ahead of the pack for the Republicans.

Filed under: Morning Report | 13 Comments »

Posted on February 5, 2016 by Brent Nyitray

Stocks are lower this morning after the jobs report. Bonds and MBS are down

- Nonfarm payrolls + 151k vs 190k expected

- Unemployment rate 4.9%

- Average Weekly Hours 34.6

- Average Hourly Earnings up 2.5%

- Labor force participation rate

Overall a good report, Payrolls are disappointing, but the rest is strong. We are starting to see the beginning of wage inflation with average hourly earnings up 2.5%. December’s number was revised upward from 2.5% to 2.7%. Stocks and bonds are down as this report will keep pressure on the Fed to maintain its posture of normalizing rates. The 2-year yield is higher by 4 basis points.

Higher wage inflation coupled with no inflation equates to lower profit margins. Ironically, this is the sort of “middle class economy” that politicians are promising to bring back. Good for workers, not so much for investors.

The rise in the dollar and the corresponding fall in commodity prices is wreaking havoc on other economies though. Citi is saying fear oilmageddon. This will be felt not only in developing economies like Russia and Brazil, but also developed economies like Canada and Norway. Norway’s “economic miracle” may have simply been a massive leveraged bet on oil and real estate.

Filed under: Morning Report | 36 Comments »

Posted on February 4, 2016 by Brent Nyitray

Stocks are lower this morning after we got some disappointing economic data. Bonds and MBS are up small.

Dismal economic numbers all around this morning

Productivity fell 3% in the fourth quarter and unit labor costs rose 4.5%. This is a recipe for falling profits in 2016. Given the tepid GDP growth being forecast for next year (sub 2%), companies will focus most on cost-cutting. Given the excess capacity in the manufacturing economy, companies have been reluctant to spend on capital expenditures, which has depressed productivity. Definitely not a recipe for releasing the animal spirits, although if builders start to address the tight supply, it will provide a good boost for the economy.

Factory orders fell 2.9% in December, which was below the Street estimate. November’s numbers were revised downward as well.

Durable Goods orders fell 5% in December as well. Capital Goods orders (a proxy for capital expenditures by business) fell by 5%. This directly relates to the lousy productivity numbers above.

Initial Jobless Claims rose 285k last week.

The Bloomberg Consumer Comfort Index fell from 44.6 to 44.2 last week.

Don’t underestimate the Fed, which is the message from major strategists. Goldman Sachs Chief Economist Jan Hatzius is calling for a 3% 10 year by the end of the year.

Both Republicans and Democrats agree the economy is lousy, and both sides are going back to their boilerplate explanations. Democrats blame Wall Street and the rich, while Republicans blame government. The funny thing is that the “Wall Street” they rail against hasn’t existed for almost 10 years.

Filed under: Morning Report | 12 Comments »