Posted on June 15, 2016 by Brent Nyitray

Stocks are higher this morning as we await the FOMC decision at 2:00 pm today. Bonds and MBS are flat.

Bonds had a sensational rally yesterday, with the 10 year yield falling to 1.57% and the German Bund going negative before giving it all back. The Bund is basically at zero this morning.

The FOMC decision is due out at 2:00 pm EST today. No one is expecting a rate increase, but we the press release and press conference might have some market-moving news. We will also get new a new Fed Funds dot graph and updated forecasts for inflation, unemployment, and GDP growth. Here is a primer on what to look for.

Mortgage Applications fell 2.4% last week as purchases fell 4.9% and refis fell 0.7%. Refis accounted for 55% of the total number of loans.

Inflation remains in check at the wholesale level, as the producer price index rose 0.4% MOM and fell 0.1% YOY. Ex food and energy, the PPI was up 1.2%, much lower than the Fed’s 2% target rate.

Paul Singer of Elliott discusses central banks and how all of their policies have been slowing growth and exacerbating inequality. He is bearish on stocks, bullish on gold. Separately, Jeffrrey Gundlach of DoubleLine says that central bankers are losing control.

Completed foreclosures ticked up to 37,000 in April from 36,000 a month ago, however they are down 16% YOY. The foreclosure inventory is just over 400,000 homes, which works out to be 1.1% of all homes with a mortgage. This number is down 23.4% from a year ago. Foreclosure inventory remains concentrated in the Northeast, Florida, and the sand states.

iServe got a nice mention in Rob Chrisman’s blog this morning. If you want to learn more about VA loans, we conduct seminars all over the US with our VA expert. We serve those that served.

In other economic news, the New York State Empire Manufacturing Index rebounded in June, while industrial production and manufacturing production fell in May. Motor vehicles (which can be volatile) accounted for a big part of the drop. Capacity Utilization fell to 74.9%. Interestingly, more CEOs intend to increase capital expenditures than they did in the first quarter.

Filed under: Economy, Morning Report | 22 Comments »

Posted on June 13, 2016 by Brent Nyitray

Stocks are lower this morning on fears over Brexit (The 6/23 vote to decide whether the UK leaves the EU). Bonds and MBS are up small.

No economic data today. The big event this week will be the FOMC meeting Tuesday and Wednesday. The markets are expecting no changes to interest rates, so any bond rally on the news of no changes will probably be limited.

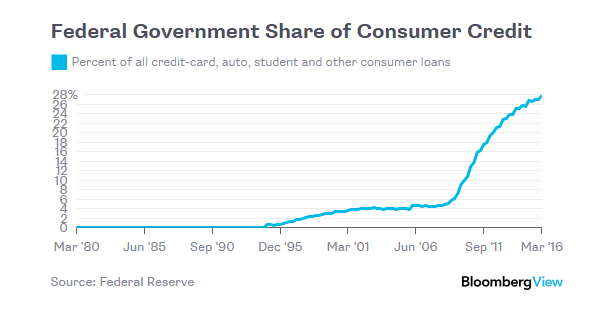

Interesting chart about the Federal government’s percent of ownership of consumer debt. This is money that US citizens owe Uncle Sam. Ever since Obama nationalized the student loan sector, they have taken their percentage of consumer debt from 5% to 28%. The student loan market is a $1.3 trillion market – not exactly chump change. Expect some sort of write-down of student loan debt in the future: many graduates have degrees that will never pay enough to work this down. As a side note, more young adults aged 18-34 live at home with Mom and Dad than in any other arrangement.

Speaking of Millennials, the high student loan debt is causing lower credit scores. The average credit score for the 18-34 age cohort is 625, compared to the national average of 667. Almost a third of that age cohort have sub-600 scores. Good luck getting a loan with that. Finally, all of the new post-2008 regulations have added anywhere form 50k-100k to the cost of building a starter home, making it difficult for builders to make homes that are affordable for the first-time homebuyer.

There is now $10 trillion worth of global sovereign debt trading at negative yields. Bill Gross of Janus Capital calls that a “supernova” that will explode one day. All of the worlds’ central banks are on a mission to create inflation: one day they will succeed. What has been the best trade for bond investors lately? The Japanese 30 year bond, which now yields 28 basis points. Bill says that bond yields today are the lowest in 500 years. Not sure where he comes up with that number.

Speaking of Central Bank jiggery-pokery, ECB corporate bond buying now makes up for 1 in 5 trades. We are truly in uncharted waters with global central banking.

As a general rule, buy stocks in an election year. Election years tend to be optimistic times, and the Fed is usually on your side. That might not be the case this year.

Filed under: Economy, Morning Report | 27 Comments »

Posted on June 10, 2016 by Brent Nyitray

The 10 year has broken out of its range and is now trading at 1.65%. The catalyst has been lower rates throughout the world. The German 10 year Bund is now trading at 2 basis points. The Japanese Government Bond yields negative 13 basis points. At some point, gold has to become interesting as an investment. The knock on gold was always that there is no yield, but compared to long term sovereign bonds that have no yield and (probably) no upside, why not? Definitely a better risk / reward.

Mortgage originator and servicer Walter Investment got slammed yesterday after the CEO resigned. Regulatory difficulties and costs were the catalyst. The stock has lost 82% of its value over the past year.

In economic news, initial jobless claims fell to 264k from 268k the week before. So in spite of the low job creation numbers, we aren’t seeing firms lay off people yet.

Consumer confidence fell slightly in June to 94.3 from 94.7 according to the University of Michigan Consumer Sentiment Survey

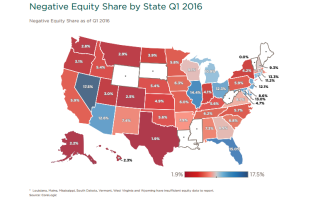

268,000 homes regained positive equity in the first quarter, according to CoreLogic. They estimate that 4 million homes (or about 8% of the homes with a mortgage) have negative equity. 18% of homes have less than 20% equity. Negative equity remains a problem in the Northeast, the Rust Belt and FL, NV, and AZ.

Ex Fed Head Narayana Kochlerakota argues the Fed should be doing more to get inflation up. Not only should they hold off on raising rates until the core PCE is above 2%, but it should pay nothing on excess reserves.

Filed under: Economy, Morning Report | 15 Comments »

Posted on June 8, 2016 by Brent Nyitray

Markets are higher this morning on no real news. Bonds and MBS are flat

Mortgage applications rose 9% last week as purchases rose 11.7% and refis rose 7.4%. Interest rates were flat for most of the week until the jobs report on Friday, so these are good numbers, all things considered. The 10 year continues to bump to see resistance at the 1.7% level.

Job opening increased to 5.8 million in April, according to the JOLTS report, which matches a record set last July. Hires and quits fell however, which is another reason for the Fed to stand pat at the FOMC meeting next week.

Separately, a survey of CFOs indicates that companies are holding off hiring due to uncertainties regarding regulation and the general machinations in DC. Interestingly, hiring and retaining skilled labor came in as the #2 concern from #5 last year. That corroborates what the JOLTS report is saying: there are a lot of openings for skilled labor, but hirings are down because skilled labor is tough to find. On the other side of the coin, unskilled labor is becoming more expensive due to the recent spate of minimum wage hikes, which is creating an even bigger glut as companies substitute technology for labor.

Hillary Clinton won California and has enough delegates to sew up the nomination. Donald Trump continues on his mission to alienate as many people as possible. The big question is Bernie Sanders. Given the backdrop of the FBI investigation, he may decide to stick around until that is settled. That said, Obama has signalled that Hillary did nothing wrong, and I am sure his DOJ and his FBI has taken note. The Democratic establishment is going to put more and more pressure on Bernie to throw his support behind Hillary and unite to defeat Trump.

Republicans are drafting a bill to fix some of the issues with Dodd-Frank, particularly Volcker rule and some of the issues with the CFPB. Banks that meet capital requirements will be allowed to prop trade, and the CFPB will come under Congressional oversight and have a Board instead of a single director. There are two issues this is intended to fix. First, market making almost doesn’t exist any more as banks are afraid to venture too close to proprietary trading and the Volcker rule. The next crash (and there will be one) investors will be in for a rude awakening when they cannot sell their less liquid stocks because there is no bid. It will be even worse for bonds, and could be a major issue for ETFs. The second issue is the CFPB, which is regulating by enforcement action. Consumer advocates are getting sick and tired of tight credit, which is creating some consternation with other members of the left who still think the banks are unregulated and need to be reined in. Elizabeth Warren is leading the charge against this, which makes sense since the CFPB is her baby.

Filed under: Economy, Morning Report, politics | 6 Comments »

Posted on June 2, 2016 by Brent Nyitray

Markets are lower this morning as ECB President Mario Draghi speaks. Bonds and MBS are flat.

The ECB will now start buying corporate bonds in an attempt to stimulate their economies. Truly an amazing time we live in.

We get some labor market data this morning, before the big jobs report tomorrow.

The ADP Employment Change report came bang in line with expectations at 173k jobs created. Tomorrow’s non-farm payroll expectation is for an increase of 160k jobs created in May. Small business led the way, adding 76k employees. Professional and business services increased the most. Manufacturing jobs fell.

Initial Jobless Claims came in at 267k last week,

Homebuilder Hovnanian reported second quarter earnings this morning. Deliveries were up 31% and revenues were up 40%. Earnings were still below expectations. The stock is down this morning

US auto sales fell in May, which is usually one of the stronger months for auto sales. Auto sales had been increasing for 6 years, pushed by a stronger economy and ridiculously cheap financing. Yield pigs may find that doing 8 year auto loans at 3.5% is a dumb trade.

Despite being disappointed by the current crop of presidential candidates, consumers still plan to buy cars and houses. Despite all the rhetoric, the economy is not doing all that badly, and there is tremendous pent-up demand for housing, especially from younger buyers. The issue for them is affordability, and tight inventory combined with a lack of building is making it hard.

The House included language in the 2017 budget to bring Congressional oversight to the CFPB and subject it to the appropriations process. Currently, it is funded by the Fed, who really has no choice but to give them what they want. Second, the provision would replace the single director with a five-member board appointed by the President. While this is going nowhere (we haven’t had a budget since early in Obama’s Presidency), it will be fodder for the fall elections. For the moment, it appears the CFPB is directing its attention to payday lenders.

Filed under: Economy, Morning Report | 91 Comments »

Posted on June 1, 2016 by Brent Nyitray

Markets are lower this morning on overseas weakness. Bonds and MBS are up.

Mortgage Applications fell 4.1% last week as purchases fell 4.7% and refis fell 3.9%. Refis ticked up to 54.3% of the total number of loans.

The ISM Manufacturing report came in better than expected, indicating that the manufacturing economy is expanding, albeit modestly. The ISM services number is much more important, as manufacturing only represents 15% of the economy. It looks like the exporters are getting hit harder than those who mainly focus domestically. Employment was flat month-over-month, however it is in a contracting trend.

Construction spending fell 1.8% month-over month, however the previous 0.3% print was revised upward to 1.5%. Residential construction fell 1.5% month-over-month, however it is up 8% YOY.

As we saw from the FHFA House Price index, home prices have recouped their losses from the bubble years. Is it time to start worrying about a new housing bubble? Freddie Mac takes a look at real estate prices relative to incomes, credit scores, inventory, and leverage in the system and concludes that it is not yet time to worry. While house prices are indeed stretched relative to incomes, that figure ignores the effect of interest rates. The overall credit profile for new originations has been strong since the crisis, and while we are beginning to see some credit deterioration in the oil states, it is nothing like 2007-2008. Tight inventory remains a huge issue in terms of pricing, and notwithstanding last week’s 617k print on new home sales, new construction is still well below historical levels. Consumers are increasing mortgage debt, however they seem to be using the cash-out refi to pay down credit card debt instead off funding consumption. The froth in the housing market still remains concentrated in the big coastal urban areas like San Francisco and Manhattan, which is driven by foreign demand.

At the end of the day, bubbles are psychological phenomenons, where investors and lenders both believe an asset is “special” and cannot go down in price. We will probably never see another real estate bubble, but our grandkids might. If anything, the bubble is in sovereign debt, and people will wonder why investors chose to tie up their money for 10 years for negative returns. Purchasing a German Bund yielding 13 basis points over 10 years is in the same category as buying a new construction McMansion in Stockton CA circa 2006 or paying $76 a share for E Toys the day of its $20 IPO in 1999.

Auto sales are coming in this morning, and it looks like they are coming in weaker than expected.

Interesting editorial by Clintonite Doug Schoen who says Hillary might not be the Democratic Party nominee. There is talk in the Democratic party about a white knight candidate, like Joe Biden or John Kerry who could enter the race at the convention, and select someone like Elizabeth Warren to be VP.

Filed under: Morning Report | 35 Comments »

Posted on May 31, 2016 by Brent Nyitray

Markets are up this morning after Chinese stocks rallied overnight. Bonds and MBS are down.

The second revision to first quarter GDP came in at 0.8%, slightly below the Street estimate of 0.9%. This was an upward revision from the initial 0.5% estimate.

Personal incomes rose 0.4% in April, in line with expectations. Personal spending rose 1%, which topped the 0.7% estimate. The personal consumption expenditures index (which is the inflation measure preferred by the Fed) rose 0.2% month-over-month and is up 1.6% annualized. We are seeing some sell-side firms take up their second quarter GDP estimates on this number.

Home prices rose 0.9% MOM and 5.4% YOY, according to the Case-Shiller Home Price Index. This was slightly ahead of estimates. An improving labor market along with tight inventory is driving prices higher.

In other economic data, both the Chicago Purchasing manager index and the consumer confidence index fell.

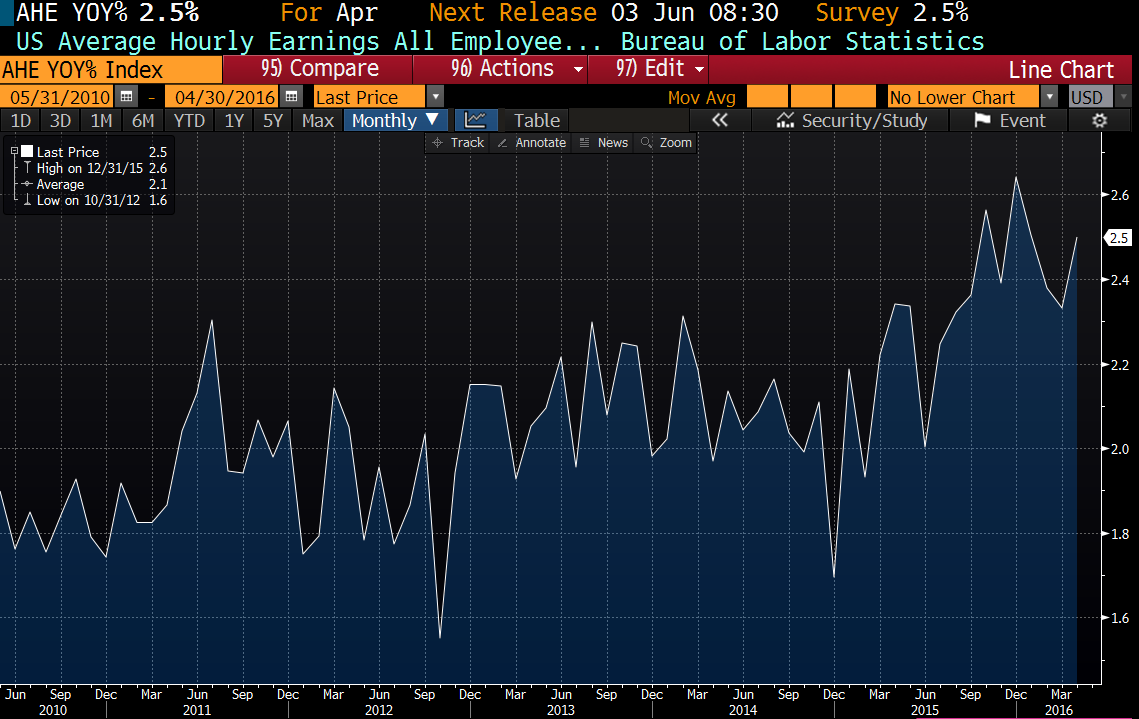

The highlight of this short week will be the jobs report on Friday, which will be the last big data point before the FOMC meeting in a couple of weeks. The number to watch: average hourly earnings. Average hourly earnings growth has been accelerating over the past 6 months or so, to around 2.5%. You can see the trend in average hourly earnings growth in the chart below:

On Friday, Janet Yellen hinted that the next rate hike is probably at the June or July FOMC meetings.

Filed under: Economy, Morning Report | 4 Comments »

Posted on May 25, 2016 by Brent Nyitray

Stocks are higher this morning as emerging markets rally. Bonds and MBS are down.

Mortgage Applications rose 2.3% last week as purchases rose 4.8% and refis rose 0.4%. The average 30 year fixed rate mortgage rose 3 basis points to 3.85%. The average jumbo rate increased 8 basis points to 3.82%.

Home prices rose 0.7% in March, according to the FHFA House Price Index. “While the overall appreciation rate was robust in the first quarter, home price appreciation was somewhat less widespread than in recent quarters,” said FHFA Supervisory Economist Andrew Leventis. “Twelve states and the District of Columbia saw price declines in the quarter—the most areas to see price depreciation since the fourth quarter of 2013. Although most declines were modest, such declines are notable given the pervasive and extraordinary appreciation we have been observing for many years.” Interesting to see prices begin to decline in some states.

A US appeals court threw out the $1.27 billion judgement against Bank of America for Countrywide’s sins related to the “hustle.” The 2nd U.S. Circuit Court of Appeals in New York said the proof at trial was insufficient under federal fraud statutes to establish liability. No comment yet from Manhattan U.S. Attorney Preet Bharara.

Filed under: Economy, Morning Report | 39 Comments »

Posted on May 25, 2016 by Brent Nyitray

Stocks are higher this morning as emerging markets rally. Bonds and MBS are down.

Mortgage Applications rose 2.3% last week as purchases rose 4.8% and refis rose 0.4%. The average 30 year fixed rate mortgage rose 3 basis points to 3.85%. The average jumbo rate increased 8 basis points to 3.82%.

Home prices rose 0.7% in March, according to the FHFA House Price Index. “While the overall appreciation rate was robust in the first quarter, home price appreciation was somewhat less widespread than in recent quarters,” said FHFA Supervisory Economist Andrew Leventis. “Twelve states and the District of Columbia saw price declines in the quarter—the most areas to see price depreciation since the fourth quarter of 2013. Although most declines were modest, such declines are notable given the pervasive and extraordinary appreciation we have been observing for many years.” Interesting to see prices begin to decline in some states.

A US appeals court threw out the $1.27 billion judgement against Bank of America for Countrywide’s sins related to the “hustle.” The 2nd U.S. Circuit Court of Appeals in New York said the proof at trial was insufficient under federal fraud statutes to establish liability. No comment yet from Manhattan U.S. Attorney Preet Bharara.

Filed under: Economy | 7 Comments »

Posted on May 24, 2016 by Brent Nyitray

Markets are higher this morning on no real news. Bonds and MBS are down.

New Home Sales came in much stronger than expected, at an annual rate of 619,000. This is the highest level since early 2008. While it is premature to bust out the champagne quite yet (prior to the bubble, the last time sales were this low was the early 90s), it is an encouraging sign. The Spring Selling season got off to a somewhat slow start, but seems to be picking up momentum. Note this number has an unusually wide margin for error this month, so expect a revision.

Speaking of new home sales, we got second quarter numbers out of Toll Brothers this morning. Earnings beat on the top and bottom lines, with revenues increasing 31% in dollars and 9% in units. Interestingly, average selling prices of signed contracts were flat. Contracts only rose 3%, and the problems were in California, with not enough inventory for sale. They continue to build out their urban apartment segment and plan to expand it to smaller cities and suburbs.

The Richmond Fed manufacturing index fell in May to -1 from 14.

More millennials are living with their parents than they are with a partner or significant other, for the first time in the modern era. This is probably a reflection of a lot of things – from the weak economy to people getting married later in life. However, it does represent pent-up demand for housing.

Foreclosure starts fell to 58,700 in April, the lowest level since 2006. Delinquencies increased slightly, but are still down 10% YOY. The active foreclosure inventory fell below 600,000 for the first time since 2007. The Northeast still has some wood to chop in terms of liquidating foreclosures.

Filed under: Economy, Morning Report | 14 Comments »