Vital Statistics:

| Last | Change | |

| S&P Futures | 2155.5 | -5.0 |

| Eurostoxx Index | 343.2 | 0.2 |

| Oil (WTI) | 48.6 | 0.4 |

| US dollar index | 86.6 | 0.4 |

| 10 Year Govt Bond Yield | 1.60% | |

| Current Coupon Fannie Mae TBA | 103.3 | |

| Current Coupon Ginnie Mae TBA | 104.2 | |

| 30 Year Fixed Rate Mortgage | 3.46 |

Markets are down this morning on no real news. Bonds and MBS are down as well.

The big event this week will be the jobs report on Friday. We will also have a lot of Fed-speak as well.

The PMI Manufacturing Index slipped in September, while the ISM manufacturing index rose.

Construction spending fell 0.7% in August. It is also down 0.3% on a year-over-year basis. Residential construction spending fell 0.2% and is up 1.3% for the year. Public construction was down 2.2% and is down 8.8% on a year-over-year basis. Note both Hillary Clinton and Donald Trump support a big infrastructure spending program.

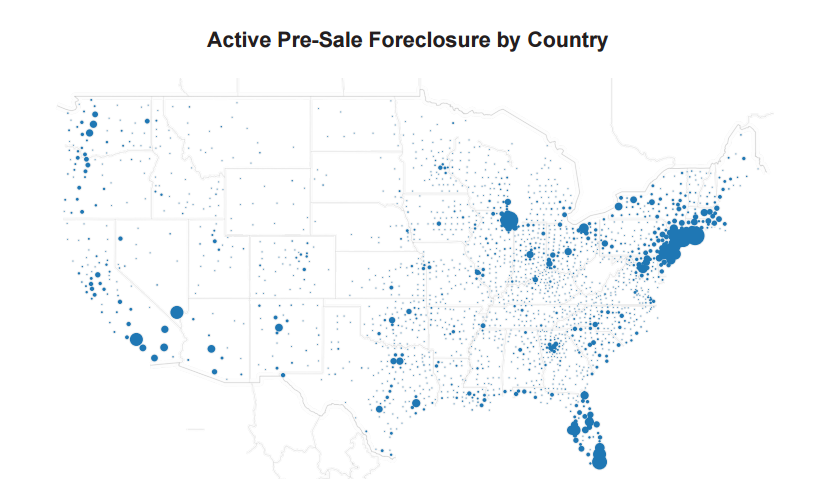

Delinquencies are down in August according to the Black Knight Mortgage Monitor. The pre-sale foreclosure inventory is now down around 1%, although the inventory is still concentrated in the Northeast, Florida, and Chicago areas. Cash-out refinances increased to 42% of all refis.

After Friday’s weak consumer spending data, the Atlanta Fed took down their estimate of Q3 GDP to 2.4% from 2.8%.

Portfolio Managers are forecasting the bond bull market will continue into the 4th quarter as global growth is simply too weak to push up inflation. Of course they are talking their books, but they are probably correct. Separately, Henderson of the UK bought Janus Capital this morning.

Over the weekend, the New York Times got ahold of Donald Trump’s taxes from 1995, where he showed a $916 million loss, which he has used to write off taxes owed going forward. Of course, using business losses to offset business income is as legal as eating a hot dog at the ballpark, so there probably isn’t a lot of political “there” there. Separately, Julian Assange claims he has emails which will finish Hillary Clinton, though WikiLeaks is delaying the release.

China continues to grapple with its housing bubble in hopes of engineering a soft landing. Watch the video at the end of the story, where investors storm an entrance in order to buy property.

Filed under: Economy, Morning Report | 47 Comments »