Vital Statistics:

| Last | Change | |||

| S&P futures | 2660 | 13.5 | ||

| Eurostoxx index | 373.93 | 6.6 | ||

| Oil (WTI) | 63.22 | -0.16 | ||

| 10 Year Government Bond Yield | 2.81% | |||

| 30 Year fixed rate mortgage | 4.41% | |||

Stocks are higher this morning on no real news. Bonds and MBS are down.

Initial Jobless Claims increased to 242k last week. Job cuts also jumped to 60k from 30k according to outplacement firm Challenger, Gray and Christmas. Retailers (probably Toys R Us) drove the increase. This is the biggest jump in 2 years.

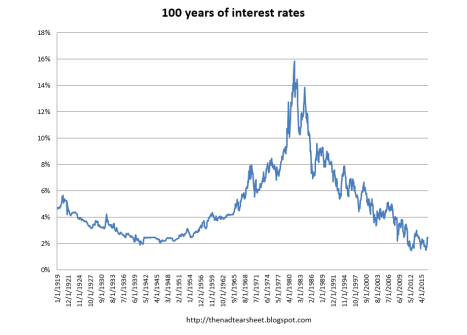

JP Morgan CEO Jamie Dimon discusses the state of the economy in his annual letter to shareholders. He argues with normal growth and inflation around 2% (the current state of affairs) historically, we would expect to see short-term rates around 2.5% and the 10 year trading around 4%. He argues that QE (both here and abroad) is what is suppressing the 10 year yield. That will reverse for the Fed this year, and in the near future overseas. There will be some countervailing forces at work, but we are in such uncharted territory that no one knows how it will turn out. Dimon then starts discussing the surprise 1979 rate hike (100 basis points on a Saturday!) and talks about how the Fed Funds rate then opened 200 bps higher that Monday. Just for the record, I want to put this chart out there – interest rate cycles are long. We are probably a generation (or two) from that sort of situation again, at least if historical observations are any guide.

Dimon makes another point in his letter about the state of the financial system. On one hand, it is much more stable and well-capitalized. Money market funds have higher restrictions, and there is much less leverage in the system overall. That said, post-crisis policy has removed the counter-cyclical levers in the financial system. First of all, the Volcker rule has meant less market-making. Investors have noted that it is much harder to trade securities, especially the less liquid ones. In a downturn, expect to see many securities go no-bid. In other words, investors will be stuck riding something down. Second, the newer bright lines means that banks will not be able to use their reserves to step in and lend. In Reminiscences of a Stock Operator, there was a credit crunch and banks were fully lent out to the reserve point. J.P. Morgan exhorts the banks to use their reserves. That is what they are for! And finally, in a swipe at the Obama Administration, the big banks are not going to agree to buy out the failing ones. JP Morgan bought Bear at the height of the crisis, as a favor to the Bush Administration. The Obama Admin then slammed them with fines for all of Bear’s sins.

We aren’t going to see much in the way of inflation without wage growth, and at least one economist (Noah Smith) is arguing that we aren’t seeing any because employers have too much market power. He also argues that minimum wage laws are not job killers, at least in the aggregate, despite what Econ 101 would say. His argument is that if employers do have market power, then they are earning a higher return than they would otherwise accept on their workforce. In other words, you could force them to hike wages, and they still will make enough that it won’t make sense to fire people. He then cites the usual Rx for increasing wages: higher minimum wage laws and more unions. The question is then where employers have market power. Perhaps in one-company towns that could be the case. But en masse? Possible, but not probable.

The trade deficit increased again in February, giving ammo to those who agitate for a trade war. A trade war could have an effect on interest rates. Right now, China sends us ships of stuff (phones, plastic goods, all sorts of things). In return (they aren’t giving it away), they have to take something. Right now, they largely take things like agricultural products. We would prefer it if they bought even more stuff. Since they aren’t, the get US dollars instead, which they then invest in Treasuries and other US assets. If trade decreases with China, they will theoretically buy less Treasuries, and that would mean higher interest rates, at least at the margin. To put this in perspective, the trade deficit with China in February was $29 billion. During QE, the Fed was buying $45 billion in Treasuries and MBS a month. So that isn’t chump change.

It is important to understand that we are in a negotiation phase with China, that many of these things are just proposals. Historically, these things get solved by a meaningless pledge that allows the US to claim victory, but doesn’t really make that much of a difference. As China gets richer, it will undoubtedly purchase more US goods and services. However, the savings rate is sky-high there – which means that consumption is low. They are in building mode.

Ginnie Mae has noted the abuses in VA IRRRLs and is taking action against some lenders. New Day and Nations Lending are no longer eligible to issue securities into multi-issuer pools. They will only be able to issue spec pools, which will trade at a discount.

Filed under: Economy, Morning Report | 22 Comments »