Vital Statistics:

| Last | Change | |

| S&P futures | 4,021 | -63.25 |

| Oil (WTI) | 80.77 | -0.43 |

| 10 year government bond yield | 3.59% | |

| 30 year fixed rate mortgage | 6.39% |

Stocks are lower this morning after the jobs report came in better than expected. Bonds and MBS are down.

The economy added 263,000 jobs in November, which was better than the 200,000 street estimate. The unemployment rate stayed steady at 3.7%. Wage inflation continues to increase, with average hourly earnings rising 0.6%, faster than the upward-revised 0.5% in October. The labor force participation rate and the employment-population ratio both declined 0.1%.

To tie this into what Powell was saying Wednesday at Brookings, the biggest component of core inflation – services ex-housing – is driven by wage inflation. The other two – goods and housing services – are less of an issue going forward. Services ex-housing is the result of an extraordinarily tight labor market, and the Fed would like to see the supply / demand imbalance in the labor market get more in balance.

There are two ways to do that. The first way is for the Fed to cool the economy with rate hikes, causing a recession and lowering the demand for workers. The other way is for workers who left during COVID to return. The latter method is preferable since it will fix the imbalance naturally. Unfortunately, the Fed doesn’t have any way to influence that. The long-COVID sufferer who decides to re-enter the labor force isn’t going to care what the Fed Funds rate is.

The imbalance in the labor force is perplexing. The most likely outcome is that it stems from two areas – a decline in immigration and an increase in early retirements. The latter one might be a long-COVID effect. Assuming long COVID isn’t a permanent state of affairs, the labor force participation rate should be ticking up over time.

The Fed Funds futures ticked slightly more hawkish on the jobs report, but we are still looking at a consensus of 50 basis points. The only other major report would be the CPI coming in on the morning the Fed begins their meeting.

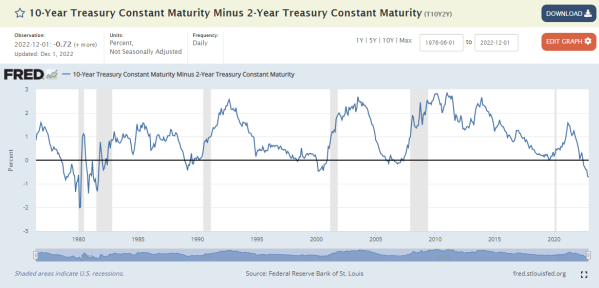

Stocks and bonds sold off on the employment number. The stock market reaction seems odd, but we may be in a “good news is bad news” environment for stocks which are fearing further rate hikes. The bond market’s reaction makes more sense. The yield curve is heavily inverted, back towards levels not seen since the early 1980s. The yield curve is typically positively slopes, which means it usually costs more to borrow for 10 years than it does for 2 years. There is a mean-reversion element too, which means you could think of the spread as a rubber band, and the further you get from normalcy, the greater the tension. In other words, with the two year being driven primarily by the Fed Funds projection and the 10 year being driven by market sentiment, further declines in long term rates will be more difficult to come by, and will be more fleeting.

The Atlanta Fed trimmed their GDP Now estimate to 2.8% from 4.3% in their latest model run. The ISM Manufacturing Survey, which has been in contraction mode for months, simply wasn’t comporting with a 4.3% expected GDP growth estimate.

Regardless, mortgage rates have been falling and are now back at levels last seen in mid-September.

Given my rubber band analogy they will want to be pulled higher, so the market is letting you back in.

Filed under: Economy | 20 Comments »