Vital Statistics:

| Last | Change | |

| S&P futures | 2853 | 3.1 |

| Oil (WTI) | 25.59 | 0.29 |

| 10 year government bond yield | 0.67% | |

| 30 year fixed rate mortgage | 3.36% |

Stocks are flat this morning on no real news. Bonds and MBS are up.

Mortgage Applications rose 0.3% last week as purchases rose 11% and refis fell 3%. “There continues to be a stark recovery in purchase applications, as most large states saw increases in activity last week. In the ten largest states in MBA’s survey, New York – after a 9 percent gain two weeks ago – led the increases with a 14 percent jump. Illinois, Florida, Georgia, California and North Carolina also had double-digit increases last week,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “We expect this positive purchase trend to continue – at varying rates across the country – as states gradually loosen social distancing measures, and some of the pent-up demand for housing returns in what is typically the final weeks of the spring home buying season.” Interesting comments about New York. It looks like people are fleeing NYC after the COVID-19 issue, and why not? NYC is expensive as heck, and the main thing to recommend it is the easy commute if you work there and all the great bars and restaurants. With work at home now becoming mainstream, is it worth the expense and the risk?

Delinquencies ticked up in the first quarter after hitting a record low in the fourth, according to the MBA. “The mortgage delinquency rate in the fourth quarter of 2019 was at its lowest rate since MBA’s survey began in 1979. Fast-forward to the end of March, and it is clear the COVID-19 pandemic is impacting homeowners. Mortgage delinquencies jumped by 59 basis points – which is reminiscent of the hurricane-related, 64-basis-point increase seen in the third quarter of 2017,” said Marina Walsh, MBA’s Vice President of Industry Analysis. “The major variances from the fourth quarter of 2019 to this year’s first quarter are tied to the increase in early-stage delinquencies for all loan types. For example, the 30-day FHA delinquency rate rose by 113 basis points, the second-highest quarterly ramp-up in the survey series. The 30-day VA delinquency rate rose by 78 basis points – the highest quarterly increase.”

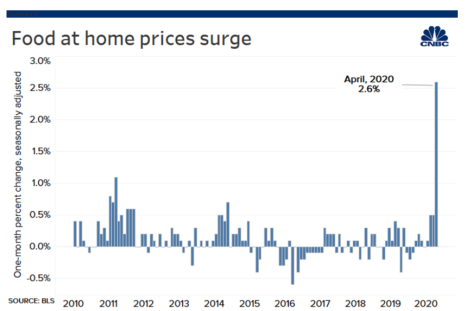

Wholesale prices fell in April, according to the PPI. The headline number was down 1.3% MOM and 1.2% YOY. Even ex-food and energy, trade services, etc, it was down on a YOY basis.

Jerome Powell warned of a prolonged recession after the Coronavirus issue get sorted out. He points out that this recession was not caused by a burst bubble or an inflationary spate which caused a tightening. “This downturn is different from those that came before it. Earlier in the post–World War II period, recessions were sometimes linked to a cycle of high inflation followed by Fed tightening. The lower inflation levels of recent decades have brought a series of long expansions, often accompanied by the buildup of imbalances over time— asset prices that reached unsupportable levels, for instance, or important sectors of the economy, such as housing, that boomed unsustainably. The current downturn is unique in that it is attributable to the virus and the steps taken to limit its fallout. This time, high inflation was not a problem. There was no economy-threatening bubble to pop and no unsustainable boom to bust. The virus is the cause, not the usual suspects—something worth keeping in mind as we respond.” For this reason, I think the economic damage won’t be as bad as the media is hoping. I also think a prolonged period of social distancing is not in the cards either, people aren’t going to put up with that, not even in deep blue states like NY and CA.

Filed under: Economy, Morning Report | 19 Comments »