Vital Statistics:

| Last | Change | |||

| S&P futures | 2743 | 9.7 | ||

| Eurostoxx index | 388.45 | 1.55 | ||

| Oil (WTI) | 65.49 | -0.32 | ||

| 10 Year Government Bond Yield | 2.91% | |||

| 30 Year fixed rate mortgage | 4.54% | |||

Stocks are higher this morning on no real news. Bonds and MBS are flattish.

We should have a relatively quiet week coming up, with not much in the way of data and no Fed-speak.

Friday’s jobs report was pretty much a Goldilocks report as far as the markets are concerned. Strong job growth, with respectable (but controlled) wage growth is exactly what the Fed wants to see. Tomorrow, we will get the JOLTS job openings report, which should show job openings of around 6.5 million.

Academics are scratching their heads trying to figure out why wage growth is so slow with unemployment below 4%. With the economy at “full employment” at least according to the unemployment numbers, how can so many jobs still be created? And if unemployment is below 4% and we are at a record number of job openings, where is the wage growth?

First of all, the jobs report had wage growth at 2.7%, and the core PCE inflation rate is 2%. So, we do have inflation-adjusted (i.e. real) wage growth. Second, productivity is a puzzle. It has been low for a decade, and part of the issue is that productivity is notoriously hard to measure, especially when valuable goods are “free” or hard to measure. Think of social media, which has all sorts of entertainment value and productivity enhancing value, yet is supposedly free. Yes, you are paying with your data, but what is your data worth? Productivity calculations need a dollar value. Productivity has been low, but there is a huge uncertainty range around that number.

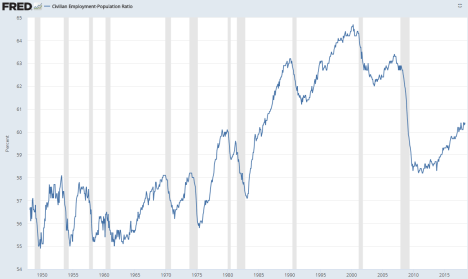

I think a huge part of the issue is the fact that the unemployment rate excludes anyone who has been unemployed over 6 months, and there is a huge reservoir of workers on the sidelines who want to return to the labor force. Companies know this, and all they have to do is relax their standards (i.e. hire people who have been out of the labor force for a while) and they will fill their positions. At the end of the day, this is a numbers game. The employment-population ratio has been steadily increasing since 1970 as women have entered the workforce. It peaked in 2000, bottomed after the Great Recession, and has been steadily working its way upward. The demographic factor (retiring baby boomers) is probably getting overplayed here, as most people no longer can retire at 65 (and there really is no reason why most can’t continue to work).

Leftist economics are arguing that employers are somehow colluding to keep wages low, and therefore are suggesting a panoply of policy levers designed to artificially force up wages and increase unionization. Aside from non-competes in the rarefied air of Silicon Valley engineers, generally this doesn’t happen – cartels are almost impossible to make work (witness OPEC) and there are simply too many employers who don’t compete with each other to coordinate it, even if they wanted to.

Instead of jumping to the “market failure” conclusion, the answer is that there is more slack in the labor market than the numbers suggest. There may be a mismatch of skills, where there is high demand in areas where there aren’t a lot of available workers (skilled trades, data scientists) but overall the employment population ratio doesn’t lie. The last time we saw decent wage growth was the 90s, where the employment-population ratio was around 63%. The latest number was 60.4%. That difference in a population of 326 million is about 8.5 million jobs. That is about 3 year’s worth of job growth, without population growth which is still measurable at 0.7% a year. Even if you take into account the 6.5 million job openings, you still have probably 2 million extra workers on the sidelines. IMO, that is your answer about wage growth, not monopsony of collusion, which is just a specious argument for more government intervention in the labor markets.

Chart: Employment-population ratio.

House price appreciation continues apace, and between rising price and interest rates, the monthly house payment on the median house with 20% down has increased by $150 a month, according to Black Knight Financial Services. Income growth at 2.7% is not going to keep up with home price appreciation, which is running at around 6% a year. When rates were falling, we were able to paper over that issue with lower mortgage payments, but that game is over. Housing starts are still way too low, and that question is even more perplexing than wage growth.

Note that private equity is now building homes for rent, which should alleviate some of the supply problem. It was only a matter of time until new entrants saw the opportunity that the big builders have been sitting on. Politicians are getting sick and tired of the lack of housing supply (especially at the lower price points).

Friday’s jobs report reversed the Euro-driven drop in the June Fed Funds futures. At one point, they were predicting a 81% chance of a hike. Now it is back up to a near certainty. The December futures are predicting a 40% chance of 4 or more hikes this year and a 60% chance of 3 or less.

Filed under: Economy, Morning Report | 12 Comments »